Mango prices are acting strange again.

In some parts of India this season, consumers are paying ₹300-₹400 a kilo for premium varieties, while in other regions farmers have been forced to sell at ₹40-₹45 a kilo.

That kind of divergence is a signal of a complex mix of climate risk, local demand, export limitations and supply chain gaps.

Let’s start with the obvious.

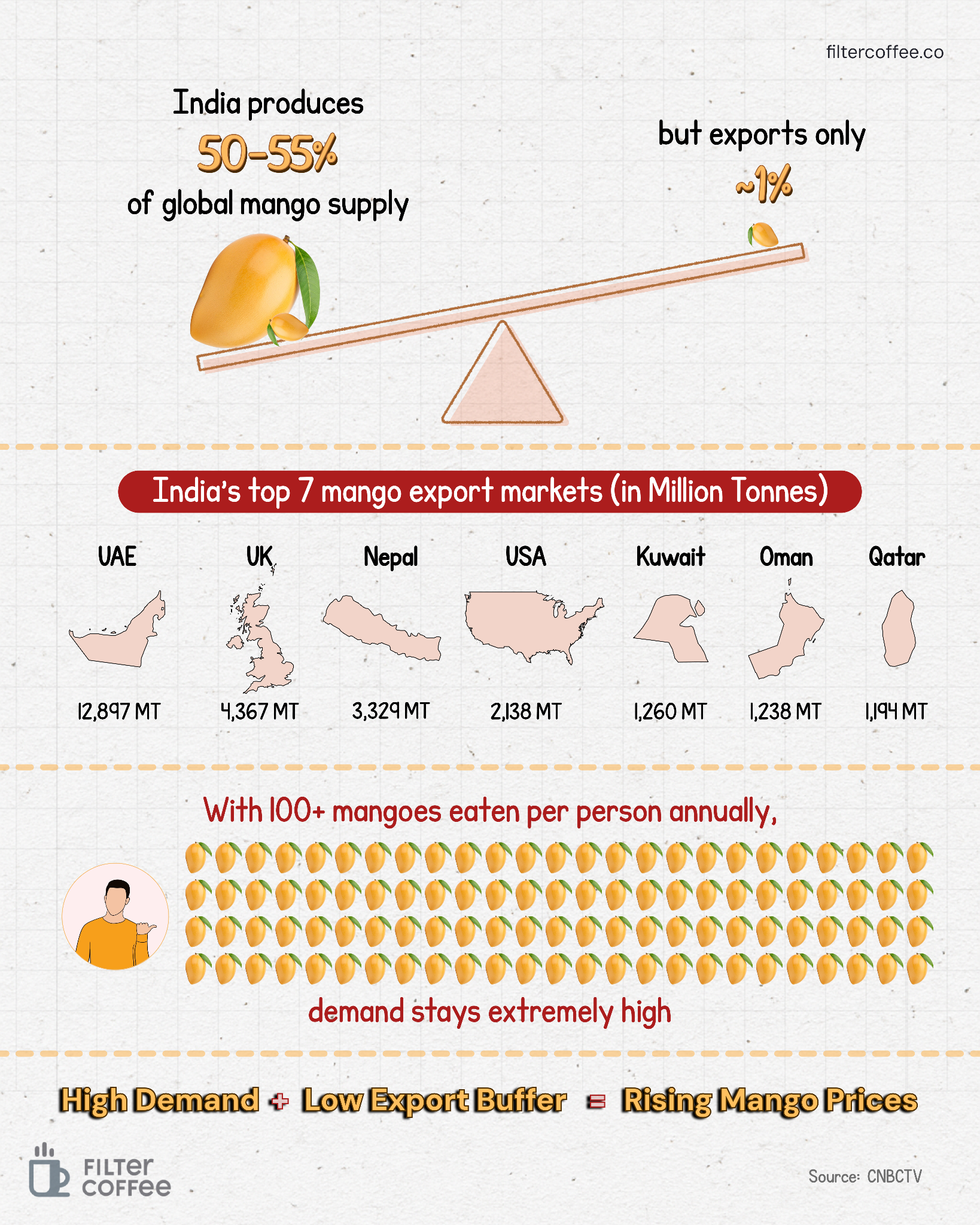

India is the undisputed king of mangoes. It produces roughly 50-55% of the world’s supply and accounts for about 42.8% of global output.

In absolute terms, India’s fruit production crossed 112 million tonnes recently, with mangoes forming a significant share. Uttar Pradesh alone contributes over 25% of India’s mango production.

But that assumption breaks down once you look at how little of this supply actually leaves the country.

India exports only about 30,000 tonnes of fresh mangoes a year which is barely a fraction of its production. Whereas Indians consume over 100 mangoes per person annually in some estimates. So almost everything grown here is eaten here.

When supply dips even slightly, prices spike quickly because there is no large export buffer that can be redirected back into the domestic market.

And then there’s climate.

Mangoes are highly sensitive to weather patterns. Unseasonal rains, heatwaves, or delayed flowering cycles can wipe out large portions of the crop.

In 2026, parts of Andhra Pradesh reported crop losses of over 60%, with yields dropping from 6-8 tonnes per hectare to as low as 2-3 tonnes. Due to this, local shortages push prices sharply upward. That is why varieties like Banganapalli and Rasalu suddenly start selling at ₹300-₹400 per kilo in affected regions.

But then you also see the opposite.

In 2025, states like Uttar Pradesh had a bumper crop. Production jumped from around 25 lakh tonnes to 35 lakh tonnes. Prices fell by as much as 30% in local markets because supply overwhelmed demand. Farmers had to sell at lower rates since there were not enough processing units or export channels to absorb the surplus.

This is the paradox of India’s mango economy.

A good harvest does not always mean higher income for farmers, and a bad harvest does not always mean uniform price increases across the country.

Exports could have acted as a stabilizer here, but they are constrained.

Mangoes are perishable, require strict quality standards, and need cold chain logistics that India still struggles with at scale. Even in premium export markets like the UAE, USA, and UK, Indian mangoes face quality checks and logistical hurdles.

There are efforts to fix this, like sea shipment protocols and export promotions, but these are still evolving.

So when supply rises, India cannot easily push large volumes abroad. And when supply falls, it cannot pull back exports to cool domestic prices because exports are already small.

There is also a geographic mismatch.

Mangoes are grown in specific clusters, but demand is spread across the country. Transporting them efficiently requires cold storage and fast logistics. Any bottleneck in this chain leads to wastage in one region and shortages in another.

That is why you can see low prices in a producing state and high prices in a consuming city at the same time.

Moreover, India has over 1,000 mango varieties, but only a handful are commercially traded. Premium varieties like Alphonso and Kesar command high prices and are export-oriented, while others are consumed locally. This segmentation creates multiple parallel markets, each with its own pricing dynamics.

So when you look at rising mango prices, it is not just inflation or demand.

It is a story of a country that produces half the world’s mangoes but consumes almost all of them, where weather shocks can wipe out supply overnight, where bumper crops can crash farmer incomes, and where export limitations prevent the system from balancing itself.

High demand plus low export flexibility plus climate volatility is what ultimately drives those dramatic price swings you see every summer.