It’s finally happening.

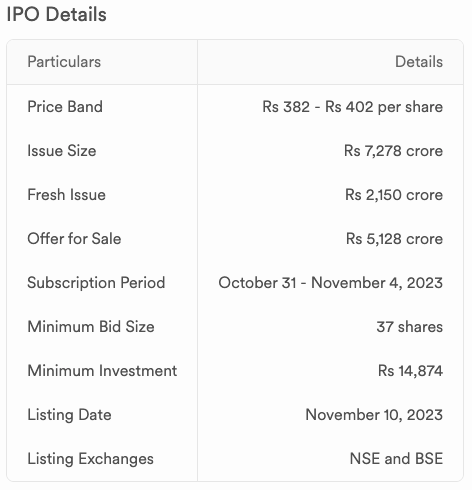

Lenskart, the eyewear brand that turned eyeglasses into a lifestyle product, is set to hit the public markets. Backed by SoftBank, KKR, Temasek, and Abu Dhabi’s sovereign fund, the company is launching one of India’s biggest consumer-tech IPOs in recent memory; a ₹7,278 crore issue that values it close to ₹70,000 crore (around $8 billion).

For a company that started as an online eyewear store just over a decade ago, this listing feels like a defining moment in India’s startup journey — one that blurs the line between tech and retail.

But before we zoom in on Lenskart, let’s zoom out for a second.

India’s eyewear market has long been both fragmented and underpenetrated. Redseer data cited in the company’s filings pegs the domestic eyewear market at roughly ₹50,000 crore in FY25, expected to touch ₹83,000 crore by FY30. Despite that size, only about 35% of Indians who need vision correction actually wear glasses. Compare that with the US or Japan, where penetration exceeds 70%.

The reasons range from affordability gaps and social stigma to uneven access to optometrists in smaller towns. But the winds are changing. India’s young population is spending more time on screens, myopia cases are rising fast, and fashion is influencing how consumers perceive eyewear.

The result is a market that’s maturing; not just in size, but in aspiration.

The eyewear business also sits at the intersection of healthcare and lifestyle, which makes it complex but rewarding. Traditionally, it was dominated by unorganised retailers and legacy opticians. Titan Eyeplus brought some structure to the space in the 2000s, but it still remained an offline-first business.

Lenskart’s bet was different; it took eyewear online first and then built stores to support that growth. It began by selling prescription lenses and sunglasses online in 2010, before opening its first physical store in 2013. The idea was simple yet disruptive: combine the scale and reach of e-commerce with the trust and convenience of physical touchpoints.

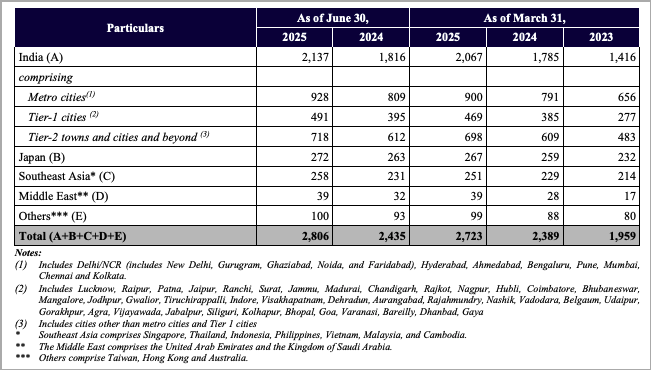

Today, it operates 2,723 stores across 14 countries; including 2,067 in India and 656 in Southeast Asia, Japan, and the Middle East.

That global spread is not just for show.

Lenskart’s model is built around what it calls an “omnichannel” strategy: customers discover online, get tested offline, and buy either way. About 70% of new customers find the brand through digital channels, but nearly half of total orders close at physical outlets. That blend is what keeps the customer experience consistent while lowering acquisition costs over time.

The brand’s own data shows how this is paying off: between FY23 and FY25, its store network in India jumped from 1,416 to over 2,100, while the total global count went from under 2,000 to nearly 2,800.

