The government just made a quiet move that says a lot without changing anything.

For the April to June 2026 quarter, interest rates on post office small savings schemes have been left unchanged, marking eight straight quarters without any revision.

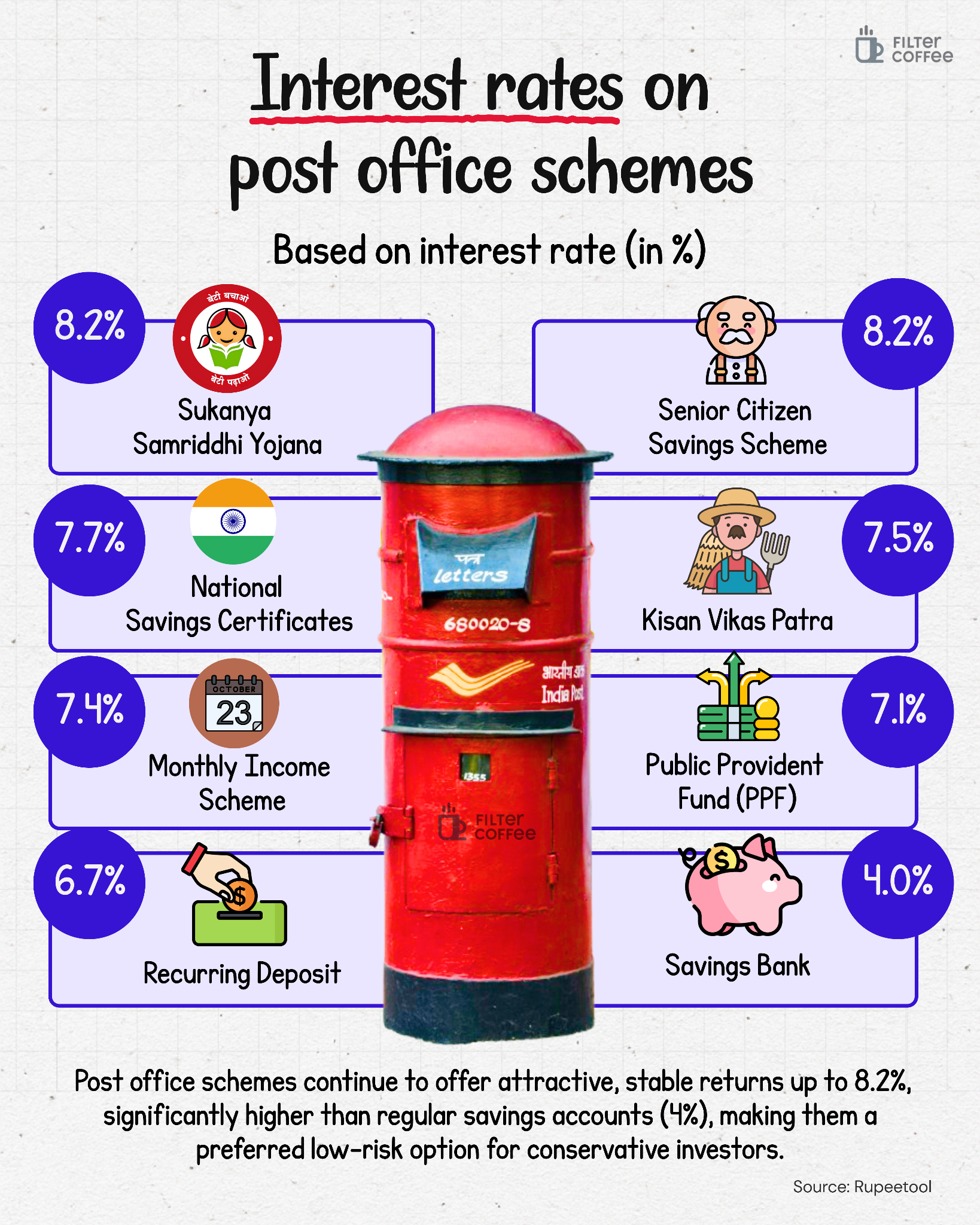

Sukanya Samriddhi Yojana and the Senior Citizen Savings Scheme continue to offer 8.2%, National Savings Certificates sit at 7.7%, Kisan Vikas Patra at 7.5%, Monthly Income Scheme at 7.4%, and the long-trusted Public Provident Fund remains at 7.1%.

On the surface, nothing has changed. But that stability is the story.

To see why this matters, you need to look at the bigger picture since these schemes aren’t priced randomly.

India uses a formula that links their rates to government bond yields with a small spread. In simple terms, if government borrowing costs rise, these rates should rise too, and vice versa.

But since early 2024, even as bond yields and inflation have moved around, the government has chosen not to tinker with these rates. It is a signal that stability is being prioritised over frequent adjustments.

There is also a balancing act here.

Small savings schemes compete directly with bank deposits. If post office rates are too high, banks struggle to attract deposits, which in turn affects lending and the broader economy.

If they are too low, households shift away from these safe instruments. Right now, a typical savings account gives about 4%, while fixed deposits from banks hover around 6.5 to 7.5% depending on tenure.

With that in mind, a government-backed 8.2% for senior citizens looks very attractive. It explains why schemes like SCSS have seen strong inflows in the last two years, especially from retirees looking for predictable income.

Then there is the trust factor.

Nearly 1.5 lakh post offices across India form the backbone of this system, many in rural and semi-urban areas where access to formal banking is still evolving.

For millions of households, these schemes are not just investments, they are default savings tools.

The Public Provident Fund alone has a 15-year lock-in and tax-free returns, making it a long-term wealth builder. Kisan Vikas Patra doubles money in about 115 months, which is roughly 9 years and 7 months.

Recent developments show the system is slowly modernising.

Aadhaar-based biometric e-KYC has been expanded to schemes like PPF and recurring deposits, allowing people to open accounts and transact without paperwork.

At the same time, the government has begun tightening processes by freezing accounts that remain inactive for more than three years after maturity, nudging investors to either extend or close them. It is a mix of convenience and discipline.

The interesting part is how all of this ties into the broader economy.

When inflation stays within the Reserve Bank of India’s comfort zone and interest rates are not rising sharply, there is less pressure to increase small savings rates.

At the same time, the government itself borrows heavily, and higher rates on these schemes would mean a higher cost of borrowing. Keeping rates steady helps manage that burden.

So while the headline says no change, the subtext is richer.

Post office schemes today sit at the intersection of financial inclusion, government borrowing, and household savings behaviour.

They offer returns that beat basic bank accounts, carry sovereign backing, and are becoming more accessible through digitisation.

While everyone else is chasing quick returns and high gains, they keep doing their own thing in a slow, steady, and still very relevant way.