Airtel is preparing to take one of its most interesting businesses public, but not in India. Instead, it is looking at London.

Bharti Airtel’s Africa arm is planning a $1.5 to $2 billion IPO for Airtel Money, its mobile payments business, and the listing could value the unit at close to $10 billion. If that happens, it will be one of the largest fintech listings on a European exchange in recent years.

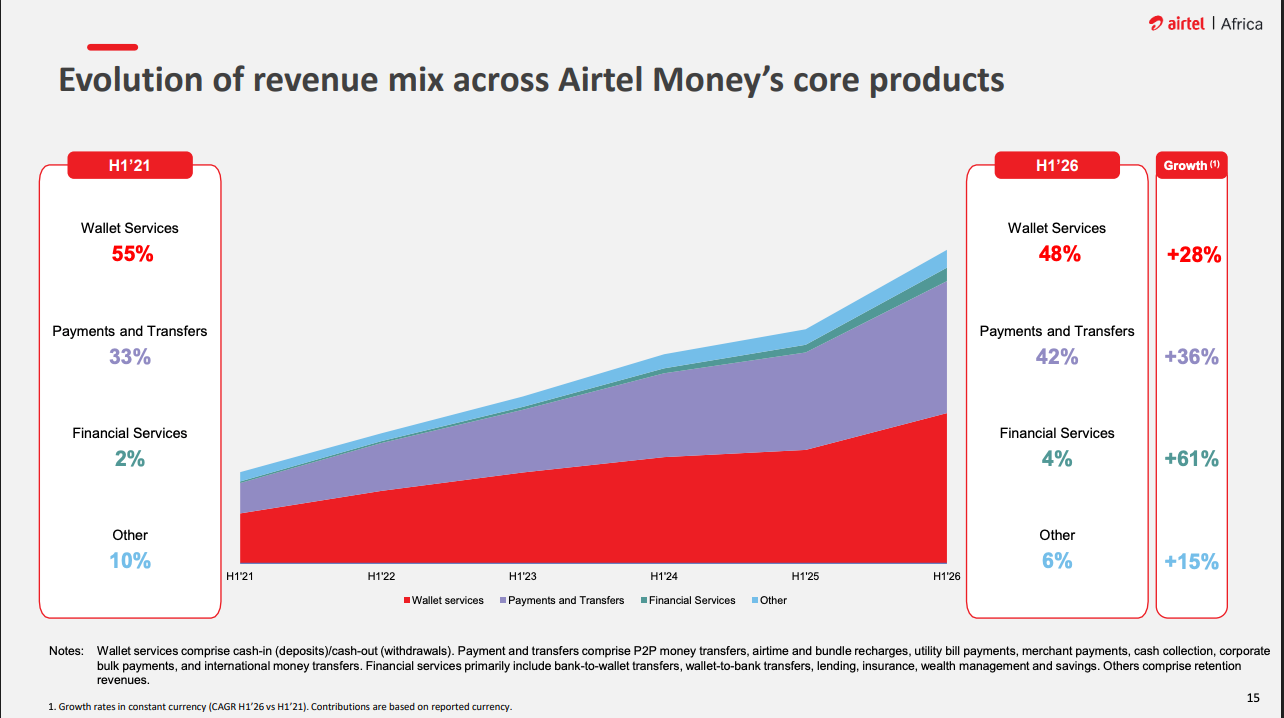

The business itself has been quietly scaling, with over 50 million users and transaction volumes that run into hundreds of billions of dollars annually. Revenues are growing fast, nearly 30% year on year, and the company has already attracted investors like Mastercard, TPG and Qatar’s sovereign wealth affiliates.

This may look like a simple IPO story. But it is actually a much deeper signal of how telecom companies are trying to reinvent themselves as financial giants, and why that strategy works in some markets but hits a wall in others like India.

To understand this, you have to go back to what mobile money really is.

In large parts of Africa, traditional banking infrastructure never reached everyone. Millions of people did not have bank accounts, but they had mobile phones. Telecom companies stepped into this gap and turned SIM cards into financial tools.

With Airtel Money, users can store value, send money, pay bills, and even access basic financial services without ever needing a bank branch. This is not just a payments app layered on top of a bank. It is often the primary financial system for many users.

That is why the numbers look the way they do. Airtel Money operates across 14 African countries, and in many of these markets, mobile money penetration is significantly higher than formal banking penetration. This gives Airtel a unique advantage.

It already owns the customer relationship through telecom, and it simply extends that into finance. Over time, this becomes a high-margin, sticky business because once users trust the platform with money, they tend to stay.

Now compare that with India, and the contrast is sharp. India did not skip banking infrastructure in the same way. Instead, it built a digital payments system that is arguably one of the most advanced in the world.

UPI alone processed over 22 billion transactions in a single month in 2026, with values touching nearly ₹30 lakh crore. It is free, interoperable, and backed by banks. This means no single private player can dominate basic payments in the way telecom-led wallets did in Africa.

Airtel tried a similar play in India through Airtel Payments Bank, but the scale and economics are very different. The bank has grown steadily, reporting over ₹2,700 crore in revenue and turning profitable, but it operates in a much more competitive ecosystem.

It is not competing with a handful of players. It is competing with UPI apps, traditional banks, fintech startups, and even Big Tech platforms. In India, sending money is no longer the business. It is the entry point.

This is where the story gets interesting. Airtel’s Africa business shows what happens when a company builds the rails and the service on top of it. India shows what happens when the rails are already public infrastructure.

In Africa, Airtel controls both distribution and the financial layer, which allows it to capture more value. In India, the infrastructure is shared, so companies have to move up the stack to make money through lending, insurance, wealth products or merchant services.

The IPO also tells you something about where global investors are looking next. Fintech growth in developed markets has slowed, and India’s payments space is crowded and tightly regulated. Africa, on the other hand, is still early in its financial digitisation journey.

A young population, rising smartphone penetration, and limited banking access create the perfect conditions for mobile money to scale. That is why investors are willing to value Airtel Money at close to $10 billion despite it operating in markets that were earlier considered risky.

For Bharti Airtel, this listing does two things. It unlocks value from a fast-growing business that is currently bundled within Airtel Africa, and it gives the company capital to expand further in these markets. It also quietly diversifies Airtel’s identity from being just a telecom operator to being a digital services company with strong fintech exposure.

At a broader level, this moment captures a shift that is happening globally. Telecom companies are no longer just carriers of data. They are becoming platforms that can layer multiple services on top of their user base.

But whether that strategy works depends heavily on the market structure. In places where financial infrastructure is weak, telecom companies can build everything from scratch and dominate. In markets like India, where digital public infrastructure is strong, they have to compete on innovation rather than access.

That is why Airtel’s biggest fintech success is not in its home market. It may be in Africa, where the rules of the game were different from the start. And now, with a potential $2 billion IPO on the table, that difference is turning into serious value.