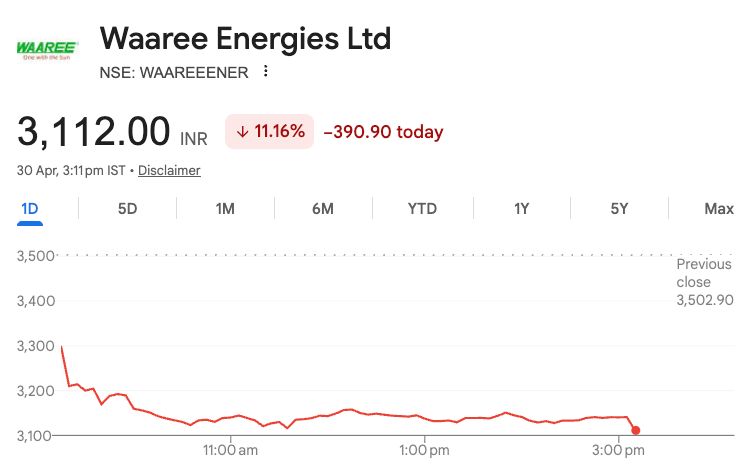

Waaree Energies just reported one of its strongest years ever. And yet, the stock crashed over 10% in a single day.

This makes no sense… right?

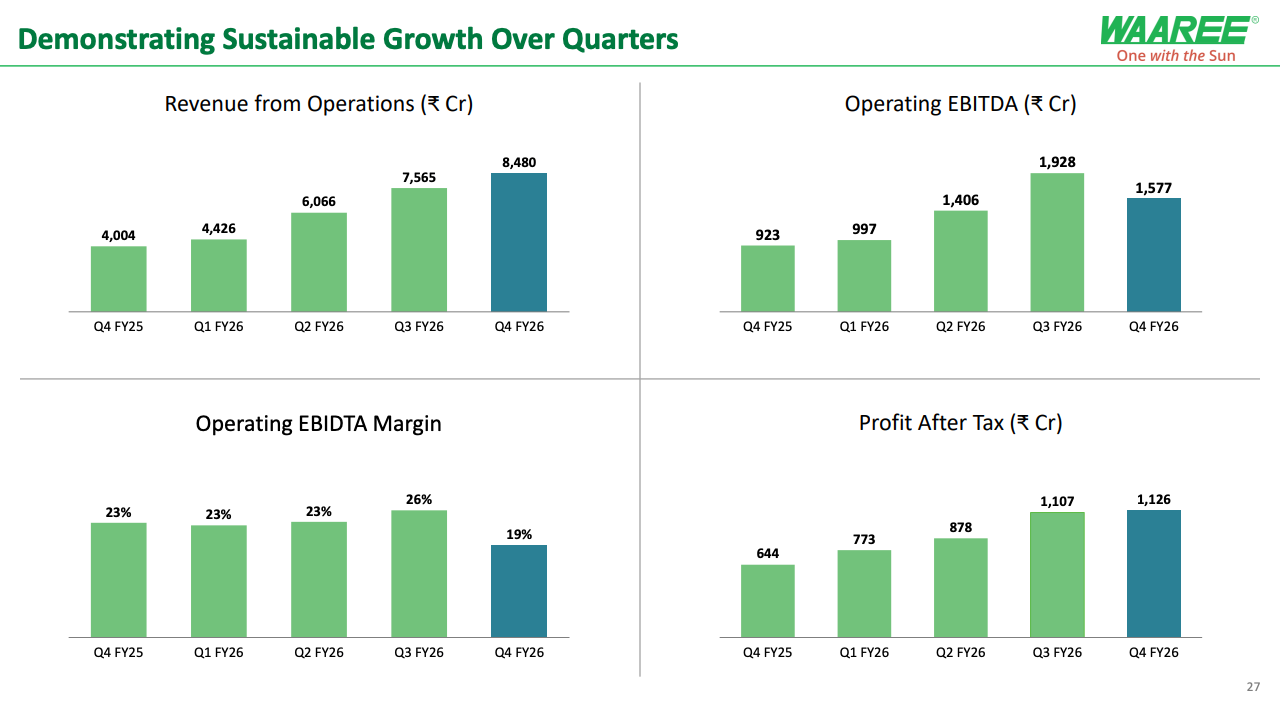

The company’s Q4 FY26 numbers were solid. Revenue for the quarter jumped over 110% year-on-year to roughly ₹8,800 crore. Net profit rose nearly 75% to about ₹1,126 crore.

