Rubber is not a sexy commodity. It does not trend on LinkedIn. It does not get policy pressers or valuations. But in FY25, while India was busy talking about AI, EVs and semiconductors, rubber had a quietly solid year. One that did not make noise, but did something more important. It strengthened the foundation of an industry India cannot function without.

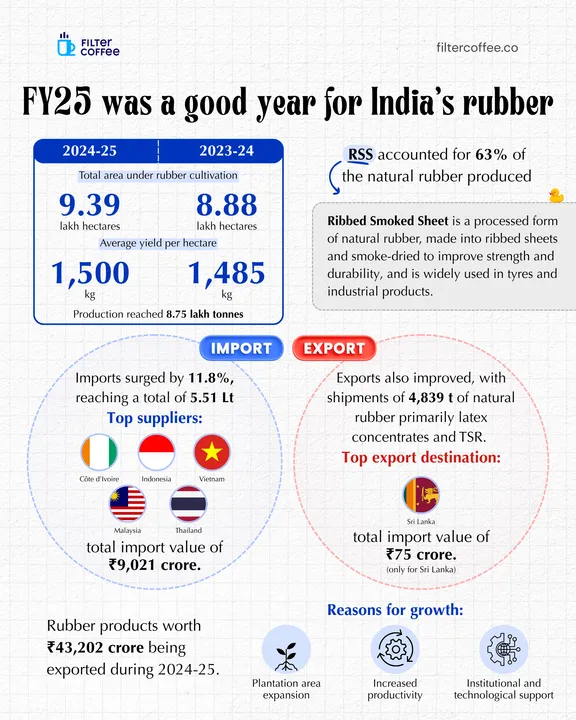

Start with the basics. In 2024–25, India expanded the area under rubber cultivation to 9.39 lakh hectares, up from 8.88 lakh hectares the year before. And in agriculture, such land expansion is never casual. It signaled that farmers believe the economics will hold up long enough to justify tapping trees that take years to mature.

Yield improved too, nudging up to 1,500 kg per hectare from 1,485 kg.

If you put it together, the total production reached about 8.75 lakh tonnes. That is not record-breaking in global terms, but for India, it is a steady climb in the right direction.

What India produces also matters.

Nearly 63% of natural rubber output came from RSS, or Ribbed Smoked Sheet. This is not raw latex straight from the tree. RSS is processed, smoke-dried, tougher, more durable and most importantly, trusted by tyre makers and industrial buyers.

If tyres are the backbone of mobility, RSS is the muscle fibre inside them. The dominance of RSS tells you something important. India is not just growing rubber. It is growing the kind the industry actually wants.

But here is where the story gets interesting.

Despite higher production, imports surged. In FY25, India imported 5.51 lakh tonnes of natural rubber, up 11.8%. The top suppliers come from Côte d’Ivoire in Africa, Indonesia and Vietnam from Southeast Asia, along with Malaysia and Thailand. The total import bill came to ₹9,021 crore.

This is because Indian demand is massive.

India consumes far more rubber than it produces. Tyres alone account for the bulk of demand, driven by passenger vehicles, trucks, buses, two-wheelers and now EVs. If you also include medical gloves, industrial belts, hoses and footwear, the gap is too big to ignore.

Domestic production is growing, but consumption has run ahead. Imports are like a pressure valve.

Exports, on the other hand, are small but improving. India shipped out about 4,839 tonnes of natural rubber in FY25, mainly latex concentrates and TSR. Sri Lanka emerged as the top destination, with exports valued at roughly ₹75 crore. The number signals India as cautiously re-entering export markets, especially for processed grades.

However, the real flex is rubber products exports touched ₹43,202 crore in FY25. This includes tyres, auto components, industrial goods and medical products. In other words, India may import raw rubber, but it exports value-added rubber at scale. This is classic Indian manufacturing behaviour. Buy raw, process smartly, sell finished.

So what changed under the hood?

Well, plantation expansion, productivity gains and institutional plus technological support. That last part is doing a lot of heavy lifting.

Over the past few years, the government has quietly rebuilt its approach to rubber.

There is a multi-year national scheme running till FY28 with a total outlay of nearly ₹14,900 crore. The focus is not just subsidies. It is productivity, processing quality, sustainability and market access. This matters because global rubber trade is getting stricter.

Europe, for instance, is rolling out deforestation-linked regulations. Buyers increasingly want traceable, certified rubber. India saw this coming.

The Rubber Board launched iSNR, or Indian Sustainable Natural Rubber, to certify origin and sustainability. It also rolled out digital platforms like INR Konnect to match growers with managed plantations and improve tapping efficiency. Geo-mapping of plantations is underway. This is boring tech, but it is the kind that keeps exports alive.

There is also a geographic shift happening. Kerala still dominates rubber, but growth is slowly moving into the North East, especially Tripura. Land availability, policy focus and diversification away from traditional crops are pulling rubber eastward. This reduces concentration risk and expands national capacity.

Challenges:

Weather volatility continues to hit yields. Price cycles are unpredictable. Small growers still struggle with income stability. And the production-demand gap is real. India consumes well over 14 lakh tonnes of rubber annually, far above what it produces. Imports are not going away anytime soon.

India is slowly moving from being a price-taker in raw rubber to a system-builder in rubber manufacturing.

FY25, then, was not just a good year. It was a telling year.

A year where higher acreage met better yields. Where RSS dominated output. Where imports rose but exports of finished goods quietly dwarfed raw trade. And where institutions finally started playing long-term chess instead of short-term patchwork.

Rubber will probably never trend on social media. But if you care about mobility, manufacturing, exports and rural livelihoods, this slow, sticky commodity is doing more heavy lifting than it gets credit for.

And India, for once, seems to be playing the long game right.