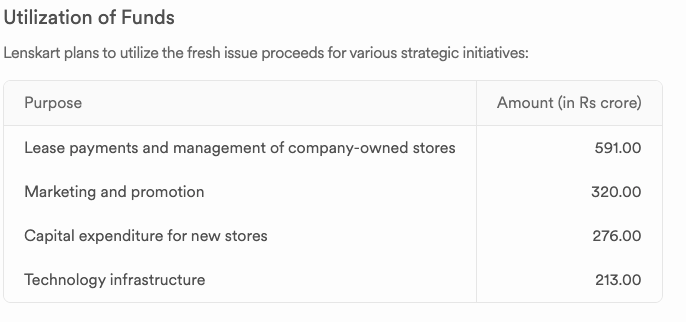

This offline expansion is where much of the IPO money will go — ₹276 crore for new company-owned stores, ₹591 crore for lease deposits and rentals, ₹213 crore for tech and cloud investments, and ₹320 crore for brand marketing.

Up to 35% of the proceeds are also reserved for future acquisitions.

Behind the stores, though, is a supply chain that resembles a precision machine. Lenskart manufactures much of what it sells. It runs plants in Bhiwadi and Gurugram, and operates additional facilities in Singapore and the UAE. It even has a joint venture in China, Baofeng Framekart Technology Ltd, for frame production. This vertical integration helps maintain margins and control design and quality in a category where differentiation is subtle but essential.

The company’s data-driven design teams, automated lens assembly lines, and AI-backed recommendations for frame fitting give it an edge over traditional retailers who rely on distributors.

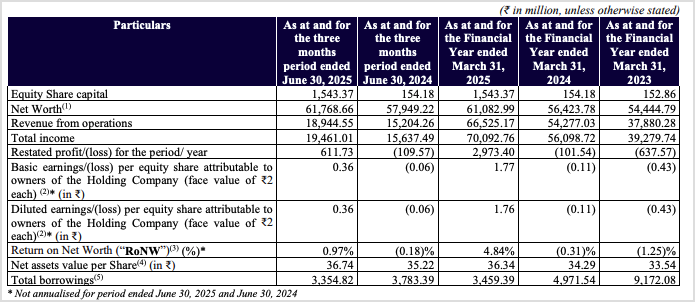

All of that shows up in its financial turnaround. In FY25, Lenskart reported revenue from operations of ₹6,652.5 crore; a 23% jump year-on-year and a two-year CAGR of 33%. More importantly, it flipped from a loss of ₹10 crore in FY24 and ₹637 crore in FY23 to a net profit of ₹297.3 crore in FY25.

Gross margins improved by 500 basis points to about 69%, thanks to scale efficiencies, a growing share of in-house brands like John Jacobs and Vincent Chase, and better procurement terms with suppliers.

For the three months ended June 30, 2025, revenue rose 25% year-on-year to ₹1,894 crore, while net profit stood at ₹61 crore — showing that the turnaround is holding stead.

Now here’s where it gets interesting for investors.

Lenskart’s valuation at the upper end of ₹402 per share implies a price-to-earnings multiple of around 228x FY25 earnings. It means investors are paying ₹228 for every ₹1 the company earned last year; a sign that the market is betting heavily on its future growth rather than its current profits.

That’s extremely high by conventional standards, especially when compared to listed peers in adjacent categories. Titan Company, for example, trades at roughly 80x earnings, while even global eyewear players like EssilorLuxottica command a PE around 35–40x.

The justification for Lenskart’s premium lies in its growth trajectory and the low penetration of its market but that also means much of its future is already priced in.

The company’s balance sheet, however, looks cleaner than most tech IPOs we’ve seen in the past. Total borrowings have fallen from ₹9,172 million in FY23 to ₹3,459 million in FY25, indicating reduced leverage. Return on net worth, which was negative for two consecutive years, turned positive at 4.31% in FY25 and stood at nearly 1% in Q1 FY26.

With net assets per share climbing to ₹36.74, the fundamentals are trending in the right direction. Still, investors must note that profitability is recent and thin; a bad quarter or unexpected expense could tilt it again.

In the broader industry context, Lenskart’s rise also reflects how consumer behavior has evolved. In India, the eyewear market is shifting from being price-sensitive to value-conscious. People now see eyewear as both functional and fashionable; an accessory that can be switched with outfits, just like watches or shoes. That mindset has fueled premiumisation.

Lenskart’s dual-brand strategy caters to both sides: Vincent Chase focuses on affordable fashion, while John Jacobs taps the aspirational, high-margin segment. Titan Eyeplus, its nearest large competitor, still operates mostly offline and focuses more on traditional optometry and established brands.

The difference is that Titan’s customers buy glasses once every few years, while Lenskart’s are encouraged to buy multiple pairs a year. That behavioral difference is what the company monetizes.

The growth story is solid, but there are a few weak spots that deserve a closer look.

