Adani Power just reported a 64% jump in quarterly profit. But the business itself didn’t grow at the same pace. In many ways, this quarter shows how power companies manage when demand doesn’t quite show up.

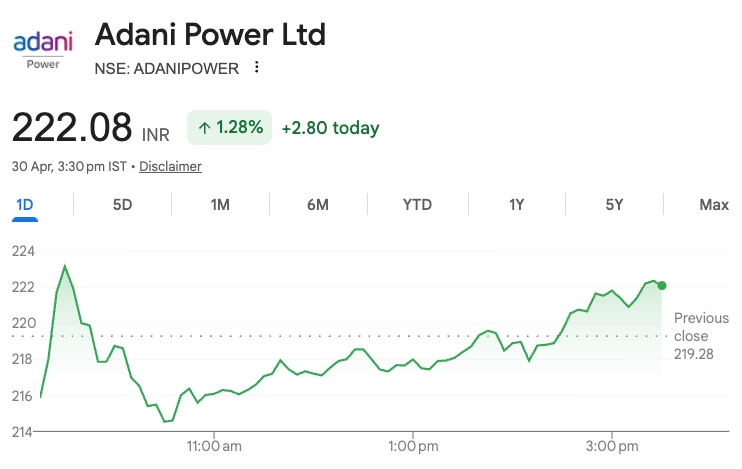

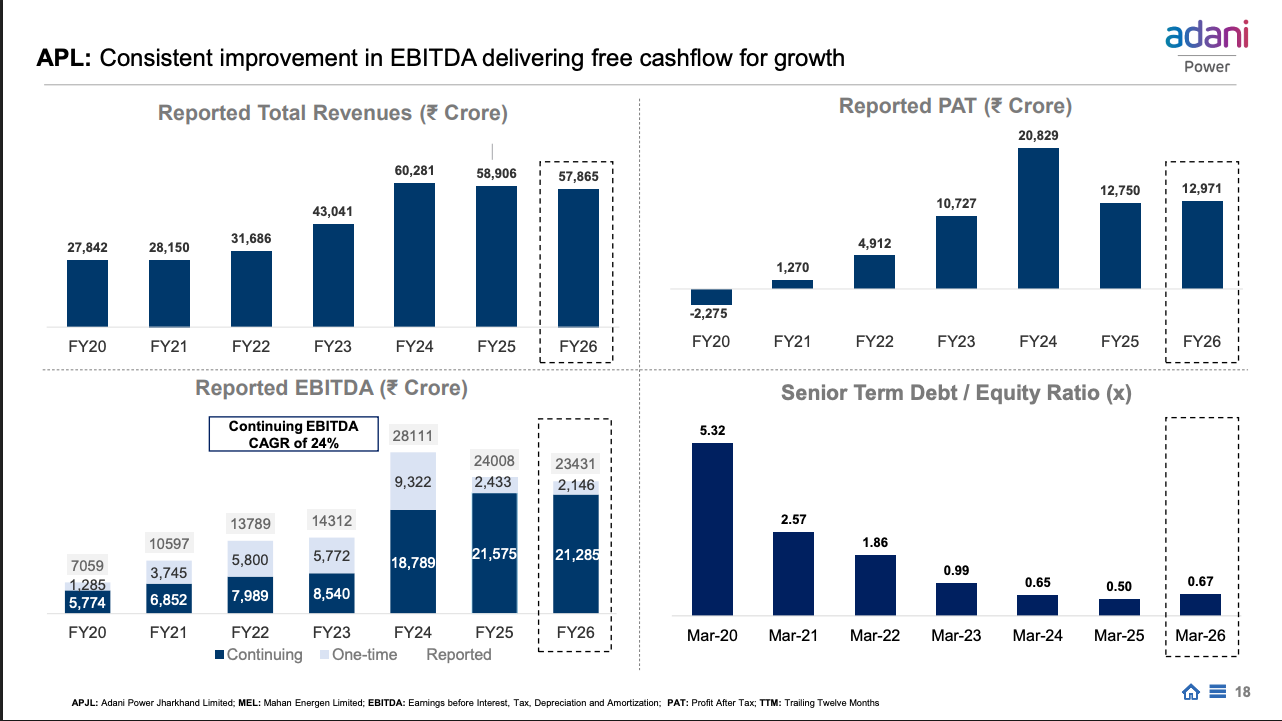

For the March quarter of FY26, Adani Power posted a profit after tax of ₹4,271 crore, up sharply from ₹2,599 crore last year. But the actual business of selling electricity didn’t really grow much.

