A few years ago, India's investing story looked unstoppable.

Every month, SIP inflows were hitting fresh records, demat accounts were growing at breakneck speed, and mutual funds had become a household conversation. It felt like India was finally embracing financial assets.

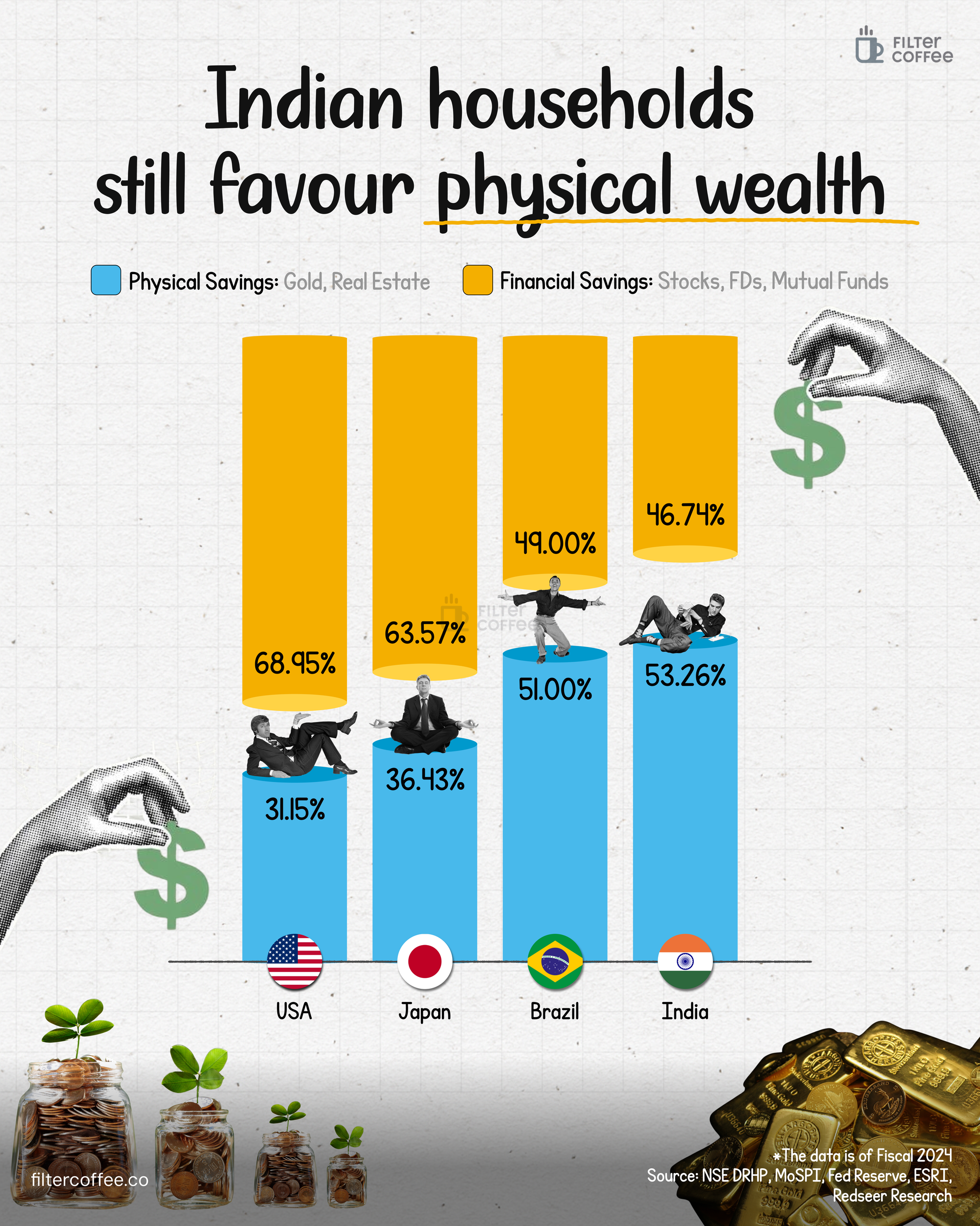

Yet, the latest data tells a different story. Indian households still park a larger share of their wealth in physical assets like gold and real estate than in stocks, mutual funds and other financial investments.

In FY24, physical assets accounted for just over 53% of household savings, while financial assets made up around 47%. That's quite different from most major economies.

Financial assets account for roughly three-fourths of household wealth in the US, around 70% in Japan and nearly two-thirds in the UK. Germany and France have a more balanced mix, while even China now holds a slightly larger share of wealth in financial assets than physical ones. India remains one of the few large economies where homes, land and gold still outweigh financial investments.

At first glance, this seems surprising. But for most Indian families, wealth has always been about more than just returns. A home represents security, stability and something that can be passed down through generations.

Gold, meanwhile, is not only deeply rooted in tradition but also serves as an emergency reserve that can be pledged for loans. These assets are tangible, familiar and trusted in a way financial products are still striving to become.

