A few years ago, most Indians only walked into a diagnostic lab when a doctor scribbled “CBC, lipid profile, fasting sugar” on a prescription pad. Diagnostics was a boring backend business. Functional, forgettable, and deeply local. Every neighbourhood had that one trusted pathology uncle with faded signage, a semi-working printer, and reports stapled together in transparent plastic folders.

Today, everyone wants a piece of this business.

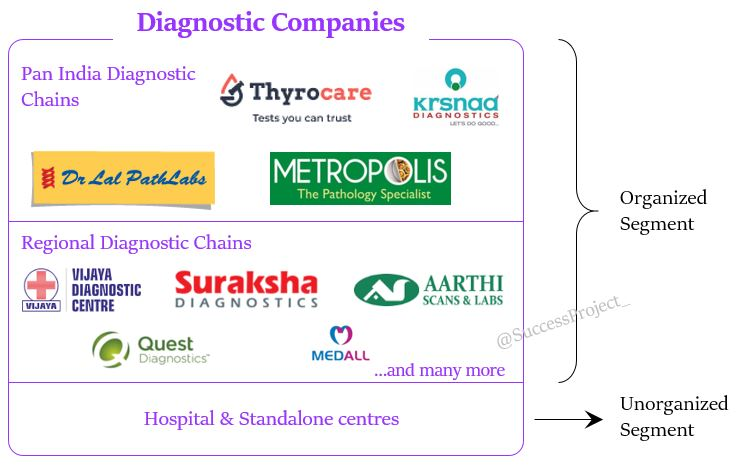

Metropolis is buying labs. Dr. Lal PathLabs is scouting for acquisitions again. Thyrocare has gone through ownership changes. PharmEasy and Tata 1mg are throwing discounts at blood tests. Amazon has entered diagnostics. Specialized cancer testing labs are getting acquired for hundreds of crores. Investors are talking about “rollups,” “hub-and-spoke efficiency,” and “preventive healthcare penetration” like diagnostics is the next big infrastructure play.

And honestly, they may not be wrong.

Because underneath the surface, India’s diagnostics industry is quietly becoming one of the most important healthcare businesses in the country.

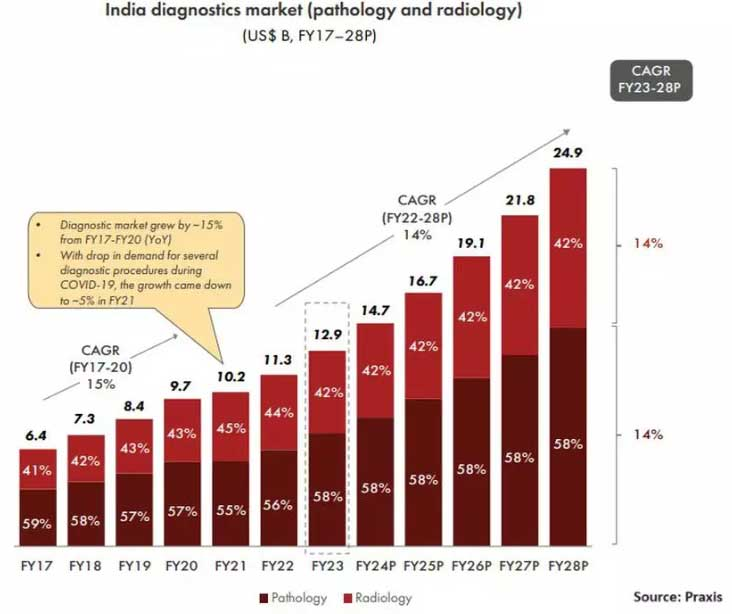

The numbers alone tell the story.

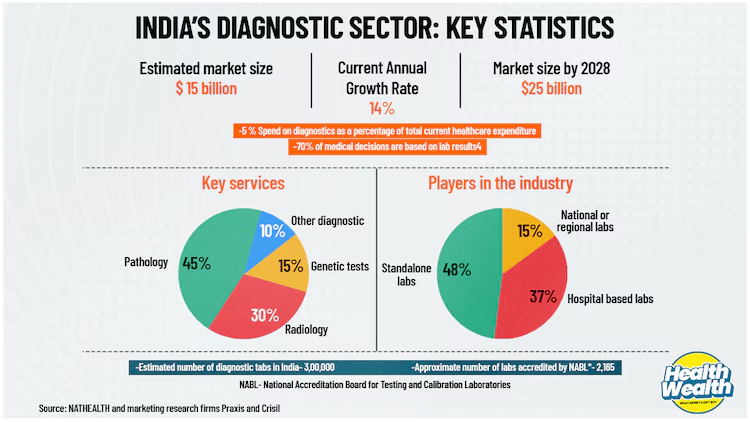

India’s diagnostics market was worth roughly ₹60,000 crore in 2020. By 2026, estimates peg it at nearly ₹1.2 lakh crore. That’s a doubling in just six years. The market is growing at around 12% to 14% CAGR, and India already conducts nearly 15 billion diagnostic tests every year.

But here’s the more interesting part.

Despite all this growth, nearly 70% of the market is still unorganized.

That means India’s diagnostics industry today looks a lot like India’s retail market did before malls and organized retail chains exploded. Or how jewellery looked before Titan scaled Tanishq. Highly fragmented. Extremely local. Built on trust instead of systems.

