Every time we tap “order now”, we are making an assumption. That someone, somewhere, will figure out how to get that product to us quickly, cheaply, and without drama. We don’t think about traffic, rider availability, wrong addresses, sudden rain, or the fact that half the country seems to order food and groceries at the same time on Friday nights. We just expect it to work.

India’s digital economy runs on that expectation.

And behind it sits a layer of companies most people never notice. Third-party logistics firms that quietly connect apps to doorsteps. They don’t sell products. They don’t own customers. But without them, the entire promise of e-commerce and quick commerce collapses.

Shadowfax is one of those companies.

Founded in 2015, Shadowfax started with a simple idea: build a technology-led logistics platform that could help businesses deliver faster without owning heavy assets. Instead of warehouses and trucks, it focused on software, data, and a flexible delivery network. Over time, it became deeply embedded in how India moves parcels, food, groceries, and even returns.

Today, Shadowfax operates across nearly 15,000 pin codes. That number matters because it shows how far digital consumption has spread beyond metros. Delivering in India is not just about highways and pin drops. It is about navigating narrow lanes, inconsistent infrastructure, and wildly different demand patterns across cities and towns. Scaling logistics here is less about glamour and more about operational muscle.

The timing of Shadowfax’s IPO reflects a bigger shift in India’s economy.

Digital commerce is no longer a niche or urban phenomenon. E-commerce platforms are expanding deeper into Tier 2 and Tier 3 cities. Quick commerce has trained consumers to expect speed as a default, not a luxury. Food delivery, hyperlocal services, and on-demand mobility have become habits, not experiments.

At the same time, enterprises are rethinking logistics. Building delivery capabilities in-house is expensive and inflexible. Outsourcing to tech-driven partners allows them to scale up during peak seasons and scale down when demand softens. This is where third-party logistics providers like Shadowfax fit in.

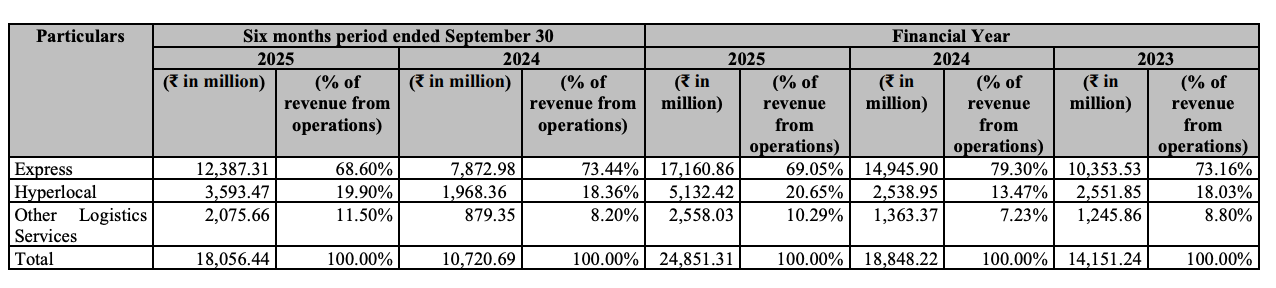

Shadowfax positions itself as a full-stack, last-mile logistics platform. It handles forward deliveries, reverse logistics for returns, hyperlocal deliveries, quick commerce, and mobility-linked logistics. Its value proposition is not just reach, but speed, flexibility, and reliability powered by technology.

But logistics is not a feel-good business. It is a pressure cooker.

Margins are thin. Client expectations are high. Delivery partners come and go. Fuel costs fluctuate. Regulations around gig workers evolve. One festive season can make or break operational metrics. And pricing power is limited because clients can switch providers if service levels drop.

