The last thing most people expect in 2026 is an ATM running out of cash.

After all, this is the country that built UPI, processes billions of digital transactions every month, and has become a global case study in digital payments. If anything, many assumed ATMs would gradually become less relevant as QR codes and smartphones took over.

Yet India's ATM industry is now warning that cash machines across parts of the country could face disruptions because they simply aren't getting enough cash to load into them.

That's not speculation. The Confederation of ATM Industry (CATMi), the body representing ATM operators, cash logistics firms, white-label ATM companies and cash replenishment providers, recently alerted the Indian Banks' Association (IBA) that ATM services could be affected due to difficulties in obtaining cash from bank branches and currency chests.

The numbers are striking.

In March 2026, ATM operators needed around ₹94,000 crore to replenish cash machines across the country. They received only ₹61,000 crore. In April, they again required roughly ₹94,000 crore but received just ₹54,000 crore. That means fulfillment levels fell to 64% in March and 57% in April.

Naturally, this raises a simple question.

How can India have a cash shortage at ATMs when the country has more cash in circulation than ever before?

Because the truth is that India is not running out of cash.

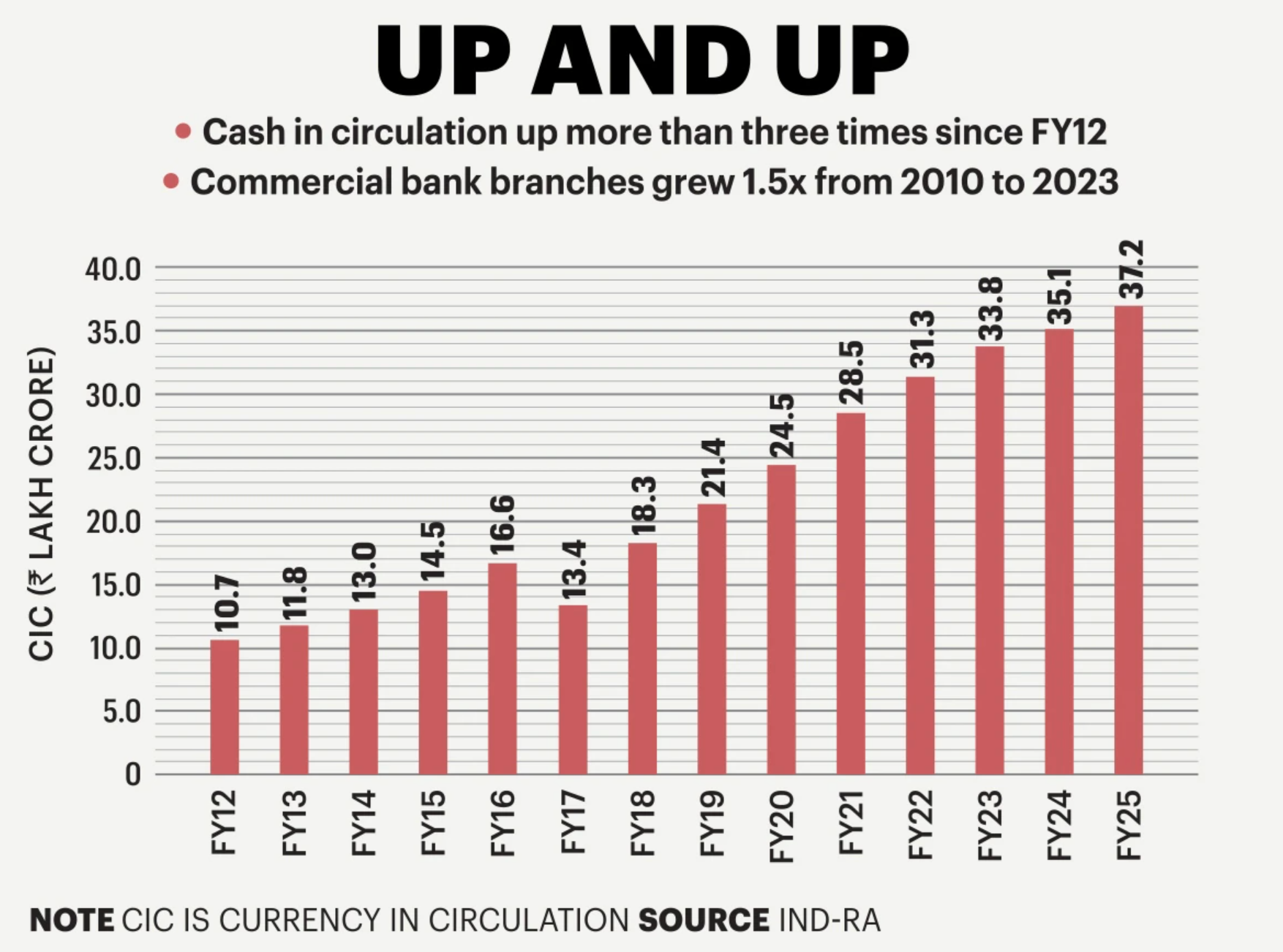

India is actually holding record amounts of cash.

According to RBI data, currency in circulation stood at roughly ₹42.5 lakh crore in May 2026. Just a year ago, it was around ₹38 lakh crore. That's an annual growth rate of nearly 12%.

In other words, there is more physical cash moving around the Indian economy than ever before.

The problem is that the cash isn't reaching ATMs efficiently.

And that leads us into a much bigger story about how India's payment ecosystem is changing.

For years, ATM economics were fairly straightforward. More people used cash, ATM transactions grew steadily, and operators could spread their costs across a large volume of withdrawals.

Today, that equation is breaking down.

