On March 17, 2026, the National Company Law Tribunal approved Adani Group’s ₹14,535 crore bid to take over Jaiprakash Associates, one of India’s most indebted infrastructure groups. At one level, it looked like a routine insolvency resolution finally reaching closure. At another, it left the market scratching its head. Because there was another bidder, Vedanta, that had offered nearly ₹17,000 crore. More money on the table. Yet, it still lost.

If you’re wondering how a lower bid wins in one of India’s largest bankruptcy cases, the answer lies in how these deals are actually structured, who controls the decision making, and what lenders really care about when things go wrong.

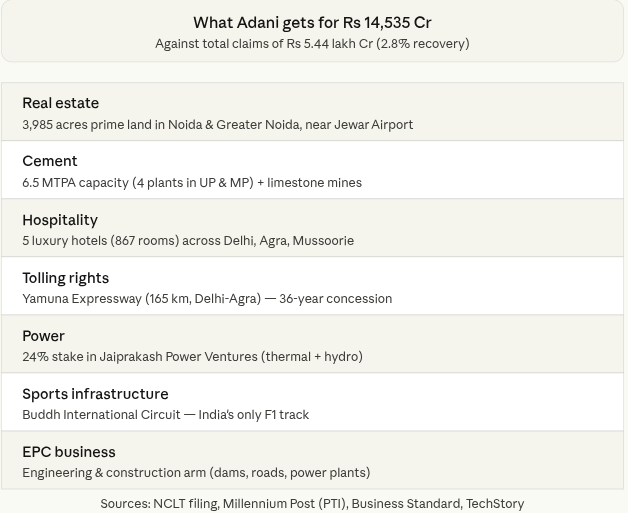

Let’s start with the basics. Jaiprakash Associates, or JAL, was once a sprawling infrastructure giant with interests across real estate, cement, power, hospitality, and highways. But years of aggressive expansion, mounting debt, and stalled projects pushed it into insolvency. By mid 2025, the company had defaulted on loans worth over ₹57,000 crore. The total admitted claims in the case were even larger, at around ₹5.44 lakh crore. This made it one of the biggest stress cases under India’s Insolvency and Bankruptcy Code.

When a company like this collapses, the goal of the system is not to save shareholders or preserve valuations. It is to recover as much money as possible for lenders. So the company is put up for auction. Bidders come in. Creditors vote. And whoever offers the best recovery plan wins.

In this case, five bidders initially showed interest. Adani Enterprises, Vedanta, Dalmia Cement, Jindal Power, and PNC Infratech. But by the final round, it was a two horse race between Adani and Vedanta.

Vedanta’s offer looked stronger. It was around ₹16,700 crore, compared to Adani’s ₹14,535 crore. But this is where things get interesting. Because the total bid amount is only part of the story. The structure of the payment matters just as much, if not more.

Vedanta’s plan involved paying roughly ₹3,800 crore upfront and the remaining amount over a period of five years. Adani, on the other hand, offered about ₹6,000 crore upfront and committed to completing most of the payment within two years.

Now put yourself in the shoes of a lender. You have already lent tens of thousands of crores to a company that has defaulted. Your capital is stuck. Your balance sheet is under pressure. Do you wait five more years to recover a higher amount, or do you take more cash today and close the chapter faster?

This is where the concept of time value of money becomes crucial. Money received today is more valuable than money received years later. When both bids are adjusted for this, the difference between them narrows significantly. In fact, estimates suggest that in present value terms, Vedanta’s bid was only about ₹500 crore higher than Adani’s.

In a deal of this scale, that difference is not large enough to outweigh the certainty of faster cash flows.

But even that does not fully explain the outcome. Because this was not a level playing field where all creditors had equal voting power.

To understand what really happened, you have to look at who was sitting at the decision making table.

Enter NARCL, the National Asset Reconstruction Company.

Set up in 2021, NARCL is often described as India’s “bad bank”. Its job is to buy stressed loans from banks and help clean up their balance sheets. Instead of banks holding onto bad loans for years, they can sell them to NARCL and move on.

In the Jaypee case, NARCL had acquired a large chunk of these bad loans from a consortium of lenders led by State Bank of India. And when it bought those loans, it also acquired the voting rights attached to them.