For the full year, revenue crossed ₹26,500 crore, while total EBITDA came in at around ₹6,600 crore, comfortably above the company’s own guidance. Production also scaled up sharply, with annual module output hitting 12.6 GW, almost double last year.

So why did investors panic?

Because the one number that really mattered went the other way. EBITDA margins dropped to around 18.6%, down from roughly 23% a year ago, and more importantly, below what analysts were expecting.

In simple terms, this means that for every ₹100 Waaree earned, it is now keeping only about ₹18 as operating profit instead of ₹23 earlier.

So even though the company is selling a lot more, it is making less profit on each sale. In fact, most brokerages had pencilled in margins closer to 21–25%. That gap is what spooked the market.

But why did margins slip despite strong growth? Let’s understand!

Waaree is no longer just a solar module manufacturer. It is trying to become a fully integrated energy company. And that shift is expensive.

Over the last year, the company has been aggressively moving upstream and downstream across the solar value chain. It has taken a strategic stake in an Oman-based polysilicon company to secure raw materials.

It has started building a 10 GW ingot and wafer facility in Nagpur. It has approved nearly ₹3,900 crore to set up a solar glass manufacturing plant, a critical component that accounts for roughly a quarter of module costs.

On top of that, it is expanding into batteries, inverters, transformers, and even green hydrogen. Add it all up, and Waaree is sitting on a massive capex pipeline that runs into tens of thousands of crores.

This is where the trade-off kicks in. When companies scale this aggressively, costs tend to rise faster than revenues in the short term. New plants take time to stabilize.

Technology transitions, like the shift to newer G12 and G12R solar cells, can initially push up costs. Input prices, especially for cells and other components, can fluctuate. All of this eats into margins before the benefits of scale and integration start kicking in.

G12 and G12R are newer, larger-format solar cells that generate more power per panel and improve efficiency.

You can actually see this playing out in the financials. While revenue more than doubled in Q4, operating EBITDA did not grow at the same pace. And sequentially, EBITDA even declined compared to the previous quarter, signalling that cost pressures are real and not just a one-off.

