2026 has been one of those years for India’s IT sector that leaves you squinting at the scoreboard, unsure whether to cheer or worry.

On the surface, things have felt a bit uncomfortable.

Indian IT stocks have been under pressure, and not without reason.

The trigger this time came from the US, where Anthropic rolled out new AI tools designed specifically for corporate legal teams.

These tools can draft, review, and manage legal documents, which immediately raised a familiar fear. If AI can do this, what else can it replace next?

Markets reacted fast, and Indian IT stocks felt the heat.

But here’s where the story gets more interesting. If you zoom out from stock prices and look at brand strength and global relevance, India’s IT giants are still very much in the game.

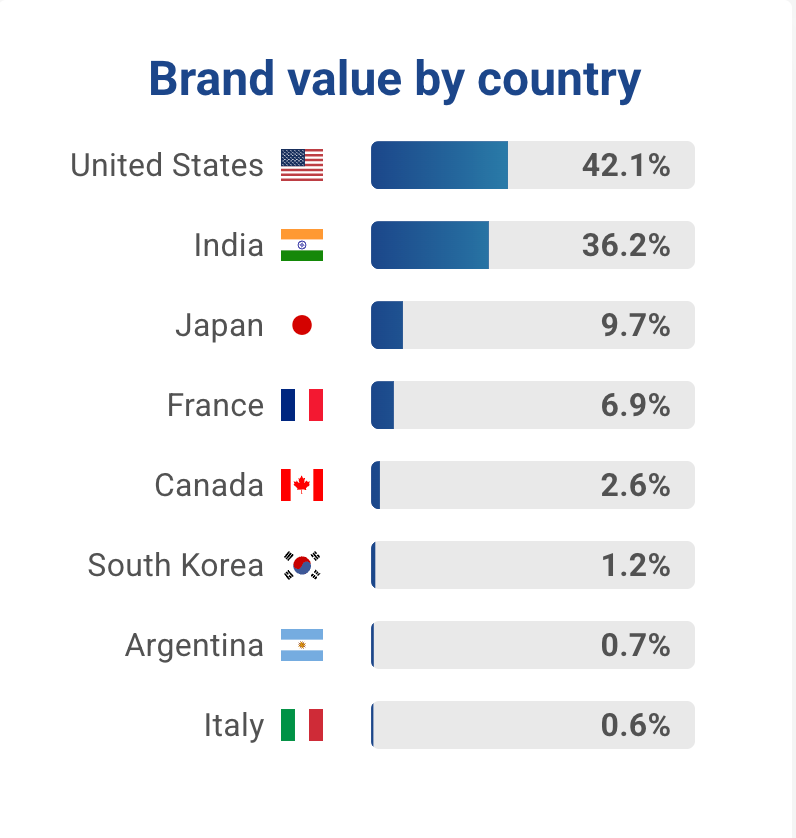

According to Brand Finance, the combined brand value of the world’s top 25 IT services companies has climbed to $167.2 billion.

That is a big number, especially when you consider the noise around automation and AI replacing services. Even more telling is that 18 of these 25 brands actually increased in value. In a world obsessed with cutting costs through technology, IT services are clearly not going out of fashion anytime soon.

Breaking it down for you:

Sitting comfortably at the top is Accenture, once again.

For the eighth straight year, it remains the world’s most valuable IT services brand.

In 2026, its brand value rose 2% to $42.3 billion. Accenture has leaned hard into AI, digital transformation, and deep client relationships across industries and geographies. It is less about chasing trends and more about embedding itself into how companies actually run.

It also happens to be the strongest IT services brand globally for the second year running, with a Brand Strength Index score of 90.7 out of 100 and an AAA+ rating.

That score reflects trust, reputation, and reliability, the kind of things that do not show up in quarterly earnings but matter deeply over decades.

But let’s bring it back to India. Accenture may be leading the race, but Indian IT companies are right up there, not watching from the sidelines.

Tata Consultancy Services holds on to second place globally, with a brand value of $21.2 billion, a position it has defended for five straight years.

In FY2025, TCS crossed nearly $30 billion in annual revenue, firmly placing it among the world’s largest IT services companies. Its growth engine looks familiar by now.

AI, cloud services, and cybersecurity are doing the heavy lifting, supported by new AI labs, centres of excellence, and delivery centres.

What’s equally interesting is how TCS has built its brand outside boardrooms and balance sheets.

Infosys comes in third globally, with a brand value of $16.4 billion. It also holds a quieter but impressive title. It has been the fastest-growing IT services brand over the past six years, clocking a compound annual growth rate of 15%.

That tells you something important. Even as technology cycles shorten and competition intensifies, Infosys has managed to keep expanding its brand relevance.

HCLTech sits in eighth place, with brand value inching up 1% to $9.0 billion from $8.8 billion last year. The company has stayed focused on engineering services, cloud, and digital infrastructure, areas where client relationships tend to be sticky and long-term.

