India has exported plenty of things over the years.

Engineers to Silicon Valley. Bollywood to the Middle East. Yoga to almost every country on Earth. Even chai has found fans far beyond India's borders.

Now, India is exporting something far less visible but potentially far more powerful: the technology that moves money.

This week, Greece became the latest country to accept India's Unified Payments Interface (UPI). A few months earlier, Indian tourists were paying with UPI at the Eiffel Tower and Galeries Lafayette in France. These are all part of India's attempt to take its homegrown payments system global.

India isn't just exporting an app. It's exporting trust, standards and digital infrastructure.

To understand why this matters, let's rewind a decade.

Back in 2016, India launched UPI to solve a uniquely Indian problem. Digital payments were fragmented. Bank transfers were cumbersome. Card acceptance was patchy, especially for small merchants. Cash dominated everyday transactions.

UPI changed that by allowing anyone with a bank account and a smartphone to send or receive money instantly using a simple QR code or mobile number. What made it remarkable wasn't just the technology. It was the fact that it worked across banks, payment apps and merchants on a common, interoperable network built by the National Payments Corporation of India (NPCI).

The timing couldn't have been better. Cheap smartphones, affordable mobile data after Jio's entry, Aadhaar-enabled bank accounts and the government's push towards digital payments after demonetisation accelerated adoption.

The result has been extraordinary.

