For a country that can split a restaurant bill in three seconds, scan a QR code at a roadside tea stall, and send money across the country instantly, we're surprisingly uneven when it comes to understanding what happens after the money reaches our bank account.

One of the easiest mistakes to make in India today is assuming that the people around you represent the country.

Spend enough time in Mumbai, Bengaluru, Hyderabad or Delhi and it starts to feel like everyone invests. Somebody is always talking about a SIP, discussing a market correction, or sharing a stock tip that they're convinced will double in the next year. Finance creators are everywhere, mutual fund ads seem impossible to avoid, and investing has become a regular topic of conversation.

In actual, the data reveals that we’re living in a ‘convenient bubble’

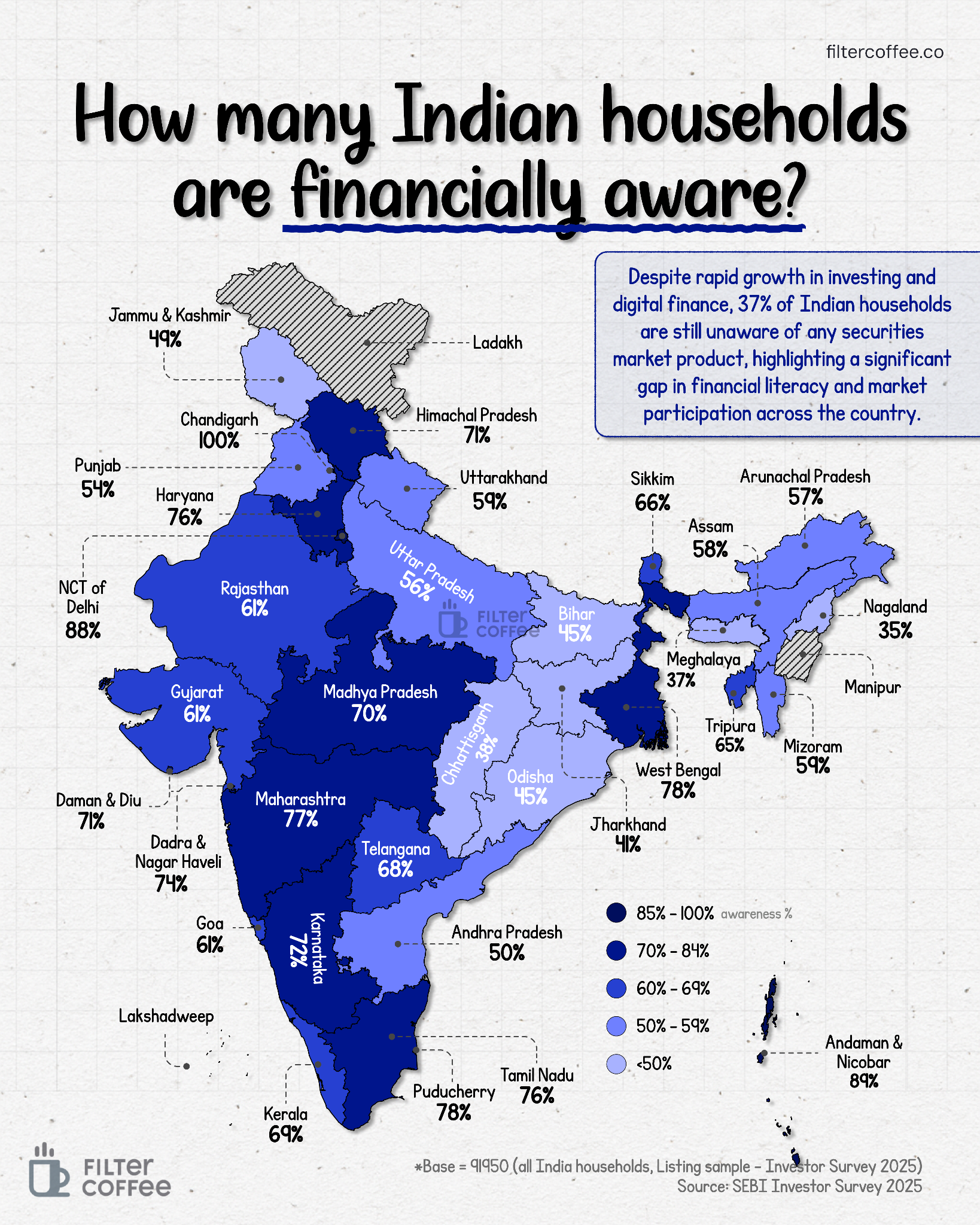

According to SEBI's 2025 Investor Survey, 37% of Indian households are unaware of any securities market product. Not uninterested. Not actively avoiding them. Simply unaware.

The state-wise numbers make the picture even more interesting. Chandigarh reported 100% awareness, while Delhi stood at 88%. Meanwhile, states such as Nagaland, Meghalaya, Jharkhand and Chhattisgarh reported awareness levels below 40%.

Most people don't learn about mutual funds because they decide to spend a weekend studying financial markets. They learn because someone around them talks about it. A colleague mentions their SIP. A friend explains tax-saving investments. A family member opens a Demat account. Over time, investing becomes familiar.

That's why awareness tends to be higher in places with larger urban centres, stronger financial ecosystems and greater exposure to formal employment. The more these conversations happen, the more knowledge spreads.

What's interesting is that India has done an incredible job improving financial access. We can move money faster and more easily than ever before.

But access and awareness aren't the same thing.

The next phase of India's financial journey may not be about helping people move money. It may be about helping more people understand what they can do with it once they have it.