OYO is back.

After nearly five years of delays, withdrawals, and endless speculation, the travel and hospitality company has once again knocked on SEBI's door. This time, it wants to raise up to ₹6,650 crore through a fresh issue of shares.

Unlike many recent IPOs, there is no Offer for Sale (OFS). Existing investors like SoftBank, Microsoft, Airbnb and Lightspeed are not selling their shares. Instead, all the money raised will go into the company itself. That sounds like a vote of confidence. The real question is why it is going public now.

To understand that, we need to rewind a few years.

Back in 2021, OYO looked very different. It was still the startup that had become famous for turning small independent hotels into branded budget accommodations. The company had expanded aggressively across more than 80 countries, was backed by SoftBank, and carried a valuation of nearly $10 billion at its peak.

It filed its first Draft Red Herring Prospectus (DRHP) in October 2021, hoping to raise around ₹8,430 crore. But the IPO never happened. Market conditions deteriorated, technology valuations collapsed globally, investors became far more cautious about loss-making startups, and OYO quietly put its listing plans on hold.

The company tried again through the confidential filing route in 2023. That attempt also did not materialise. Now, in 2026, OYO is making its third serious attempt to enter the public markets. But this is no longer the same company that investors saw five years ago.

In fact, the biggest change is that OYO has slowly stopped being just an Indian budget hotel company.

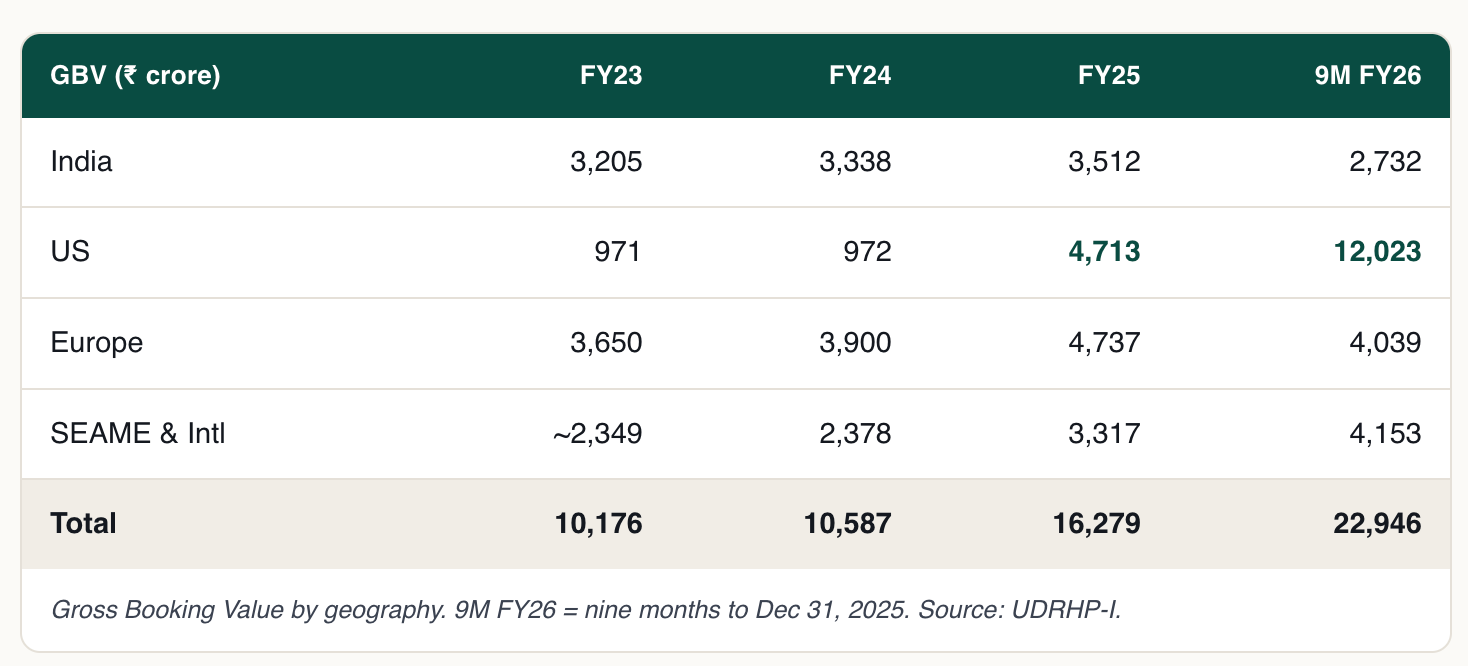

Today, it operates 43 brands across more than 35 countries. Its network includes over 24,300 hotels, more than 124,000 homes, and nearly 145,000 listings globally. Over the past few years, it has quietly expanded into vacation rentals across Europe through brands like Belvilla and DanCenter, entered urban holiday homes through acquisitions like CheckMyGuest in France, expanded into Australia through MadeComfy, and most importantly, bought G6 Hospitality, the owner of Motel 6 and Studio 6 in the United States.