A significant part of its manufacturing depends on imports from China, making it vulnerable to currency fluctuations, shipping disruptions, or geopolitical tensions. While its joint venture there helps manage costs, it also concentrates risk.

The omnichannel model, though powerful, is capital-heavy; setting up new stores and maintaining brand consistency across markets takes serious spending. And while Lenskart’s international expansion looks promising, it’s also entering competitive regions like Southeast Asia, where local players and established brands have loyal followings.

In essence, scale may not automatically translate into profitability abroad.

Another factor that may slip past a casual investor is that eyewear, unlike electronics or apparel, doesn’t lend itself easily to impulsive repeat purchases. Even with strong marketing, buying cycles depend on prescription updates or fashion seasons, not impulse.

That means Lenskart must keep innovating on design and convenience to sustain customer frequency. The company’s push into AI-led lens customization and faster delivery is one answer, but whether that translates to durable margins will only become clear over time.

Still, it’s hard to ignore how Lenskart has executed so far. Few Indian startups have built a business that combines manufacturing, retail, and tech at this scale. The brand is visible, the economics are improving, and the global opportunity is vast. And as India’s middle class expands and screen usage grows, the base demand for eyewear will likely stay resilient.

From an investor’s lens, Lenskart’s IPO sits at the crossroads of optimism and caution. On one hand, it’s a profitable consumer-tech company in a high-growth category with a strong brand moat. On the other, its valuation leaves little room for error, and the execution risks are real.

The enthusiasm will likely drive strong subscription in the short term, but long-term returns will depend on how efficiently it scales new stores and whether it can sustain double-digit growth without compromising margins.

In the larger picture, Lenskart’s listing is more than a financial event. It’s a symbolic one; the graduation of India’s D2C ecosystem into mainstream capital markets.

For a generation of startups that grew up chasing market share, it shows that profitability and discipline eventually matter more than hype. For investors, it’s a chance to own a slice of a company that redefined an everyday product with technology and design.

And for Lenskart, it’s the beginning of a new chapter; one where its vision will be tested not in focus groups or fundraising decks, but on the trading screens of Dalal Street.

FAQs

What is the Lenskart IPO issue size and valuation?

Lenskart’s IPO is valued at around ₹7,278 crore, with the company seeking a market capitalization of nearly ₹70,000 crore (about $8 billion) at the upper end of its price band. It includes a ₹2,150 crore fresh issue and an offer for sale by existing shareholders.

What is the price band for the Lenskart IPO?

The Lenskart IPO price band is set between ₹382 and ₹402 per share. Investors can apply for a minimum of one lot, and each lot will include 37 shares.

When will the Lenskart IPO open and close?

The IPO opens for subscription on October 31, 2025, and closes on November 4, 2025. Anchor investors will be able to bid a day earlier, on October 30.

What will Lenskart use its IPO proceeds for?

Lenskart plans to use the IPO proceeds for store expansion, lease deposits, technology upgrades, and brand marketing. A portion will also go toward acquisitions and general corporate purposes over the next three years.

How is Lenskart performing financially?

Lenskart reported a revenue of ₹6,652.5 crore in FY25, up 23% year-on-year. It turned profitable with a net profit of ₹297.3 crore after losses in previous years, and its gross margins improved to nearly 69%.

Why is Lenskart’s IPO valuation considered high?

At ₹402 per share, Lenskart’s price-to-earnings ratio stands at about 228x FY25 earnings, meaning investors are paying ₹228 for every ₹1 the company earned last year. This high multiple reflects strong future growth expectations rather than current profits.

What are the key growth drivers for Lenskart?

Lenskart’s growth is driven by increasing screen time, rising eye health awareness, fashionable eyewear trends, and its omnichannel model that blends online discovery with offline sales. Its focus on vertical integration and in-house brands also supports higher margins.

What are the major risks or challenges for Lenskart investors?

Key risks include dependence on China for raw materials, the capital-intensive nature of its store network, and slower repeat purchases since eyewear isn’t an impulse category. Its international expansion also faces tough local competition.

How does Lenskart compare to competitors like Titan Eyeplus?

Titan Eyeplus remains primarily offline and focuses on established optical brands, while Lenskart operates across both online and offline channels with in-house brands like John Jacobs and Vincent Chase, catering to both mass and premium segments.

Should investors consider subscribing to the Lenskart IPO?

Lenskart’s IPO offers exposure to a growing consumer-tech brand in a high-potential market, but the high valuation leaves little margin for error. Long-term returns will depend on sustained profitability and execution across new markets.