A few weeks ago, India's stock market crossed another milestone. The National Stock Exchange's unique investor base surpassed 13 crore people, adding one crore investors in just seven months. Demat accounts have crossed 21 crore. Mutual fund SIP contributions continue to hit record highs month after month.

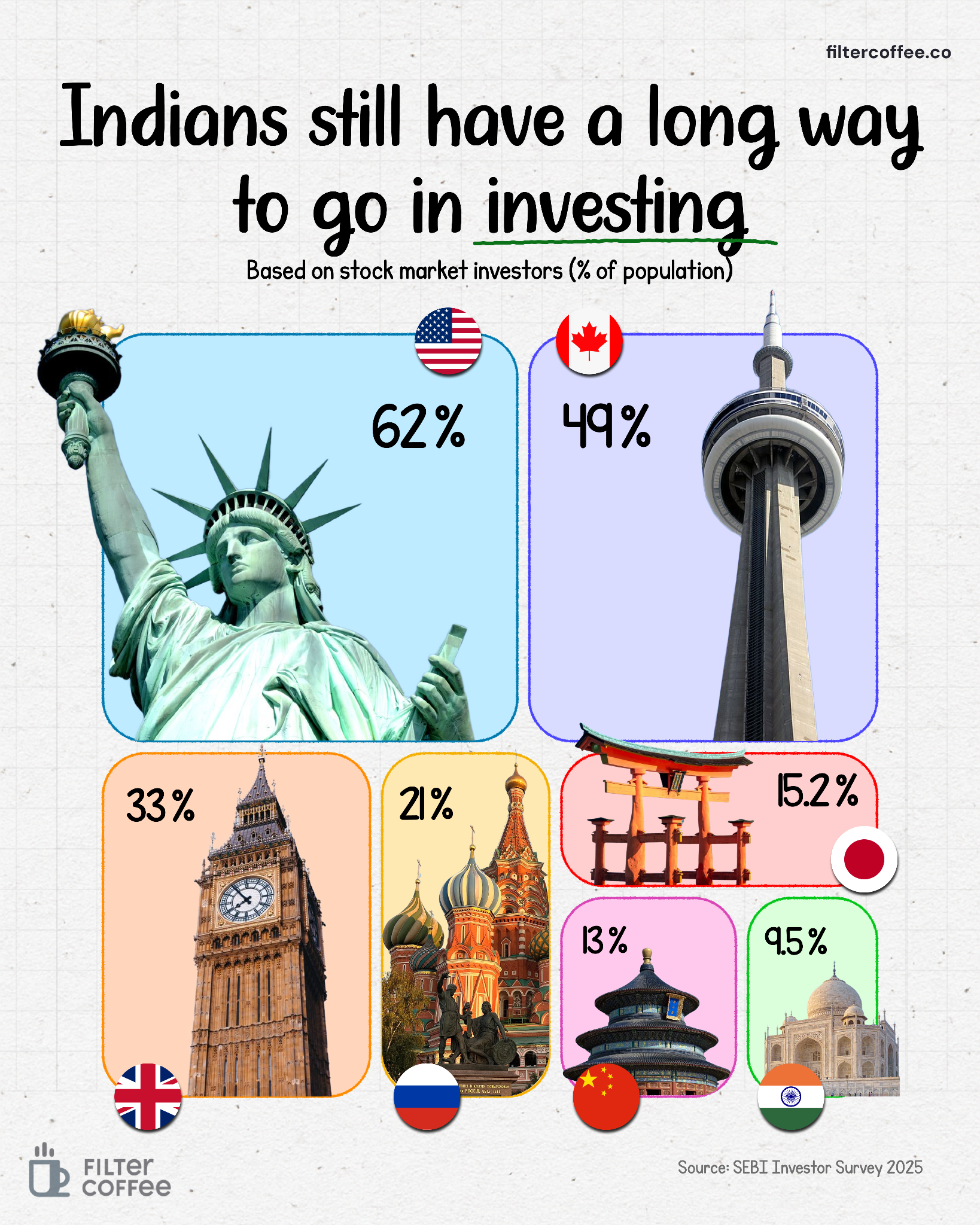

However, according to SEBI's Investor Survey 2025, only 9.5% of Indian households participate in securities markets. In comparison, stock market participation stands at around 62% in the United States, 49% in Canada, and over 30% in the United Kingdom.

But why?

The truth is that India is simultaneously experiencing two seemingly contradictory realities. The stock market has never been more popular. Yet most Indians still do not invest in it.

To understand why, let’s first understand how Indians have traditionally managed their money.

For decades, the average Indian household viewed savings and investing as two different things. Savings meant safety. Investing meant risk. Most families preferred bank fixed deposits, gold, land, insurance policies, or simply cash savings. These assets may not always generate the highest returns, but they offer something Indians value deeply: certainty.

SEBI's survey found that nearly 80% of households prioritize capital protection over wealth creation. In simple terms, most people would rather earn a lower return and sleep peacefully than chase higher returns with uncertainty attached.

This mindset did not emerge out of nowhere.

India is still a relatively young economy in terms of household wealth. Unlike the United States, where generations have accumulated wealth through pensions, retirement funds and stock ownership, a large section of Indian households are still focused on building financial security first. When your primary goal is buying a home, funding education, handling medical emergencies or supporting family members, preserving money often feels more important than multiplying it.

There is also the issue of income.

While India's economy has grown rapidly, a large percentage of households still have limited surplus income available for long-term investing. Before someone can invest in equities, they need disposable income after paying for essentials. For millions of families, that surplus remains small or inconsistent.

Today, the barriers that kept people away from investing are slowly disappearing.

Ten years ago, opening a demat account involved paperwork, physical forms and multiple visits. Today it can be completed in minutes through a smartphone. Brokerage costs have collapsed. Financial information is available through YouTube, Instagram, podcasts and investing apps. UPI has familiarized millions of Indians with digital financial transactions.

The result is visible everywhere.

India added roughly 2.35 crore demat accounts during FY26 up to December 2025. Unique demat investors crossed 12 crore by September 2025 and continued rising thereafter. Mutual funds have also expanded far beyond major metros. More than 3.5 crore mutual fund investors now come from smaller cities and towns rather than India's largest urban centres.

India's investing story is no longer limited to Mumbai, Delhi or Bengaluru. The next wave of investors is emerging from Indore, Surat, Lucknow, Coimbatore, Bhubaneswar and hundreds of smaller towns that barely featured in financial conversations a decade ago.

At the same time, awareness remains much higher than participation.

SEBI found that around 63% of households are aware of at least one securities market product, yet only 9.5% actually invest. Many people understand what stocks are. Far fewer understand how to build a diversified portfolio, stay invested during market crashes, or separate investing from speculation.

The rise of social media has helped spread awareness, but it has also created a flood of questionable advice, unrealistic return expectations and short-term trading behaviour.

This is where India's investing journey becomes particularly fascinating.

The country is not suffering from a lack of interest. It is going through a transition. Millions of people are moving from physical assets to financial assets for the first time. They are learning how markets work, making mistakes, discovering mutual funds, experimenting with SIPs and gradually becoming comfortable with risk.

In many ways, India's current position resembles the early stages of investing cultures seen in developed markets decades ago. The difference is that India is doing it at internet speed.