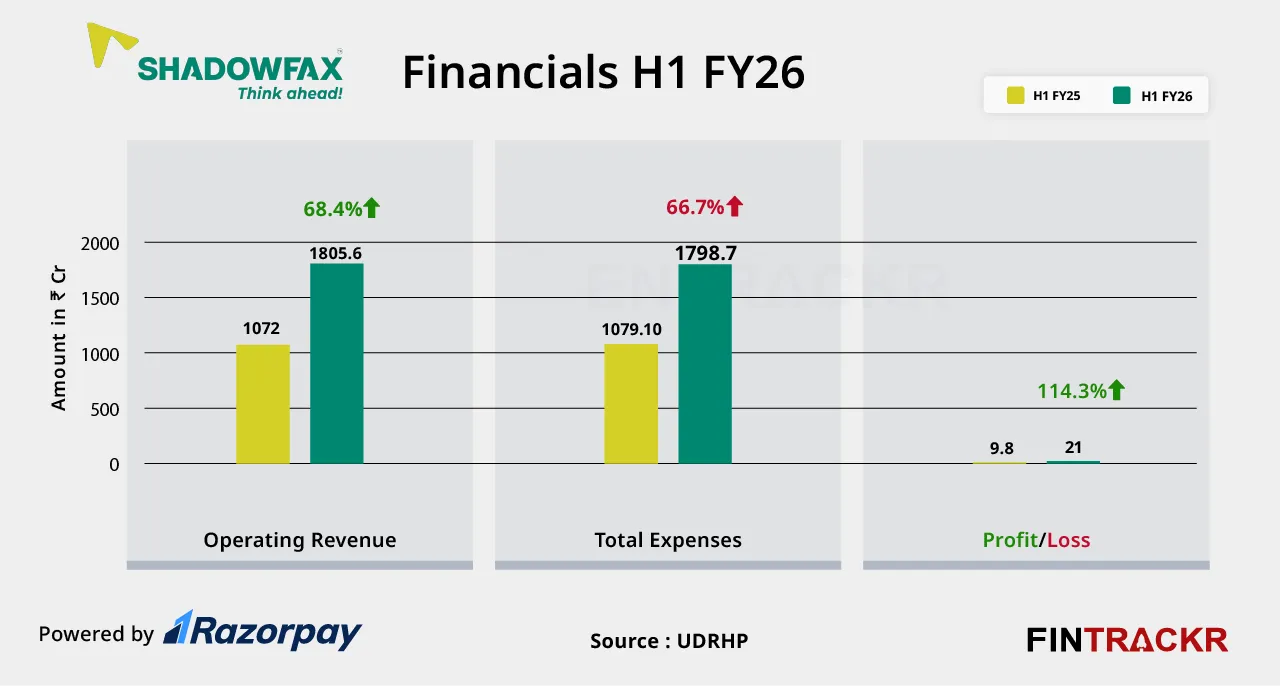

Shadowfax’s financials reflect this reality clearly.

The company has reported losses in recent years, largely due to high operating costs and continuous investments in expansion and technology. But the trend within those numbers is important.

*Figures are in ₹ million.

Here, you’ll see that the losses stand out. But look closer.

Revenue has grown strongly over this period, reflecting higher volumes and wider client adoption. More importantly, losses have narrowed sharply. The jump from a loss of over ₹1,400 million in FY23 to roughly ₹119 million in FY24 suggests tighter cost control and improving unit economics.

This pattern is common in logistics. At smaller scales, inefficiencies dominate. Riders are underutilised, routes are fragmented, and fixed costs weigh heavily. As scale increases, delivery density improves. More orders per rider, shorter routes, better batching, and smarter allocation through software. That is when operating leverage starts showing up.

Shadowfax is betting that it is approaching this phase.

The IPO is designed to support that transition. It includes a fresh issue of shares to raise capital for the business and an offer for sale by existing investors. The fresh capital is expected to strengthen the balance sheet and fund growth initiatives. The offer for sale allows early backers to partially monetise their investments after years of funding the company’s expansion.

This structure matters. Shadowfax is not coming to the market as a distressed company looking for rescue capital. It is coming as a scaling business trying to move from startup economics to institutional discipline.