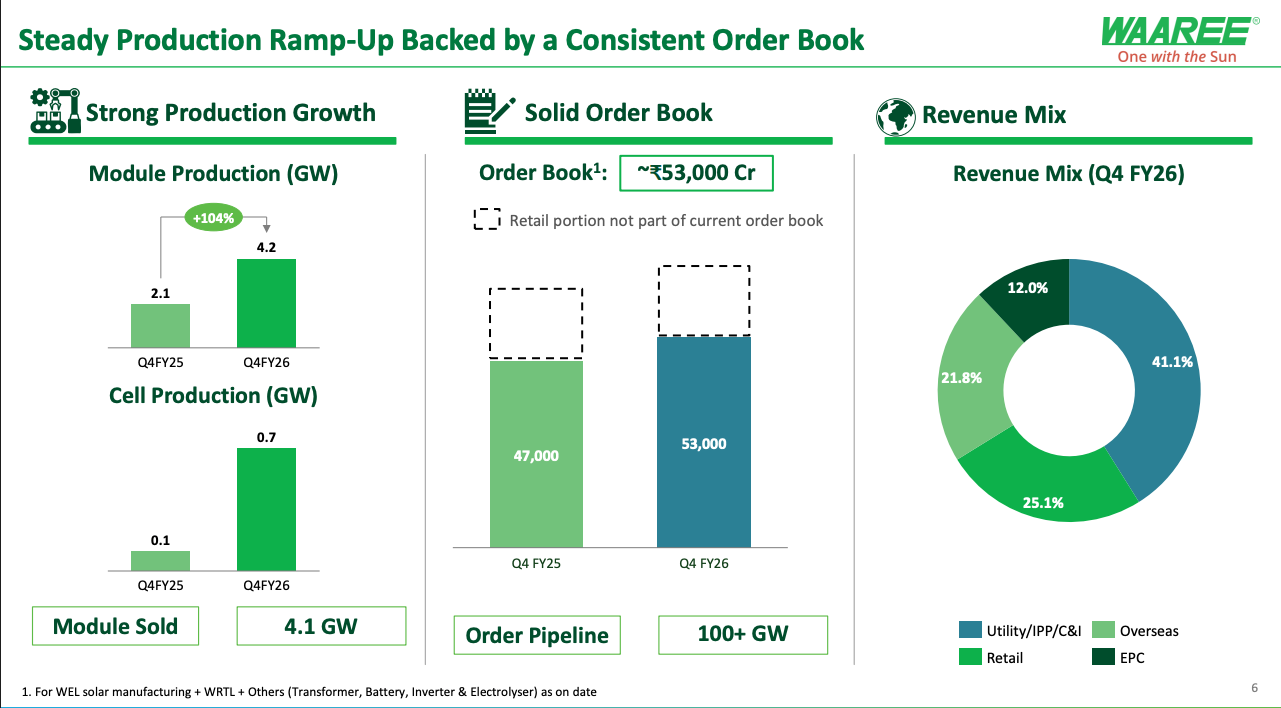

At the same time, expectations were already very high. Waaree has positioned itself as one of the largest non-Chinese solar module manufacturers globally, with around 26 GW of module capacity and a strong order book of roughly ₹53,000 crore.

It also claims a pipeline of over 100 GW, which gives it significant revenue visibility. In a market where global buyers are increasingly looking for alternatives to China, Indian players like Waaree are in a sweet spot.

But that also means the market is not just looking for growth. It is looking for consistent, high-quality growth with stable margins. When margins fall short, even strong revenue and profit numbers are not enough to keep investors happy.

There is also a broader industry context at play.

Solar demand globally is booming, with total installed capacity expected to grow multiple times over the next decade. India itself added over 44 GW of solar capacity in FY26, taking the cumulative total past 150 GW. Government policies like the PLI scheme, anti-dumping duties on imports, and the push for domestic manufacturing are all tailwinds for companies like Waaree.

But the industry is also highly competitive. Pricing pressure remains intense, especially with Chinese manufacturers still dominating global supply. Raw material costs can be volatile. And as companies expand into adjacent areas like storage, hydrogen, and grid infrastructure, the execution complexity increases significantly.

Waaree is trying to solve this by building a fully integrated model. The idea is simple in theory. If you control everything from polysilicon to modules to storage and even power infrastructure, you reduce dependency on external suppliers, improve cost control, and capture more value across the chain. Over time, this can lead to better margins and a stronger competitive position.

But in the short term, it looks messy. Capital is tied up in new projects. Costs rise before revenues from these segments fully kick in. And margins tend to normalise or even dip.

That is exactly what the market is reacting to right now.

Interestingly, the company itself remains optimistic. It has guided for FY27 EBITDA in the range of ₹7,000 to ₹7,700 crore, implying continued growth. The order book is strong, capacity expansions are on track, and new verticals are expected to start contributing over the next few years.

So the real story here is not about a bad quarter. It is about a company in transition.

Waaree is moving from being a fast-growing solar manufacturer to a large, integrated energy player. The opportunity is massive, especially in a world that is rapidly shifting towards clean energy. But the journey comes with costs, both financial and operational.

For investors, the question is fairly straightforward now. Not whether Waaree can grow, because it clearly can, but whether it can manage this expansion while protecting margins.

Because in markets, growth gets attention. But profitability earns trust.