That last acquisition changes almost everything about the OYO story.

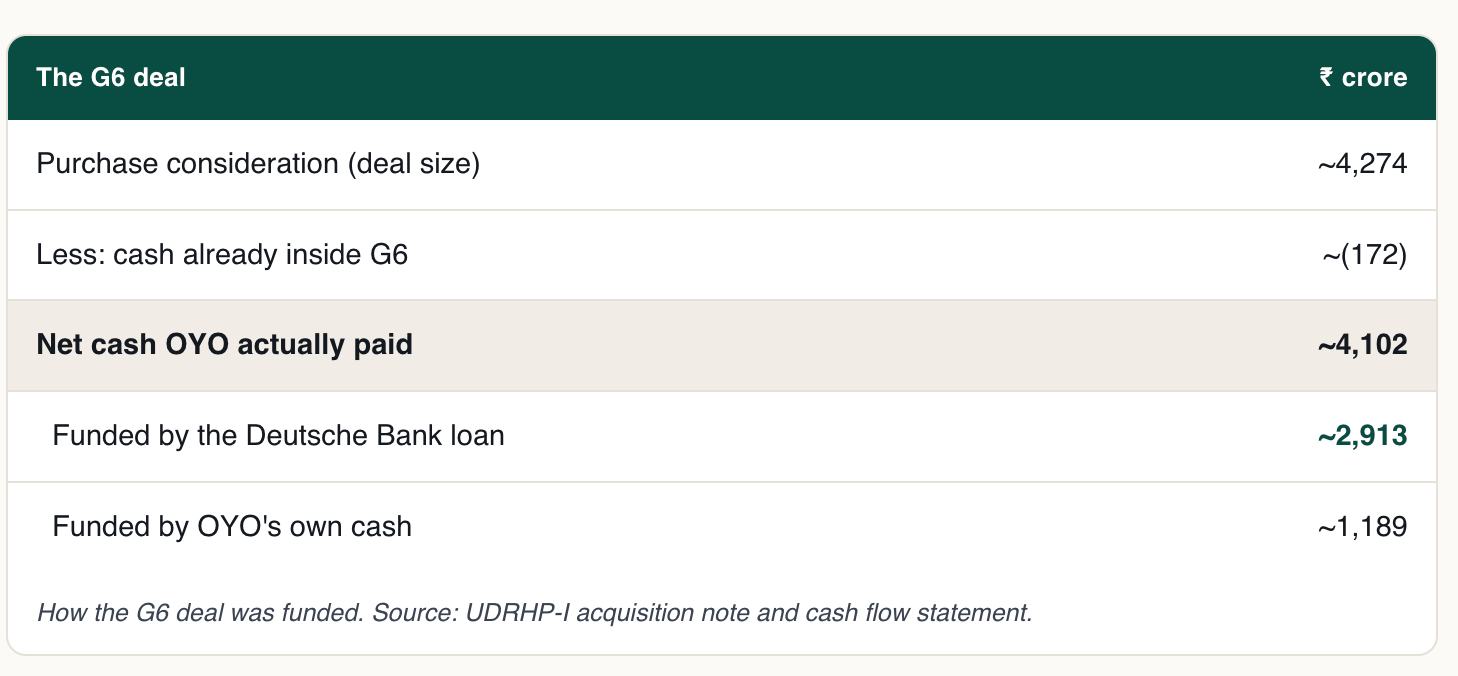

In September 2024, OYO agreed to acquire G6 Hospitality from Blackstone for around $525 million. The deal closed in December 2024. Motel 6 is one of the most recognised economy lodging brands in the United States, operating thousands of franchised properties. Overnight, OYO went from being known primarily as an Indian travel-tech startup to owning one of America's largest budget motel chains.

