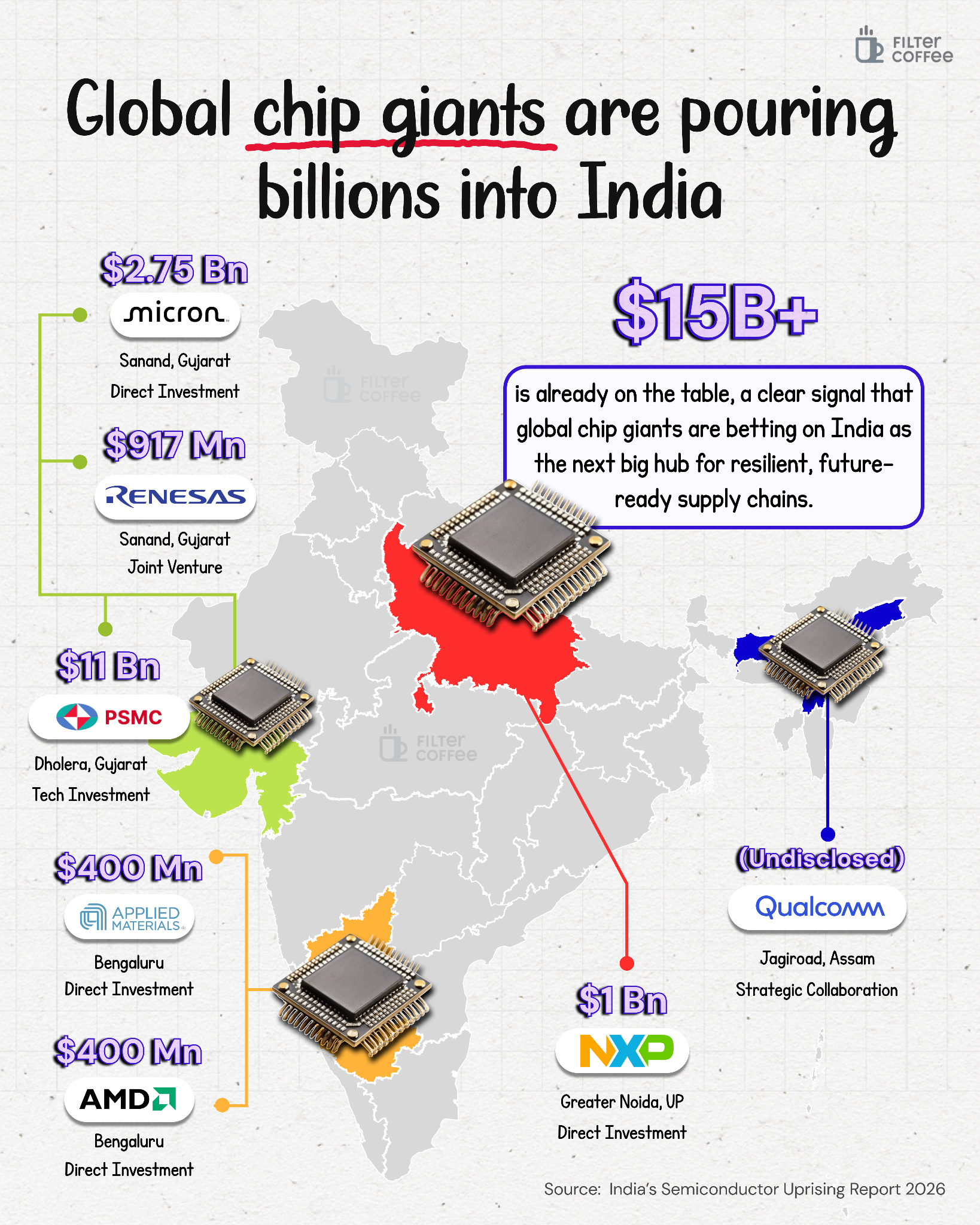

Global chip giants are building factories across India and the number is already past $15 billion in committed investments. Micron has opened its semiconductor assembly and test plant in Gujarat. Tata is building a full-fledged chip fabrication unit with Taiwan’s PSMC in Dholera. Qualcomm has tied up with Tata to manufacture automotive chips in Assam. And companies like AMD, Applied Materials, and Renesas are expanding design and R&D operations across Bengaluru and Noida.

To understand why this is happening now, you need to rewind to 2020. When Covid hit, the world ran out of chips. Cars couldn’t be produced, electronics were delayed, and even gaming consoles became scarce. The problem was simple. Almost the entire world depended on a few regions like Taiwan, South Korea, and parts of China for semiconductor supply. When that chain broke, everything else followed.

Since then, countries have been trying to “de-risk” their supply chains. The US passed the CHIPS Act. Europe followed with its own subsidies. And India entered the game with a ₹76,000 crore semiconductor mission, offering incentives covering up to 50% of project costs. The pitch was simple. If companies want to diversify away from China and Taiwan, India will help absorb the risk.

That pitch seems to be working.

But here’s where it gets nuanced. Not all chip investments are the same. A full semiconductor fab, like the one Tata and PSMC are building, is the most complex piece. It can cost $10 billion or more and takes years to become operational. These fabs process silicon wafers and are the core of chip manufacturing.

Then comes OSAT or ATMP facilities. These are assembly, testing, marking, and packaging units. Micron’s Gujarat plant falls into this category. It’s still critical, but less complex than a fab and quicker to scale. India is seeing more traction here because it’s easier to build capabilities in stages.

And then there’s design and R&D. This is actually where India already has an edge. Companies like AMD, Renesas, and Applied Materials are investing hundreds of millions of dollars into engineering talent and chip design capabilities. Renesas has even started work on 3nm chip design in India, which is cutting-edge globally.

So what India is building isn’t just one thing. It’s a layered ecosystem. Fabs, packaging units, and design centres, all coming up together.

Geographically too, this is spreading out. Gujarat is becoming the manufacturing anchor with Sanand and Dholera. Assam is emerging as an unexpected player with Tata’s packaging plant and Qualcomm’s automotive chip partnership. Karnataka and Uttar Pradesh are positioning themselves as design and electronics hubs.

The scale is also expanding quickly. By 2025–26, India had approved around 10 semiconductor-related projects worth roughly ₹1.6 lakh crore. And the domestic semiconductor market itself is expected to double from about $45–50 billion today to over $100 billion by 2030, driven by demand from smartphones, EVs, data centres, telecom, and defence.

But here’s the reality check.

India is still at a very early stage. Most of the current investments are in assembly, packaging, or design. The real test will be execution. Can these fabs be completed on time? Can supply chains for chemicals, gases, and equipment be built locally? Can India move beyond being a support player and actually produce chips at scale?

There are also cost challenges. Building and running fabs requires massive water, power, and precision infrastructure. Talent is another bottleneck. While India has strong design engineers, large-scale semiconductor manufacturing needs specialised skills that take time to develop.

That’s why the government is already moving to phase two. The next version of the semiconductor mission is focusing on equipment, materials, and intellectual property. Because building fabs is just step one. Owning the ecosystem is where the real value lies.

So what we’re seeing right now is not a finished story. It’s the beginning of one.

India isn’t replacing Taiwan or South Korea anytime soon. But it’s positioning itself as a credible alternative in a world that no longer wants to depend on just one region for chips.

And if even a part of this $15 billion pipeline translates into real output, India’s role in the global tech supply chain could look very different over the next decade.