There are reportedly more than 1 lakh small diagnostic labs across India. Most operate within a single city or even a single locality. Many still rely on legacy machines, manual operations, paper reports, and local doctor relationships. Some don’t even have apps, websites, or digital patient records.

Meanwhile, the biggest organized chains still control shockingly tiny market shares.

Dr. Lal PathLabs, one of the largest listed players in India, reportedly has revenue of roughly ₹2,200 crore. That translates to barely 1.8% market share in a ₹1.2 lakh crore industry. Metropolis sits around ₹1,400 crore revenue and about 1.2% market share.

Thyrocare is roughly ₹700 crore. Vijaya Diagnostic is about ₹550 crore.

In other words, even the biggest players are still minnows in the broader market.

And that’s exactly why consolidation is becoming the story.

Organized chains have realized that India’s diagnostics market isn’t a winner-takes-all industry yet. It’s still early enough to build regional dominance city by city, lane by lane, collection center by collection center.

So instead of building everything from scratch, many chains are simply buying existing labs. The acquisition math looks surprisingly attractive.

A typical small unorganized lab may generate around ₹5 crore in annual revenue with EBITDA margins of 15% to 20%. That means EBITDA of roughly ₹80 lakh to ₹1 crore. Such labs are often acquired at 4x to 6x EBITDA valuations, implying acquisition costs of around ₹4 crore to ₹6 crore for a functioning business with existing patients, local doctor relationships, and geographic presence.

Then comes the real game: integration.

The organized chain usually converts the acquired lab into part of a hub-and-spoke model. Instead of running expensive testing infrastructure at every location, the local lab becomes largely a collection center. Samples move to centralized high-capacity processing labs.

This single operational shift changes everything.

Small labs usually perform all tests in-house. That means expensive equipment, duplicated infrastructure, maintenance costs, lower machine utilization, and inefficient staffing. Large chains centralize testing. A single large reference lab can process thousands of samples across cities with much higher efficiency. This reportedly cuts operating costs by 30% to 40%.

Then they expand the test menu.

A small lab may offer 200 to 300 tests. A large chain can offer 3,000 to 5,000 tests including advanced pathology, genomics, oncology panels, autoimmune testing, allergy testing, molecular diagnostics, and preventive health packages.

Suddenly, the same customer who earlier came for a ₹300 CBC test can now be sold a ₹4,000 wellness package or a ₹15,000 specialized panel.

That’s why organized players often see revenue expansion after acquisitions.

After operational integration and cross-selling, revenue may rise to ₹7 crore over a few years while EBITDA margins expand to nearly 28%. That pushes EBITDA close to ₹2 crore. In simple terms, the acquiring chain is not just buying current earnings. It is buying inefficiency that can later be optimized.

And diagnostics happens to be one of those businesses where scale really matters.

Take logistics, for example.

Dr. Lal reportedly has over 250 collection centers in Delhi alone. A small lab may have one or two centers. That density creates convenience. Patients don’t necessarily choose the “best” lab. They often choose the nearest trusted one.

Then comes the home collection.

Before COVID, home sample collection felt like a premium service. Today, it’s becoming standard urban behaviour. Many consumers now expect a phlebotomist to arrive at home within a few hours, collect blood samples, and send reports digitally.

Large chains built this infrastructure aggressively during the pandemic.

Smaller labs struggled.

And once digital habits form, switching becomes harder.

If all your reports from the last 8 years sit inside one app with trend charts, historical comparisons, and family records, moving to another lab suddenly feels inconvenient. Diagnostics starts behaving less like a transactional business and more like a sticky consumer platform. But the bigger reason diagnostics is booming is because India itself is changing.

For decades, Indian healthcare spending was largely reactive. People spent money after they got sick. Now the industry is slowly moving toward preventive healthcare.

Urban consumers increasingly do annual health checkups even without symptoms. Companies include wellness packages in employee benefits. Insurance coverage is slowly expanding. Chronic diseases are rising sharply. Fitness culture, smartwatches, and health influencers have made blood markers part of everyday conversations.

People casually discuss Vitamin D deficiency and HbA1c levels over coffee now. That simply did not happen a decade ago.

Then there’s preventive healthcare.

Urban annual health checkup penetration reportedly moved from roughly 15% in 2019 to nearly 35% by 2026. If the average preventive checkup costs around ₹3,000, the incremental market expansion becomes massive.

And India still remains deeply under-tested compared to developed markets.

India conducts roughly 10 diagnostic tests per person annually. The US does around 45. Even if India never reaches US levels, the headroom is obvious.

But the really interesting shift is happening inside diagnostics itself.

Pathology still dominates roughly 60% of the market. These are routine blood and urine tests. High volume, relatively lower ticket size, EBITDA margins around 25% to 30%. Radiology forms another 30% with X-rays, CT scans, ultrasounds, and MRIs. Lower volumes but much higher ticket sizes and often stronger margins.

Then comes the smallest but fastest-growing category: specialized diagnostics.

This includes genomics, oncology panels, advanced autoimmune testing, molecular diagnostics, and precision medicine. Tiny volume today, but margins can reportedly touch 45% to 50%.

And then there’s the regulatory wildcard.

Unlike medicines, diagnostic pricing in India still doesn’t face heavy centralized regulation. But fears remain that authorities could eventually cap pricing for common tests, especially if healthcare inflation becomes politically sensitive.

In many ways, diagnostics is becoming a fascinating hybrid industry.