Polycab India just pulled off something that would’ve sounded improbable a decade ago. It has raced past Havells to become the new leader in consumer electricals; in market cap, revenues, and even profits.

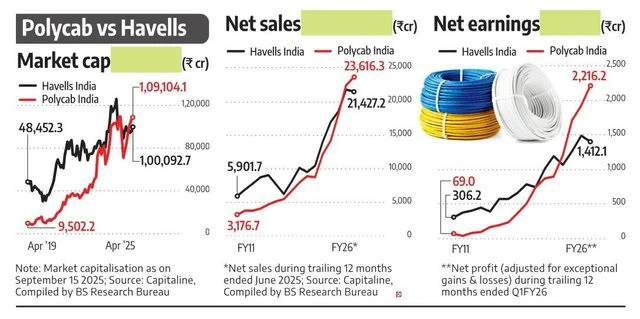

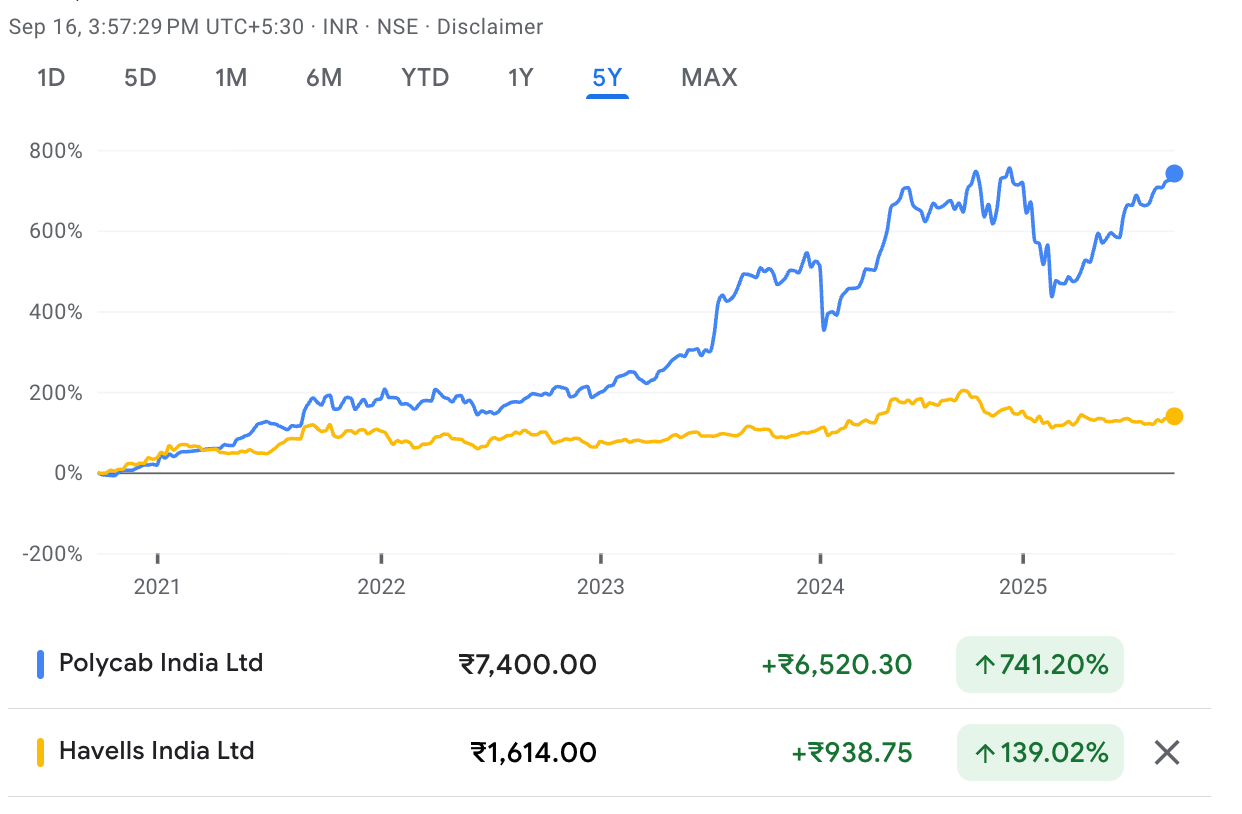

As of September 2025, Polycab’s market cap stood at about ₹1.09 trillion, nudging past Havells’ ₹1 trillion. It might look like a close fight, but this shift has been building up quietly over the years, powered by steady execution, financial discipline, and a bet that wires and cables would remain the real growth engine of India’s power story.