Wipro rounds out the Indian presence in ninth place. Its brand value rose 4% to $6.3 billion, helped by gradual gains from cloud, cybersecurity, and enterprise transformation services.

Let the numbers do the talking.

Now, step back even further, because the brand story is just one layer of a much bigger picture.

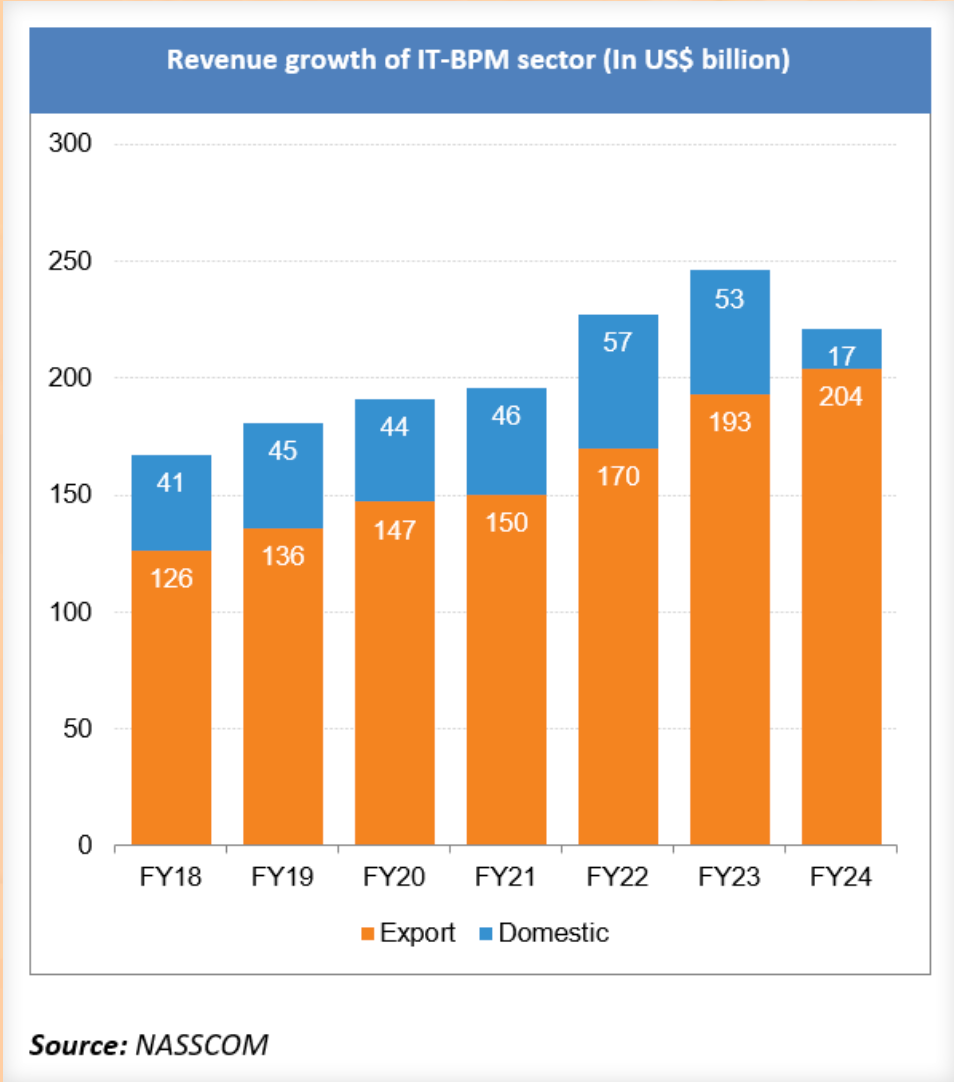

According to NASSCOM, India’s IT industry revenue has expanded from $118 billion in FY15 to an estimated $283 billion in FY25. Exports alone now account for $224 billion of that.

IT exports grew 12.48% in FY25, and services continue to dominate, contributing over 65% of total IT exports. These are not the numbers of an industry in decline.

What is changing, though, is where this growth is coming from.

For years, Bengaluru, Hyderabad, and NCR were the default centres of gravity. That is no longer the case. Non-metro cities like Udaipur, Vizag, Coimbatore, and Nagpur recorded over 50% IT hiring growth in the first half of 2025. Compare that with 12 to 15% growth in Bengaluru and NCR, and you start to see a structural shift taking shape.

These tier-II and tier-III hubs are attracting work in AI, cloud, and cybersecurity while offering cost savings of around 30%. For companies under pressure to protect margins, that matters a lot.

The domestic market is also pulling its weight. IT spending in India grew 11.1% in 2024 to $138.6 billion and is expected to reach ₹15.1 lakh crore in 2026. Data centres and AI-enabled software are driving much of this demand.

Put all of this together, and a pattern emerges. India remains the world’s preferred offshoring destination, trusted for scale, cost efficiency, and delivery. At the same time, it is entering a new phase where AI, cloud, cybersecurity, and data engineering are no longer add-ons but core capabilities.