India’s quick commerce race just hit a new gear.

In early 2026, Eternal (the parent of Blinkit) revealed that its quick-commerce business had, for the first time, overtaken its food delivery arm in quarterly order value. Around the same time, Swiggy’s Instamart crossed ₹5,600 crore in quarterly gross order value, growing over 100% year-on-year.

And Zepto, the youngest, filed for what could be a ₹11,000 crore IPO. This a signal that quick commerce in India has moved from experiment to economic engine.

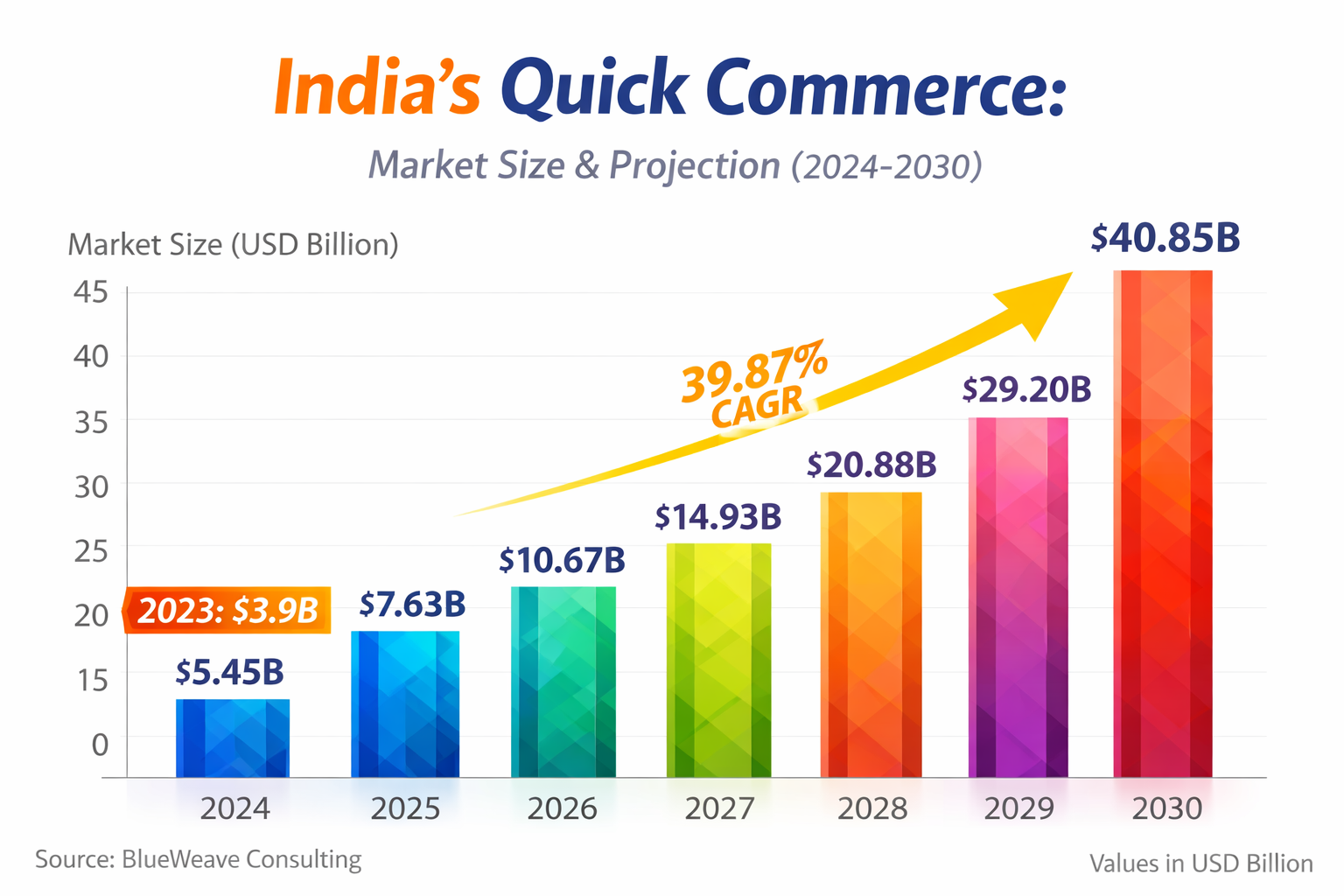

A couple of years ago, 10-minute delivery sounded like a gimmick; a convenience for urban elites ordering milk and chips. Today, it’s a serious slice of India’s $60 billion e-retail market. Estimates suggest quick commerce has already crossed $10 billion in gross merchandise value and now contributes roughly 15% of total e-commerce GMV in India. What’s more striking? The category was growing at nearly 150% year-on-year through early 2025.