Let’s put the scorecard on the table.

In FY25, Polycab reported revenues of ₹22,408 crore and net profit of ₹1,930 crore. Havells, on the other hand, clocked ₹21,778 crore in revenues and ₹1,483 crore in profits. The growth trajectory is even starker when you stretch it back a few years. Between FY22 and FY25, Polycab’s sales grew at a compound annual growth rate of 22.5% and its profits at 29.3%. Havells grew too, but at a more modest 16% and 7.4% respectively.

The secret? Polycab stuck to its knitting.

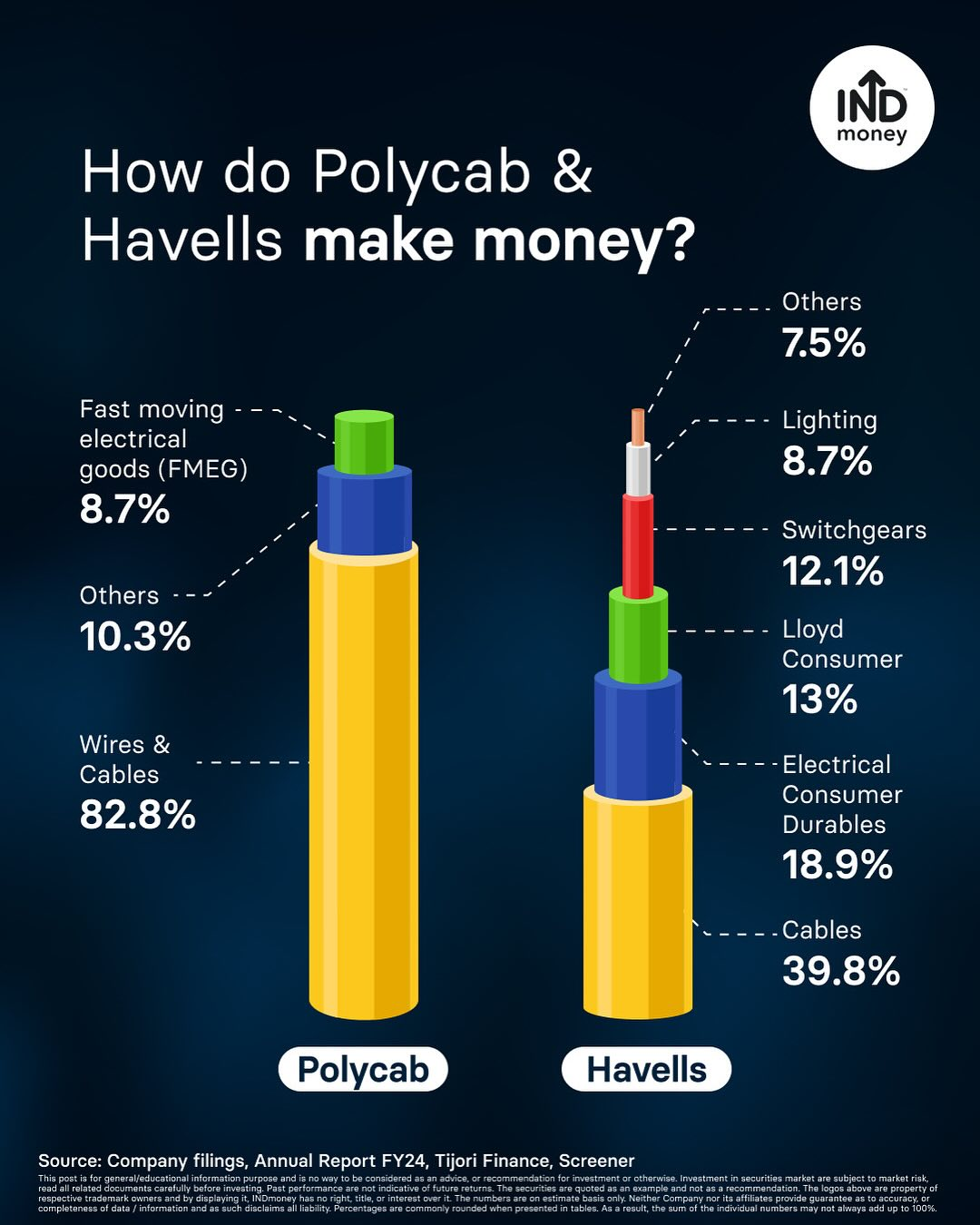

Its cables and wires business, which still makes up a chunky 85% of its revenue, kept firing thanks to government spending on infrastructure, electronics manufacturing, and some smart backward integration. Margins actually improved — rising from around 10.7% in FY19 to nearly 13% this year. And the side bet on fast-moving electrical goods finally turned a corner. After ten straight quarters of losses, the FMEG business swung into profitability in Q1FY26. That gave Polycab a new growth engine without burning cash.