That doesn't mean financialisation isn't happening. Far from it.

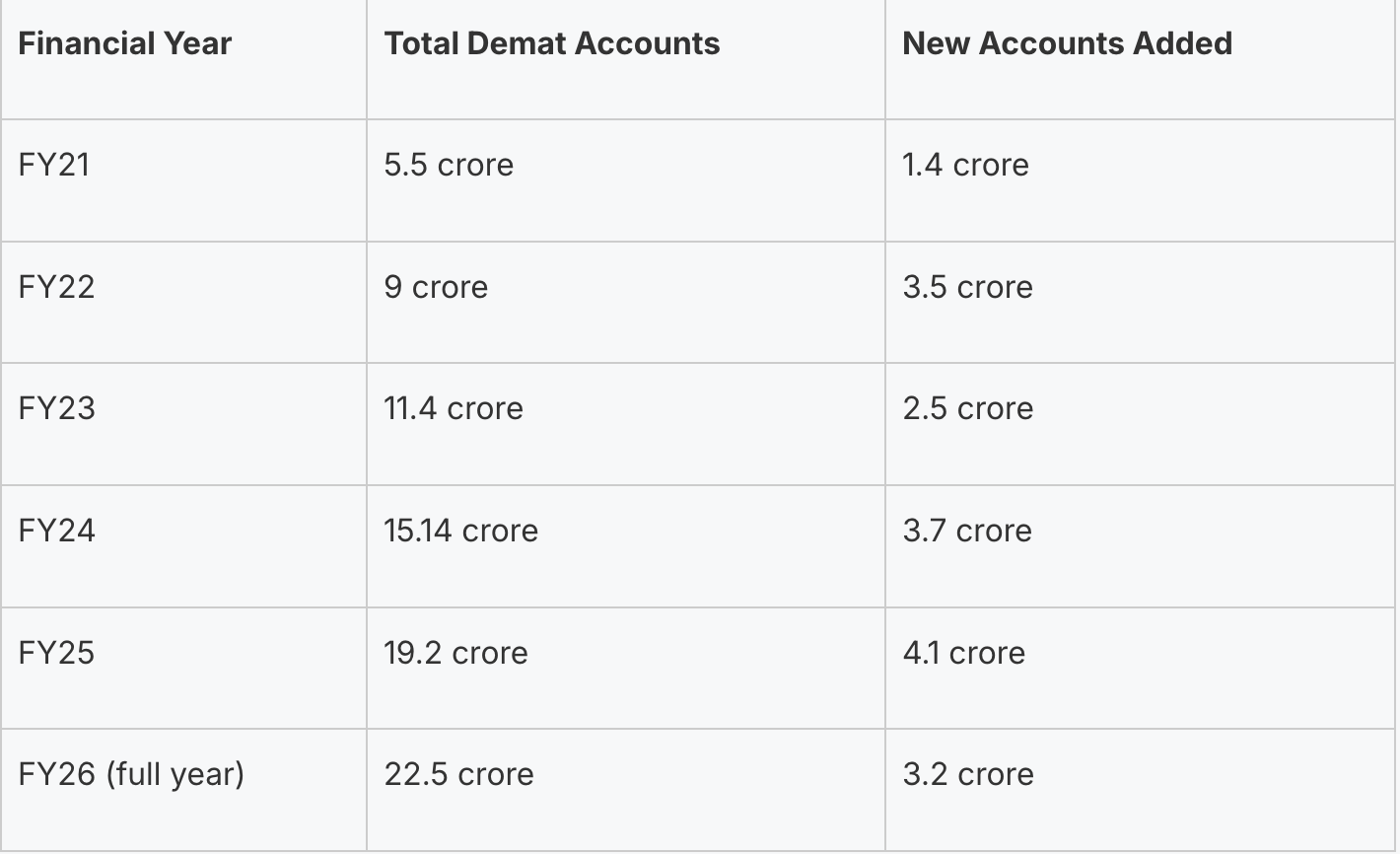

Retail participation in India’s capital markets accelerated sharply in FY26, with 235 lakh demat accounts added till December 2025, taking the total number of accounts beyond 21.6 crore, according to the Economic Survey 2025-26.

Monthly SIP inflows continue to scale new highs, and mutual funds are steadily expanding beyond metro cities. The real shift is that households are adding financial assets to their portfolios rather than replacing physical ones.

Even within financial savings, bank deposits are gradually losing share as more money flows into equities, mutual funds, insurance and pension products.

The bigger story isn't that Indians are choosing between gold and stocks. They're choosing both. Physical assets continue to offer comfort and stability, while financial assets are becoming the engine of long-term wealth creation. As incomes rise, financial literacy improves and capital markets deepen, this balance is likely to shift further. But for now, India's wealth story remains rooted in a simple belief: own something you can see, while steadily building wealth through something you can't.