Revenue from core operations stayed almost the same as last year, hovering around ₹14,200–₹14,500 crore. Even for the full year, revenue was slightly lower at about ₹55,500 crore, compared to around ₹56,400 crore last year.

Adani Power is India’s largest private thermal power producer. Simply put, it generates electricity mainly using coal and sells it to state utilities, industrial customers, and power distribution companies.

It operates a network of large power plants across states like Gujarat, Maharashtra, Tamil Nadu, and Chhattisgarh, with over 18 GW of installed capacity. Most of its electricity is sold through long-term contracts, which helps keep revenues stable even when market conditions fluctuate.

So how did profits jump if the core business barely moved?

Two things quietly did the heavy lifting. One, costs came down. Two, income from non-core sources went up significantly.

Fuel costs, which are a big expense for power companies, came down a bit because coal became cheaper and sourcing improved. At the same time, “other income” shot up sharply, rising nearly five times compared to last year. This included things like a government refund of around ₹539 crore, gains from foreign exchange movements, and some one-time adjustments from earlier periods. If you also add a lower tax bill, profits start looking much stronger, even though the core business hasn’t really grown much.

Because FY26 was not exactly a great year for power demand. India’s total electricity demand grew just 0.8% for the year and about 1.6% in the March quarter. That is unusually slow for a country where power consumption typically grows alongside the economy. A big reason was the weather. Extended monsoons and cooler temperatures meant lower consumption for months, especially in the early part of the year.

At the same time, power prices in the open market started falling. The average price on the Indian Energy Exchange dropped over 12% in the quarter and nearly 14% for the full year. Think of it like this. Not all electricity is sold through fixed contracts. Some of it is sold daily in the open market, where prices keep changing based on demand and supply.

So when demand is weak, prices fall. And any power that isn’t locked into long-term contracts ends up getting sold at these lower, more volatile prices.

So if demand was weak and prices were falling, why didn’t Adani Power’s numbers fall apart?

Because most of its business is no longer dependent on the open market.