This changed everything.

Because voting power in insolvency cases is proportional to the amount of debt held. In simple terms, the more money a lender has at stake, the more say they have in the final decision. A bank that has lent ₹10,000 crore will carry far more voting weight than one that has lent ₹500 crore.

By buying these loans, NARCL ended up controlling around 86% of the voting power in the Committee of Creditors. Meanwhile, original lenders like SBI and ICICI Bank were left with a fraction of that influence. So when the final vote took place, it was not a fragmented group of banks debating and negotiating. It was largely one dominant entity with the power to decide the outcome.

This is important because it shifts how we interpret the result. It was not just about which bid was higher. It was about which bid aligned with the priorities of the entity holding most of the voting rights.

And those priorities were clear. Faster recovery, higher upfront payment, and greater certainty of execution.

Moreover, there is one more thing. These bids are not judged purely on price. There is a qualitative evaluation as well. Factors like the bidder’s track record, financial strength, sector expertise, and ability to execute the turnaround are all taken into account.

In this case, Adani had a strong strategic fit with Jaypee’s assets. The group already has a large presence in cement through Ambuja and ACC. It has infrastructure capabilities, power assets, and access to capital. Jaypee’s cement plants, land parcels, and infrastructure projects can be integrated into this ecosystem relatively easily.

Vedanta, on the other hand, operates primarily in metals, mining, and oil and gas. It does not have a major presence in cement or real estate. So while it may have offered a higher price, the perceived execution risk could have been higher.

According to Reuters and other business publications, citing sources involved in the process, Adani scored higher than Vedanta on qualitative parameters such as execution capability and strategic fit.

So yes, there is a perfectly rational explanation for why Adani won. Higher upfront cash, faster timeline, better strategic fit, and stronger control over the decision making process.

But even if you accept all of this, there is a bigger, more uncomfortable reality sitting underneath.

The recovery itself is still extremely low.

Against total claims of ₹5.44 lakh crore, the winning bid of around ₹15,000 crore translates into a recovery of just about 2.8%. Even if you look only at the ₹57,000 crore of bank loans, recovery is roughly 25%. Which means lenders are taking massive haircuts. Years of capital are being written off. And this is not an isolated case. It is a pattern across many large insolvency resolutions in India.

Then come the equity investors.

Under the approved plan, all existing shares of Jaiprakash Associates will be cancelled. There will be no payout. The stock will be delisted. Around ₹400 crore of market value held by over 6 lakh shareholders will simply be wiped out.

This often surprises retail investors. But it is how the system is designed. In the repayment hierarchy, equity holders come last. After secured lenders, unsecured creditors, and other claims are settled, whatever remains goes to shareholders. In most bankruptcies, there is nothing left by that stage.

And then there is a group that does not neatly fit into financial models or recovery calculations: Homebuyers.

For over a decade, thousands of families invested their savings into Jaypee’s housing projects in Noida and Greater Noida. Many paid anywhere between ₹40 lakh and ₹1 crore. These projects were supposed to be delivered years ago. Instead, they got stuck as the company’s finances deteriorated.

Even today, many of these buyers are still waiting. And the current resolution does not automatically solve their problem, because several of these projects fall under different entities within the group.

So while the focus is on a ₹14,535 crore deal, the human story remains unresolved.

The closing: This entire episode reveals how India’s insolvency system actually works in practice.

It is not an auction in the purest sense where the highest bidder always wins. It is a negotiated process where speed, certainty, and execution matter as much as price. It is also a system where control over voting power can shape outcomes decisively.

And most importantly, it is a system where value is often destroyed long before the resolution happens. By the time a company reaches this stage, the question is not how to maximise value, but how to minimise losses.

So was it fair that Adani won despite a lower bid?

If you look purely at numbers, it feels counterintuitive.

But if you look at the structure of the deal, the time value of money, the strategic fit, and the concentration of voting power, the decision starts to make sense.

At the same time, the bigger takeaway is not about who won. It is about what happens when large companies collapse under debt. Value erodes quickly. Control shifts to creditors. Decisions get centralised. And by the end of it, everyone is trying to recover whatever they can, rather than what they originally hoped for.