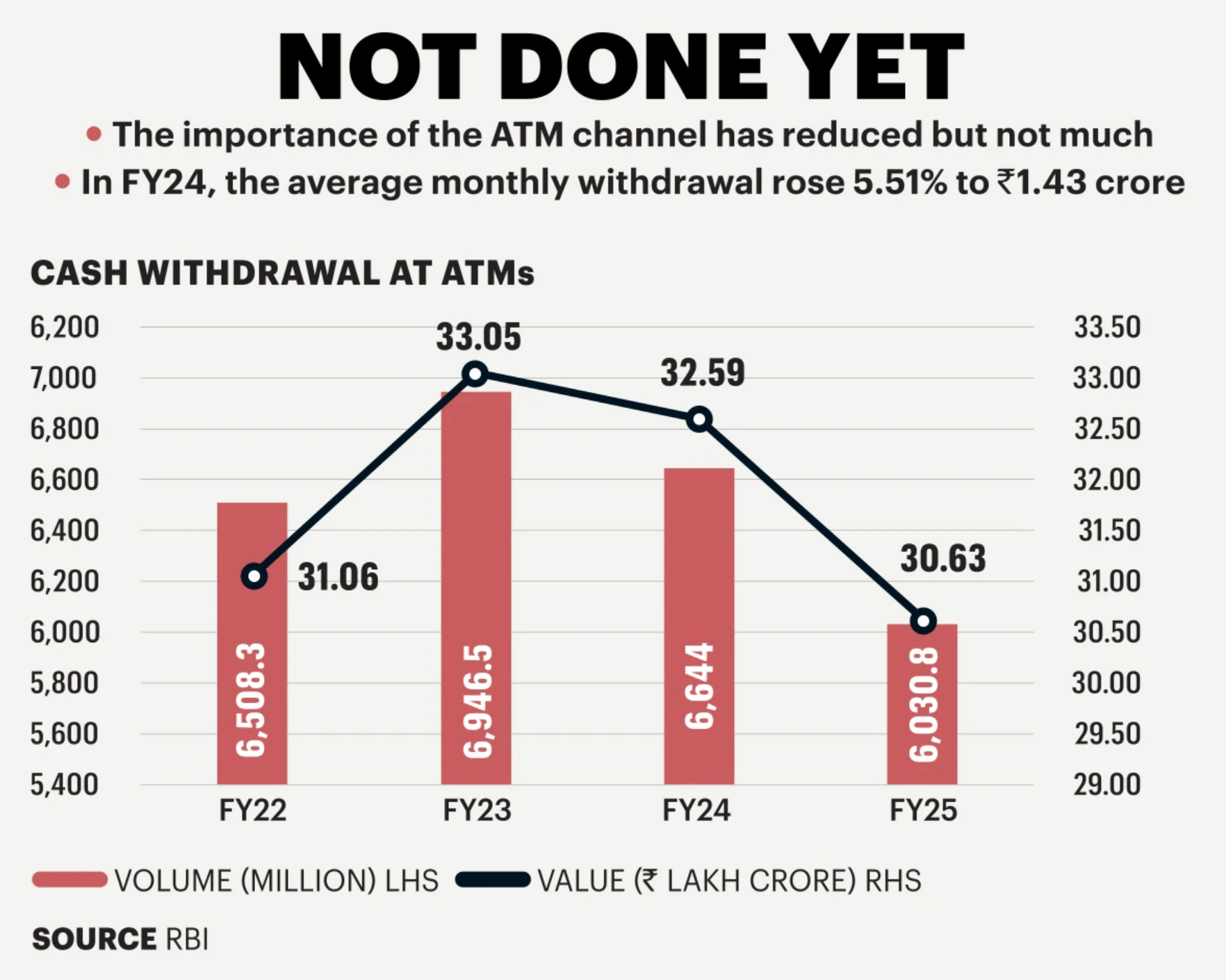

According to RBI's Monthly Bulletin, ATM transactions fell from 498.4 million transactions to 446.5 million transactions over the past year. That's a decline of more than 10%.

The industry had planned for a gradual decline of around 2.5% to 3% annually as digital payments grew. Instead, transaction volumes have fallen more than three times faster than expected.

The obvious reason is UPI.

India processed more than 18 billion UPI transactions in a single month earlier this year. From street vendors and tea stalls to supermarkets and fuel pumps, digital payments have become the default option for millions of Indians.

Every time a customer scans a QR code instead of withdrawing cash, that's one less ATM transaction.

At first glance, that sounds like good news. Less cash usage should mean less pressure on ATM infrastructure.

But something interesting has happened.

People are withdrawing cash less frequently, yet they are not abandoning cash altogether.

In fact, cash in circulation continues to rise rapidly.

This apparent contradiction has puzzled economists for years.

The answer seems to be behavioural.

Instead of visiting ATMs regularly, people are making fewer trips and withdrawing larger amounts each time. Studies from SBI and data from cash management firms suggest that Indians are increasingly holding precautionary cash balances. They may use UPI for daily payments, but they still want physical cash available for emergencies, local transactions, rural markets, informal payments, festivals and situations where digital infrastructure may not work perfectly.

As a result, cash demand remains strong even as ATM usage falls.

This creates a problem for ATM operators.

Running an ATM is expensive.

Every cash withdrawal depends on a surprisingly large physical infrastructure network. Cash must be transported in specialised vans. Security personnel have to accompany the cash. Machines require maintenance. Fuel costs must be paid. Insurance costs continue to rise. Technicians need to be deployed. ATM locations require rent and electricity.

On top of that, wage costs have increased across several states following revisions under the Code on Wages. Fuel prices have also remained elevated due to geopolitical tensions and volatility in global energy markets.

While costs have surged, revenue growth has not kept pace.