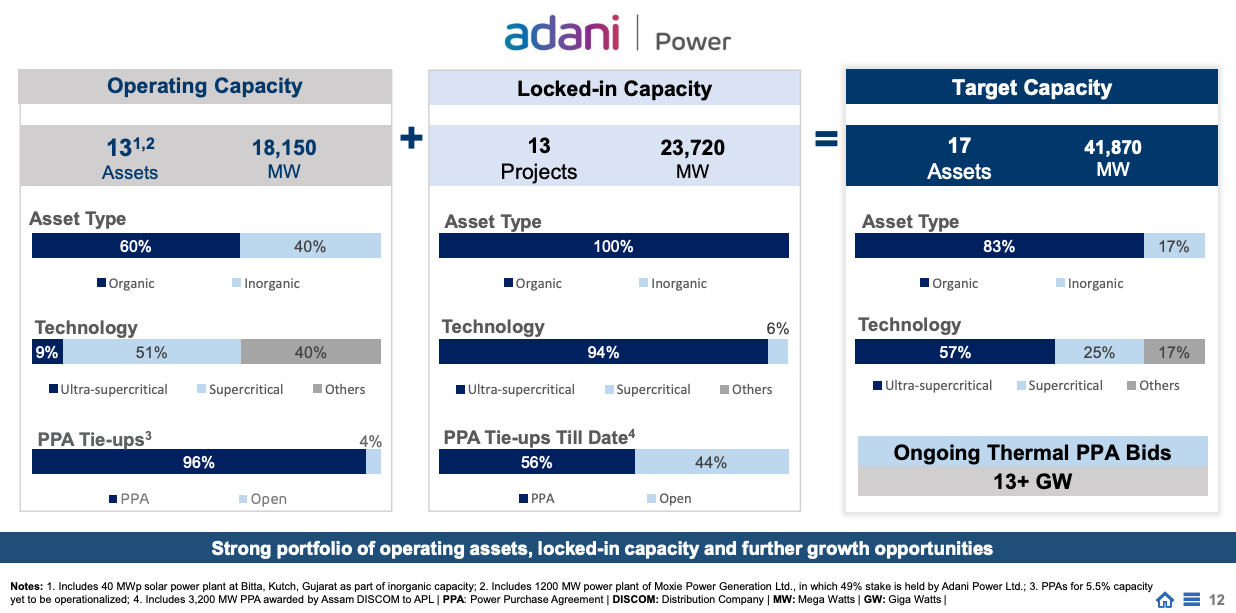

About 95% of its operating capacity is now tied up under long-term power purchase agreements, or PPAs. These contracts ensure a steady flow of revenue regardless of short-term demand fluctuations. It is like a subscription model for electricity. Even if consumption dips temporarily, the company still gets paid for making capacity available.

This shift towards contracted capacity is one of the most important things happening in Adani Power right now. Over the last year, it signed multiple deals, including a fresh 1,600 MW long-term agreement with Maharashtra and a 558 MW deal through its subsidiary with Tamil Nadu. In total, it has tied up over 13 GW of additional capacity under contracts.

This is also why volumes are still growing. Power sales increased to about 99 billion units for the year, up around 3.4%. Generation crossed 105 billion units. So operationally, the company is expanding. It is just doing so in a market where pricing is under pressure.

But there is another side to this story that is easy to miss.

Growth is getting more capital intensive.

Adani Power is in the middle of a massive expansion cycle. It plans to add around 23.7 GW of capacity by 2032, which is a huge number even by industry standards. Projects like Mahan, Raipur, and Raigarh are already under construction, with some nearing completion.

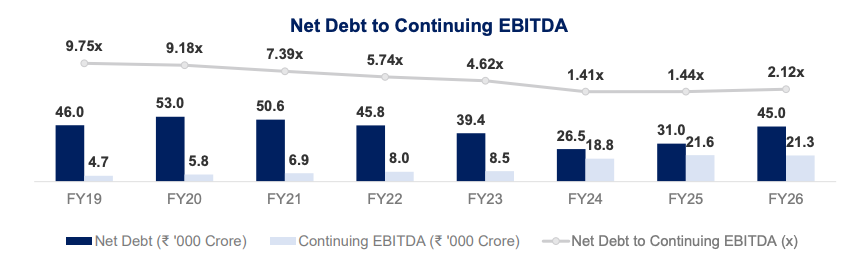

To fund all of this, debt is going up again. Net debt has risen to about ₹45,000 crore, compared to roughly ₹31,000 crore a year ago. The company also raised ₹7,500 crore through non-convertible debentures recently. While management insists that most expansion will be funded through internal accruals, the balance sheet is clearly getting heavier.

This is where the future gets interesting.

Because the long-term demand story for power in India is still very strong. Estimates suggest that electricity demand could multiply nearly four times over the next two decades. Peak demand is expected to keep rising as manufacturing, electric mobility, and digital infrastructure scale up.

And despite all the buzz around renewables, thermal power is still expected to play a crucial role. Not because it is clean, but because it is reliable. Solar and wind are intermittent. Coal plants provide the steady base load that keeps the grid stable, especially during peak demand hours.

That is exactly the bet Adani Power is making.

It is positioning itself as a large-scale, contract-backed, base load power supplier in a country that will need a lot more electricity. Its strategy is simple. Lock in long-term contracts, expand capacity aggressively, and ride the structural demand growth.

But execution will matter a lot from here.

Because the environment is getting more complex. Renewable energy is increasing its share in the grid, which can suppress spot prices further. Demand growth can remain uneven due to weather patterns. And higher debt means less room for error if cash flows become volatile.

So the real takeaway from this quarter is not just that profits went up.

It is that Adani Power is transitioning into a more stable but also more capital-heavy business model. One where short-term volatility is managed through contracts, but long-term success depends on how well it balances expansion, pricing, and financial discipline.

In a way, this is what the next phase of India’s power story might look like. Less about sudden spikes in growth, and more about who can build scale, lock in demand, and still keep the numbers under control.