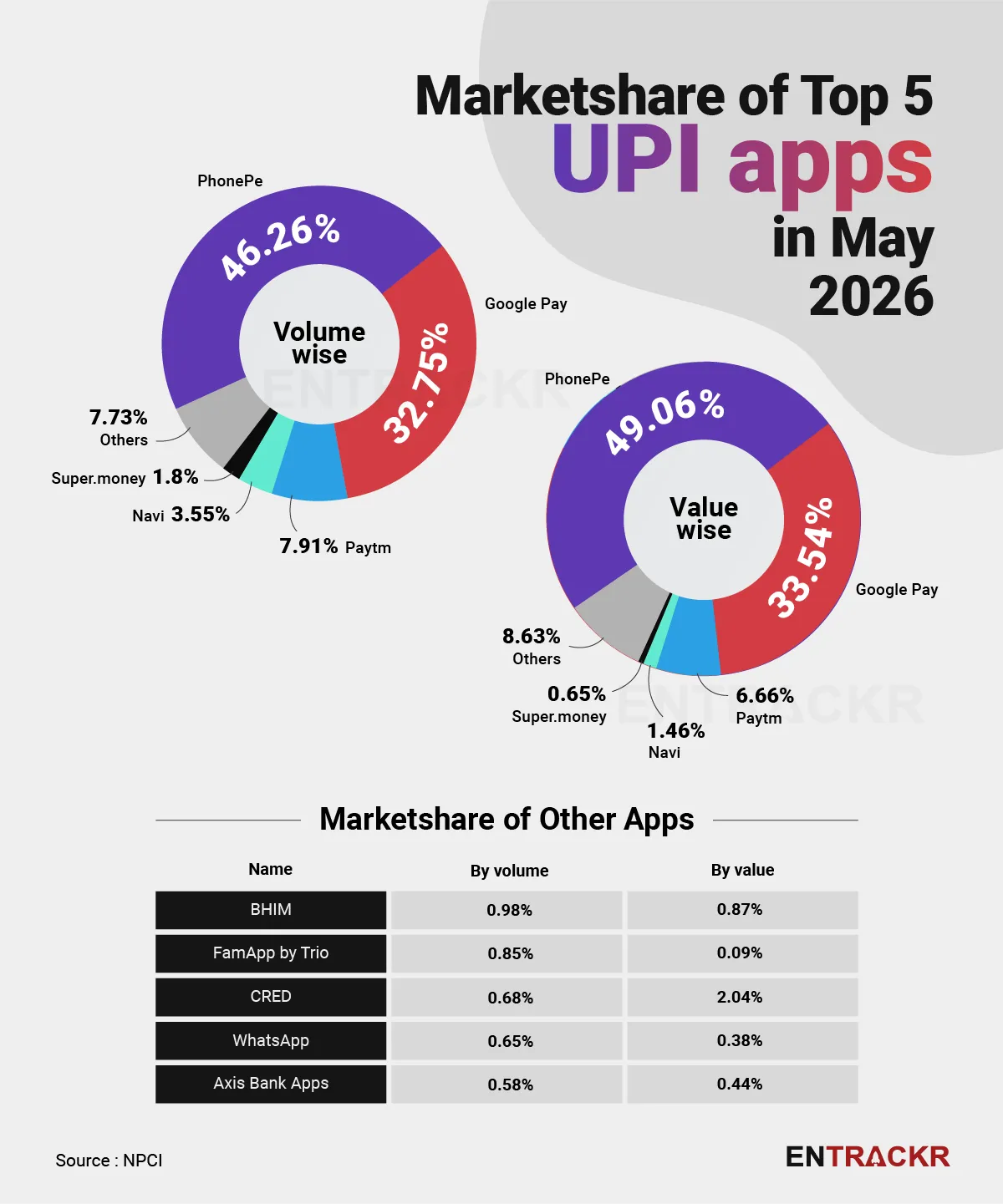

UPI today processes well over 18 billion transactions every month, with monthly transaction values crossing ₹29 lakh crore. According to NPCI, more than 650 banks are now live on the platform, while payment apps such as PhonePe, Google Pay, Paytm, BHIM and others have made QR code payments a part of everyday life. From buying vegetables to paying school fees, UPI has become India's default payment method.

But success at home naturally raised a bigger question. Could India export this model?

The answer appears to be yes.

With Greece joining the network, UPI is now accepted across ten countries, including Singapore, the UAE, France, Mauritius, Nepal, Bhutan, Sri Lanka, Qatar and Cambodia. Rather than replacing local payment systems, NPCI International Payments Limited (NIPL) works with banks and payment providers in each country to enable UPI payments for Indian users.

In Greece, that partner is Eurobank.

The immediate benefit is convenience. Indian travellers can increasingly pay overseas using the same apps they use at home instead of relying entirely on international cards or carrying large amounts of cash. Over time, this could also reduce transaction costs for merchants and improve payment efficiency.

But if this were only about tourists, governments wouldn't be paying so much attention.

The real story is Digital Public Infrastructure, or DPI.

Think of DPI as the digital equivalent of roads, railways or electricity networks. It is the invisible infrastructure that allows citizens to prove their identity, move money, access documents and interact with public services securely.

India has spent the last fifteen years quietly building one of the world's largest digital public infrastructure ecosystems.

Aadhaar provides digital identity for more than 1.4 billion people. UPI powers real-time payments. DigiLocker stores official documents digitally. FASTag enables electronic toll collection. The Account Aggregator framework allows secure sharing of financial data with user consent. ONDC is attempting to create an open network for digital commerce.

Together, these systems form what is popularly known as India Stack.

Unlike proprietary technology owned by a private company, much of India Stack operates on open standards. That means other countries can study, adapt and even deploy similar systems for their own citizens.

In fact, several countries across Asia, Africa and the Middle East have already expressed interest in different parts of India's digital public infrastructure. India has also signed multiple memorandums of understanding with foreign governments to share expertise on digital identity and payments.

This is where UPI becomes something much bigger than a QR code.

Historically, countries projected influence by exporting products, culture or technology. The United States exported Silicon Valley, Hollywood and the dollar. Japan exported automobiles and electronics. South Korea exported semiconductors and K-pop.

India has traditionally exported software services, pharmaceuticals, textiles, yoga and skilled professionals.

Today, it is adding digital infrastructure to that list.

And that creates an interesting form of soft power.

When another country adopts an Indian payment standard, integrates with India's financial infrastructure or studies India Stack while designing its own digital systems, India's influence grows without exporting a single physical product.

There is another reason countries are interested.

Indian travellers are becoming increasingly important.

India is one of the world's fastest-growing outbound tourism markets. Millions of Indians travel overseas every year for leisure, education, business and medical tourism. According to government estimates, outbound travel from India is expected to grow steadily over the coming decade as incomes rise and passport ownership expands.

For retailers, hotels, airports and tourist destinations, accepting the payment method Indian travellers already use makes commercial sense.

That said, UPI's global journey is still in its early stages.

Acceptance remains limited to participating merchants. International credit and debit cards continue to enjoy far wider acceptance. Building a payment network isn't simply about signing agreements with governments or banks. It requires thousands of merchants to install systems, educate staff and encourage customers to use them.

Cross-border settlements, foreign exchange regulations and local compliance requirements also make international payments significantly more complex than domestic ones.

Every new partnership expands India's digital footprint. Every merchant that displays a UPI QR code abroad makes Indian payments a little more familiar. Every country that integrates with India Stack validates the idea that technology built for India's scale can solve problems elsewhere too.

For decades, India's biggest technology export was the people who built software for the world.

The next chapter could be about exporting the software itself.