Much of the industry's income comes through interchange fees. This is the fee one bank pays another when its customer uses a different bank's ATM. The current interchange fee stands at ₹19 per transaction, up from ₹17 earlier.

Industry players argue that this increase has been nowhere near enough to offset rising operational costs.

To make matters worse, the fee customers pay after exhausting their free monthly ATM transactions was increased from ₹21 to ₹23 in 2025. While this was intended to support ATM economics, it may have had an unintended consequence. Higher withdrawal costs encouraged even more customers to shift toward digital payments.

So ATM operators ended up facing both declining transaction volumes and rising operating expenses at the same time.

That combination is rarely sustainable in any business.

There is another factor that receives far less attention.

The withdrawal of ₹2,000 notes may have increased cash handling costs.

A single ₹2,000 note stores the same value as four ₹500 notes. Once high-value notes disappeared from circulation, ATMs required larger physical volumes of cash to dispense the same amount of money. More cash movement means more loading trips, more logistics operations and higher costs throughout the system.

None of these issues individually would have caused a crisis.

Together, however, they have gradually weakened the economics of maintaining India's ATM network. In large parts of rural and semi-urban India, ATMs remain a critical piece of financial infrastructure.

Millions of people receive government benefits through Direct Benefit Transfer schemes. Pensioners often withdraw cash from ATMs. Agricultural markets continue to rely heavily on cash transactions. Small merchants and local businesses frequently prefer physical cash for settlement purposes.

For these users, an empty ATM can disrupt access to income, welfare benefits and daily economic activity.

That is why CATMi's warning has attracted attention from both the Indian Banks' Association and the Reserve Bank of India.

The country now finds itself in a strange transition phase.

And unless regulators, banks and ATM operators find a way to make that infrastructure economically viable again, India could discover that even in the age of UPI, keeping cash available is a lot more complicated than printing it.