This acquisition immediately changed OYO's financial profile. For the nine months ended December 2025, the company reported revenue from operations of ₹6,941 crore, already higher than the ₹6,259 crore it generated during the entire previous financial year. And this looked like an explosive growth. But there is an important nuance.

A significant part of this jump comes from consolidating G6 Hospitality into OYO's financial statements. In other words, OYO didn't suddenly convince millions of new travellers to book through its existing platform. It bought a mature business that was already generating revenue and added those numbers to its own books. That does not make the growth any less real, but it does change how investors should interpret it.

Growth driven by acquisitions is very different from growth generated organically.

The same nuance appears when you look at profitability.

For the first nine months of FY26, OYO reported a profit after tax of ₹748 crore. At first glance, that seems to settle one of the biggest criticisms the company has faced over the years. OYO is finally profitable.

However, around ₹559 crore of this profit came from a deferred tax credit. Think of it as a tax benefit that the company has earned because of losses it incurred in the past. It boosts reported profit today, even though no new cash has come into the business.

After removing this adjustment, the company's profit before tax was much smaller. The quality of earnings matters just as much as the earnings themselves.

But the real story isn't how much OYO wants to raise. It's what it plans to do with the money.

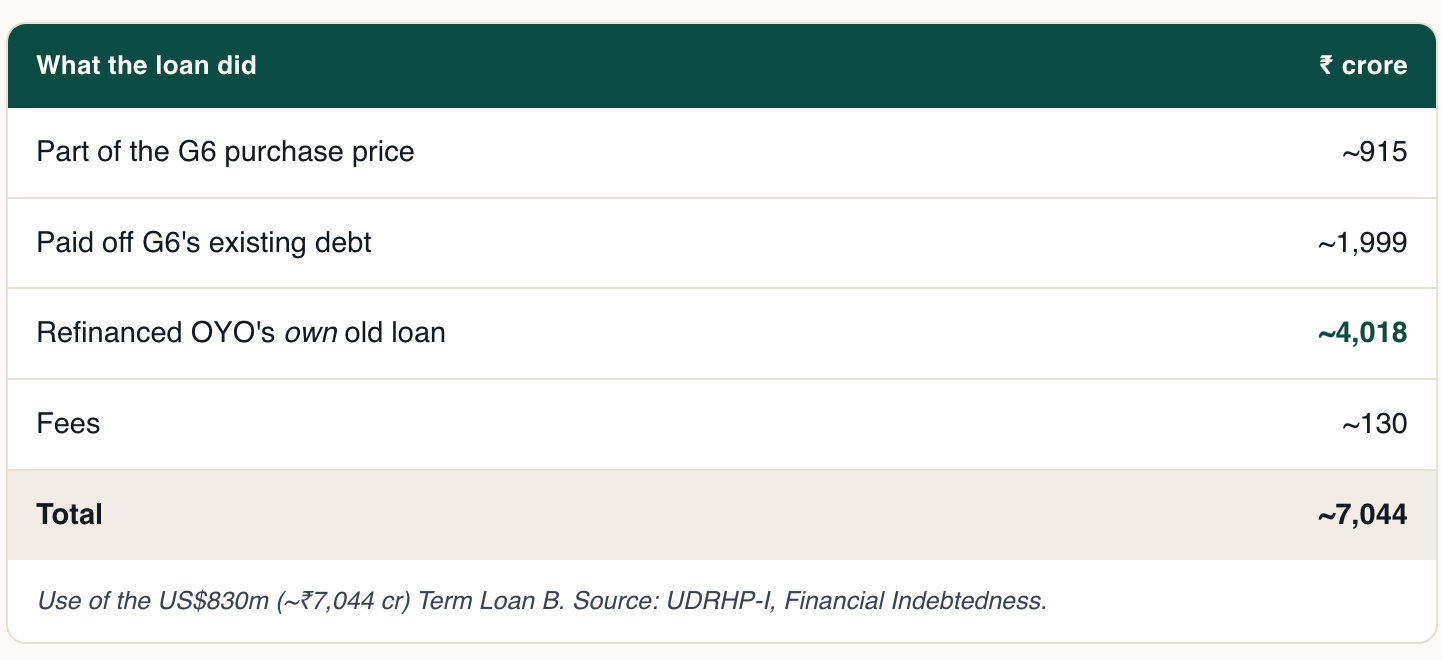

Nearly ₹4,987 crore of the IPO proceeds will be used to repay or prepay borrowings taken for the acquisition of G6 Hospitality. That means roughly three-fourths of the fresh capital is earmarked for reducing debt rather than funding new expansion.