Havells, in contrast, doubled down on a different bet. Back in 2017, it spent ₹1,600 crore acquiring Lloyd’s consumer durables business and has poured in another ₹2,900 crore since, hoping to transform into a full-fledged appliances player. Lloyd’s top line did expand — from ₹2,273 crore in FY22 to over ₹5,134 crore in FY25. But profitability never arrived. Margins in the division languished at just 2.3% last year, compared to the company’s overall 9.7% and its star switchgear business at 22.5%. In fact, Lloyd’s drag has steadily pulled down Havells’ consolidated margins from nearly 24% in FY19 to under 10% today.

And it isn’t just about execution. The appliances market in India is brutal. Global giants like Daikin, LG, Samsung, and Hitachi already dominate air conditioners and refrigerators. Whenever Lloyd tried to raise prices to protect margins, consumers simply switched to premium foreign brands. Add to that an unusually mild summer this year and weak consumer demand, and Havells’ Q1FY26 numbers slipped below estimates. Inventories piled up, margins contracted, and brokerages were forced to trim earnings forecasts for the next couple of years.

Polycab, on the other hand, saw analysts raise estimates. With domestic demand buoyant, infrastructure capex strong, exports picking up, and its EPC order book looking healthy, earnings got upgraded by 4% for FY27. Investors seem convinced that Polycab has momentum on its side.

That said, it’s not a clear runway. Adani and AV Birla are both gearing up to enter the wires and cables market. Given that this segment makes up the bulk of Polycab’s revenues, any price war could hit margins. Havells, with its more diversified mix, might actually be better cushioned if that happens. So while Polycab holds the crown today, the rivalry isn’t over.

For investors, the takeaway is straightforward. Polycab has earned its lead with focus and financial discipline, while Havells has been dragged down by an ambitious but unprofitable diversification. But leadership in fast-moving sectors is never permanent. The real question now is whether Polycab can defend its fortress as new entrants storm the gates, and whether Havells can stop Lloyd from bleeding away its margins.

For now though, the cables-and-wires specialist has proved that sometimes the safest bet is sticking close to the core.

FAQs

Who is the current market leader in consumer electricals in India?

As of September 2025, Polycab India has overtaken Havells to become the market leader in consumer electricals, leading in market cap, revenues, and profits.

What is Polycab India’s market capitalisation in 2025?

Polycab India’s market capitalisation stood at about ₹1.09 trillion in September 2025, slightly ahead of Havells’ ₹1 trillion.

How much revenue did Polycab India earn in FY25?

Polycab India reported revenues of ₹22,408 crore in FY25, surpassing Havells’ ₹21,778 crore for the same period.

What is Polycab India’s profit growth compared to Havells?

Between FY22 and FY25, Polycab’s profits grew at a 29.3% CAGR, while Havells’ profits grew at only 7.4% CAGR.

What drives most of Polycab India’s revenue?

About 85% of Polycab’s revenue comes from its cables and wires business, supported by infrastructure capex, electronics manufacturing, and backward integration.

Has Polycab India’s FMEG business become profitable?

Yes, after ten straight quarters of losses, Polycab’s fast-moving electrical goods (FMEG) segment turned profitable in Q1FY26.

Why are Havells’ margins declining?

Havells’ margins have fallen from 24% in FY19 to under 10% now, mainly due to losses in its consumer durables arm Lloyd, which has weak profitability.

How has the Lloyd business impacted Havells’ performance?

Lloyd’s revenue grew from ₹2,273 crore in FY22 to ₹5,134 crore in FY25, but margins stayed at just 2.3%, pulling down Havells’ overall profitability.

What risks does Polycab India face going forward?

Polycab faces rising competition as Adani Group and Aditya Birla Group plan to enter the wires and cables space, which could spark price wars and pressure margins.

What is the key takeaway for investors from Polycab vs Havells?

Polycab has surged ahead by sticking to its core business and maintaining financial discipline, while Havells has been weighed down by an unprofitable diversification into consumer durables.