In April 2026, dealers, who just a few months ago were drowning in unsold cars, suddenly found themselves with far less stock than they were used to.

Data from the Federation of Automobile Dealers Associations shows that passenger vehicle inventory at dealerships has dropped to roughly 27 to 29 days by February 2026 and about 28 days by March. A year ago, that number was sitting above 50 days. That is a complete reset of how cars are moving through the system.

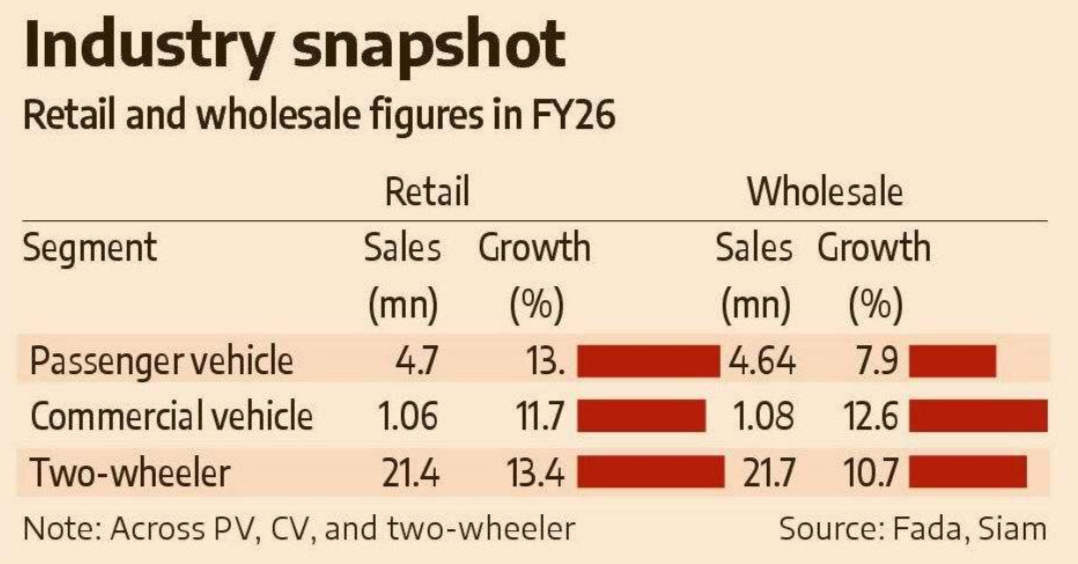

At the same time, retail sales surged ahead. In FY26, India sold about 4.7 million passenger vehicles at the retail level, a solid 13% jump year on year. But here’s where it gets interesting. Wholesale dispatches, the number of cars manufacturers send to dealers, only grew 7.9% to around 4.64 million units.

So cars are being sold to customers faster than they are being shipped to dealerships. That gap is what drained the excess inventory and flipped the market narrative.

At the start of 2025, the market was dealing with a completely different problem.

Back then, dealers were sitting on piles of unsold inventory. In April 2025, inventory was already around 50 days. By May, it crept up to 52 or 53 days, and through June and July it stayed elevated near 55 days. That is a stressful place to be if you are a dealer because every extra day a car sits unsold, it eats into your margins.

To clear stock, dealers were offering discounts, bundling offers, and in some cases pushing sales just to reduce inventory pressure. At the same time, entry-level demand was weak and financing was not exactly easy, especially outside big cities.

That is why even rating agencies got cautious. ICRA, for instance, cut its FY26 passenger vehicle wholesale growth forecast to just 1-4% because of high inventory and even flagged supply-side risks like shortages of rare-earth magnets, which are crucial for electric vehicles and certain components. So the industry was stuck in a weird place where demand existed but the system was clogged with excess supply.

Then the clean-up began.

By December 2025, inventory had dropped to about 37 to 39 days. By January 2026, it was down to 32 to 34 days. And by February, it had reached that healthier 27 to 29-day range. This was not just because companies slowed dispatches.