This is probably the most important insight in the entire IPO.

Most companies tell investors they are raising money to build factories, expand capacity, enter new markets or launch products. OYO is effectively telling investors something different. It wants public market capital to strengthen its balance sheet after making one of the biggest acquisitions in its history.

Reducing debt can improve future profitability by lowering interest expenses. But it does change the investment thesis. Investors are not primarily funding growth. They are helping OYO digest the largest acquisition it has ever made.

OYO paid for the Motel 6 acquisition partly by taking a large loan instead of issuing more shares. This meant existing shareholders didn't have to give up part of their ownership. But loans come with interest payments. That is why reducing this debt has become one of OYO's biggest priorities, because the lower the debt, the less it will have to spend on interest every year.

Interestingly, OYO's business model today also looks very different from what many people still remember.

The company built its reputation by leasing hotels, standardising rooms, and putting the OYO brand on independent properties. That strategy eventually created enormous operational complexity and led to disputes with hotel owners over pricing, payments and contracts. Over time, OYO gradually shifted towards a far more asset-light franchise and technology model.

Today, instead of owning hotels or taking on large lease commitments everywhere, it increasingly earns through franchise fees, software, booking commissions, hotel management systems and technology services. This shift has made the business less capital intensive and more scalable, although lease liabilities still remain on the balance sheet in several markets.

Technology is another part of OYO's business that often gets overlooked.

The company no longer describes itself simply as a hotel aggregator. It has built pricing engines, property management software, channel management systems, booking platforms and operational tools that hotels use to manage inventory and optimise occupancy.

Even many of its acquisitions are not just about adding hotel rooms but about adding technology, operational capabilities and new customer segments. For example, its acquisition of Danish pricing technology assets was aimed at improving revenue management for vacation rentals, while CheckMyGuest strengthened its presence in professionally managed urban homes across Europe.

Another interesting aspect is how global OYO has quietly become.

Its subsidiary list now spans Europe, North America, Latin America, the Middle East, Southeast Asia and Australia. The company owns or operates businesses across France, Spain, Italy, Croatia, Switzerland, Denmark, Mexico, Brazil, Chile, Peru, Colombia, the UAE, Malaysia, Thailand and several other markets. It is difficult to classify OYO as purely an Indian company anymore because a growing share of its operations, acquisitions and revenues are international.

None of this means OYO's journey has been smooth.

The company has spent years dealing with legal disputes, partner complaints, regulatory scrutiny and governance questions. Hotel associations have accused it of unfair contract practices. The Competition Commission of India previously investigated arrangements involving OYO and online travel platforms.

The long-running dispute with Zostel also became a major talking point during its first IPO attempt.

On top of that came the pandemic, which devastated the hospitality industry, forcing OYO to lay off thousands of employees globally and rethink its expansion strategy.

Perhaps the biggest setback, however, was the collapse in its valuation.

At one point, OYO was valued at nearly $10 billion. As global technology stocks corrected and investors began prioritising profitability over growth, the company's valuation fell sharply in subsequent funding rounds. Instead of chasing expansion at any cost, management shifted its focus towards improving margins, reducing losses, simplifying operations and building a more sustainable business.

That shift is visible throughout the latest DRHP.

The emphasis is no longer on how many countries OYO has entered or how quickly it is adding hotels. Instead, the company repeatedly highlights profitability, operating leverage, technology, disciplined acquisitions and capital allocation.

There is another detail worth noting. This IPO contains no Offer for Sale.

Existing shareholders are not using the public issue to cash out. SoftBank remains the largest shareholder, while investors such as Microsoft, Airbnb, Khazanah Nasional and Lightspeed continue to stay invested. Promoters together still own a majority stake.

So, what exactly are investors buying if OYO finally lists?

They are not buying the same startup that filed for an IPO in 2021. They are buying a company that has survived one of the toughest periods in global hospitality, abandoned its hypergrowth strategy, acquired one of America's largest budget motel chains, built a much broader international presence, improved profitability, and is now asking public investors to help it reduce debt and begin its next phase with a cleaner balance sheet.

Whether that deserves the valuation OYO ultimately seeks is a separate debate that the market will decide.

But one thing is already clear.

The company going public today is very different from the OYO most people still remember. It is no longer just India's budget hotel startup. It is trying to become a global hospitality platform, and this IPO is less about funding a dream than proving that the transformation is finally complete.