So what changed?

Platforms like Blinkit and Instamart are rapidly expanding into electronics, beauty products, toys, home essentials, and even higher-ticket items. This shift is pushing up average order values and making the business more viable.

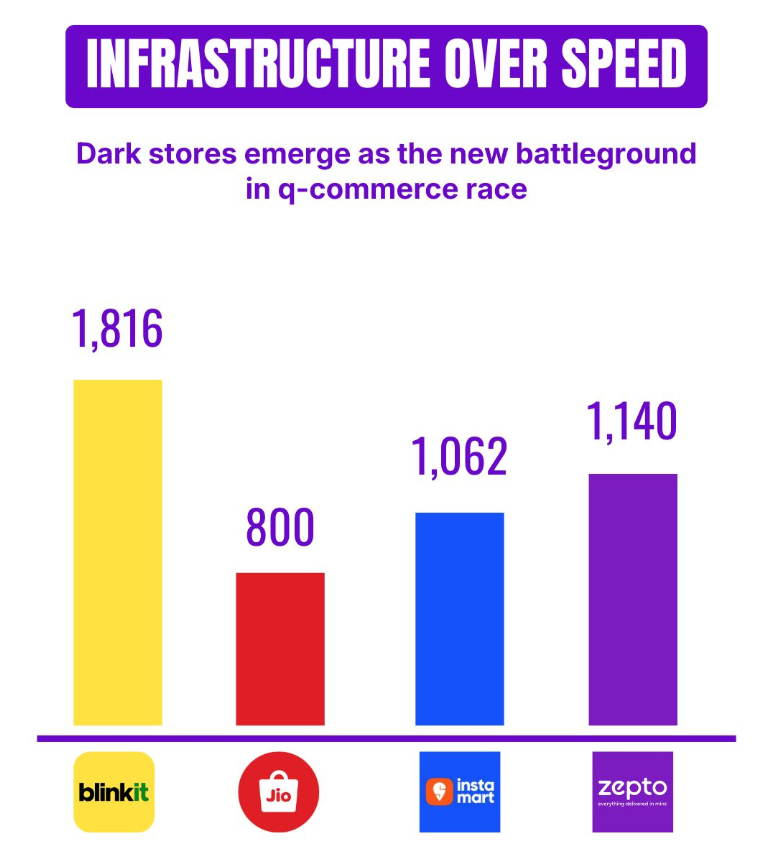

Scale is the second big story. Blinkit crossed 1,300 dark stores and is targeting 3,000 by the end of March 2027. Swiggy’s Instamart has already crossed 1,000 stores across 120+ cities. Zepto is expanding just as aggressively. These “dark stores” small warehouses optimized for fast delivery are the backbone of quick commerce. The more you have, the faster and cheaper you can deliver.

But they also require massive upfront investment, which brings us to the third layer of the story: money.

Image credit: NDTV Profit

This is a capital-heavy game. Zepto raised $450 million in 2025 at a $7 billion valuation. Eternal continues to pour resources into Blinkit. Swiggy is investing heavily in Instamart while balancing its food delivery business.

Analysts have already flagged that 2026 will likely be a year of “discovery, not profits.” In other words, the winners aren’t clear yet, and everyone is still spending aggressively to capture market share.

The competitors keep entering the market. Even Amazon has begun scaling its “Amazon Now” quick delivery service, reportedly targeting hundreds of dark stores. Flipkart is pushing its “Minutes” offering across dozens of cities. These are giants with deep pockets and existing logistics networks. Their entry ensures that competition will only intensify from here.

However, growth is still heavily skewed towards metros. While platforms now operate in over 100 cities, non-metros contribute only around 15% of quick commerce GMV. Expanding beyond large urban centers without killing margins remains a big challenge.

So where does this leave India in the global race? Interestingly, Indian companies are already among the most valuable players in the space. Blinkit’s parent, Eternal, is valued at over $25 billion, while Swiggy is not far behind. Globally, only giants like DoorDash and Meituan are ahead. That’s a remarkable shift for a market that was once seen as a follower, not a leader.

The real question now is who will dominate quick commerce in India, and whether they can turn this scale into sustainable profits. Because in this race, speed got them here. But discipline will decide who stays.