Demand genuinely picked up, especially from rural India. In fact, rural growth outpaced urban demand during parts of this period, which is a big shift because urban markets usually lead car sales in India. Better affordability, stable financing conditions, and a steady pipeline of new launches all played a role.

March 2026 then sealed the story.

Retail passenger vehicle sales for that month alone hit around 4,40,000 units, one of the strongest monthly numbers on record. Across all vehicle categories, India clocked nearly 3 crore units in total retail volumes in FY26.

On the manufacturing side, the Society of Indian Automobile Manufacturers reported total domestic wholesales of about 2.83 crore vehicles across segments, marking a 10.4% increase. Even exports joined the party, rising 24% to a record 66.4 lakh units, the fastest growth seen in seven years.

But when retail grows faster than wholesale, it also means the system is running tighter. There is less buffer stock sitting with dealers. That also means any disruption in production or supply chains can quickly show up as shortages in showrooms.

The industry has flagged potential risks from geopolitical tensions in West Asia, which could impact supply chains and logistics costs. Earlier concerns about rare-earth magnet shortages have not completely disappeared either.

If key components become scarce, manufacturers may not be able to keep up with demand, which could slow down sales or push up costs.

Margin-wise volume growth does not always translate into profit growth.

Automakers may sell more cars, but if input costs rise or if they have to offer incentives to sustain demand, margins can get squeezed. In fact, early expectations for FY26 suggest revenue growth for auto companies could be in the 17-20% range, driven by volume expansion, but profitability may not keep pace.

But that’s not the only thing changing right now.

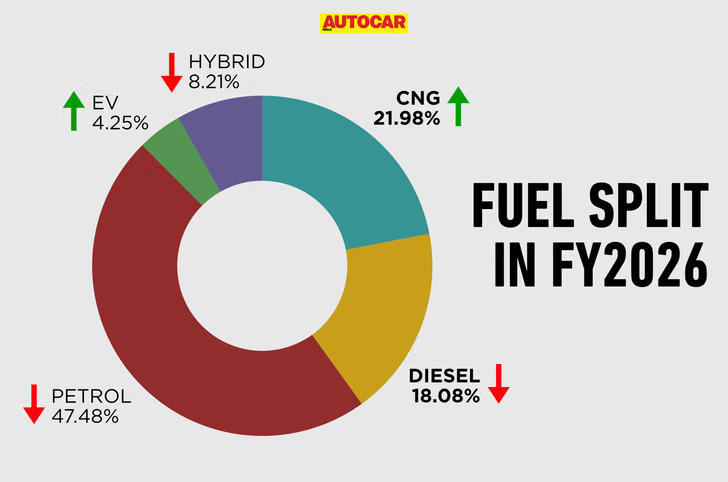

The type of cars people are buying is evolving. Petrol still dominates, but its share is slowly declining. In April 2025, petrol cars made up about 50% of sales. By FY26, compressed natural gas vehicles had grown to over 21% share, and by March 2026 they were close to 24%.

Image source: Auto Car India

Electric vehicles are still a small slice, but their share has risen from around 3.5% to just over 5% in a year. Hybrids are also gaining traction. So the market is not just growing, it is diversifying.

In 2025, the story was about excess supply, rising dealer stress, and muted wholesale growth. In 2026, the story has shifted to strong retail demand, healthier inventory levels, and a more disciplined supply approach by manufacturers. But the new challenge is not about selling cars. It is about making sure there are enough cars to sell without letting costs spiral or margins shrink.

So the market has not become simpler, it has just changed its problem statement.

Earlier, the industry was asking how to clear unsold cars. Now it is asking how to keep up with demand without running into supply bottlenecks or profitability issues. And that shift tells you one thing clearly.

India’s auto market is no longer struggling with demand. It is now learning how to manage growth.