Still, investors should be clear-eyed about the risks.

Profitability is not guaranteed in the near term. Shadowfax itself acknowledges that losses could continue as it invests in growth. Competition in third-party logistics is intense, with multiple startups, established players, and even large e-commerce firms building hybrid delivery models.

The gig workforce model, while flexible, comes with challenges. High attrition, training costs, and evolving labour regulations can disrupt operations and push up costs. Hyperlocal and quick commerce deliveries are particularly demanding, with tight service-level agreements and low tolerance for delays.

There is also dependency on the broader digital economy. Any slowdown in e-commerce growth or recalibration in quick commerce economics would directly affect logistics volumes.

So what does this IPO represent in the bigger picture?

Shadowfax is not pitching a futuristic vision or a breakthrough technology. It is pitching relevance. The relevance of being embedded in how India consumes, orders, and receives goods every day. Its business grows when digital habits deepen and when enterprises choose flexibility over ownership.

For investors, this is not a short-term thrill play. It is a long-term bet on scale, execution, and operational discipline. The upside lies in operating leverage and consolidation. The downside lies in execution missteps, competitive pressure, and slower-than-expected margin improvement.

The biggest question you should ask yourself is simple. Do you believe scale will eventually tame the chaos?

If yes, this IPO is worth studying closely.If not, it simply highlights that convenience-led businesses take time to translate scale into steady shareholder returns.

Either way, the next time your order arrives faster than expected, you will know that behind that small moment of convenience is a complex business trying to turn everyday logistics into long-term value.

FAQs

What does Shadowfax do?

Shadowfax is a third-party logistics company that helps businesses deliver parcels, groceries, food, and other items to customers. It focuses on last-mile delivery using a technology-driven platform that connects enterprises with a flexible delivery partner network across India.

Why is Shadowfax launching an IPO now?

Shadowfax is launching its IPO as India’s digital commerce ecosystem continues to expand rapidly. The company is looking to raise capital to strengthen its balance sheet, support growth, and move toward more efficient, scale-driven operations as delivery volumes increase.

Is Shadowfax a profitable company?

As of the latest reported periods, Shadowfax is not yet profitable. However, its losses have reduced significantly over recent years, while revenues have grown. This suggests improving operational efficiency, though profitability will depend on future execution and scale benefits.

How does Shadowfax make money?

Shadowfax earns revenue by providing logistics and delivery services to businesses such as e-commerce platforms, quick commerce companies, and food delivery apps. It charges clients for services like forward delivery, reverse logistics, and hyperlocal fulfilment.

What are the biggest risks in Shadowfax’s business model?

Key risks include intense competition in the logistics sector, thin margins, high dependence on gig workers, regulatory changes related to labour laws, and sensitivity to slowdowns in e-commerce or quick commerce demand.

How is Shadowfax different from traditional logistics companies?

Unlike traditional logistics firms that own fleets and warehouses, Shadowfax operates a platform-based, asset-light model. It uses technology to optimise delivery routes, manage capacity, and scale operations quickly without heavy physical infrastructure.

What will Shadowfax use the IPO proceeds for?

The fresh issue proceeds from the IPO are expected to be used to support business growth, strengthen the company’s financial position, and fund ongoing investments in technology and operational expansion.

Who are Shadowfax’s key customers?

Shadowfax works with a wide range of enterprise clients, including e-commerce platforms, quick commerce players, food marketplaces, and on-demand service providers that require fast and reliable last-mile delivery solutions.

Is Shadowfax dependent on India’s e-commerce growth?

Yes. Shadowfax’s business is closely linked to the growth of e-commerce, quick commerce, and digital consumption in India. Any slowdown in these sectors could directly impact delivery volumes and revenue growth.

Is Shadowfax’s IPO suitable for long-term investors?

Shadowfax’s IPO may appeal to long-term investors who believe in India’s expanding digital economy and the potential for logistics platforms to benefit from scale over time. However, it carries execution and profitability risks that investors should consider carefully.