Walk into a supermarket, pick up a Lux soap or a Lifebuoy bar, grab a pack of Lay’s or Doritos, maybe a Sprite or a Fanta, and it feels like you are choosing between rivals.

But in many cases, no matter what you pick, the money flows to the same company.

And this is not just a quirky coincidence.

In India, this “rivals on the shelf, siblings in reality” strategy is becoming sharper and more intentional in 2025 and 2026.

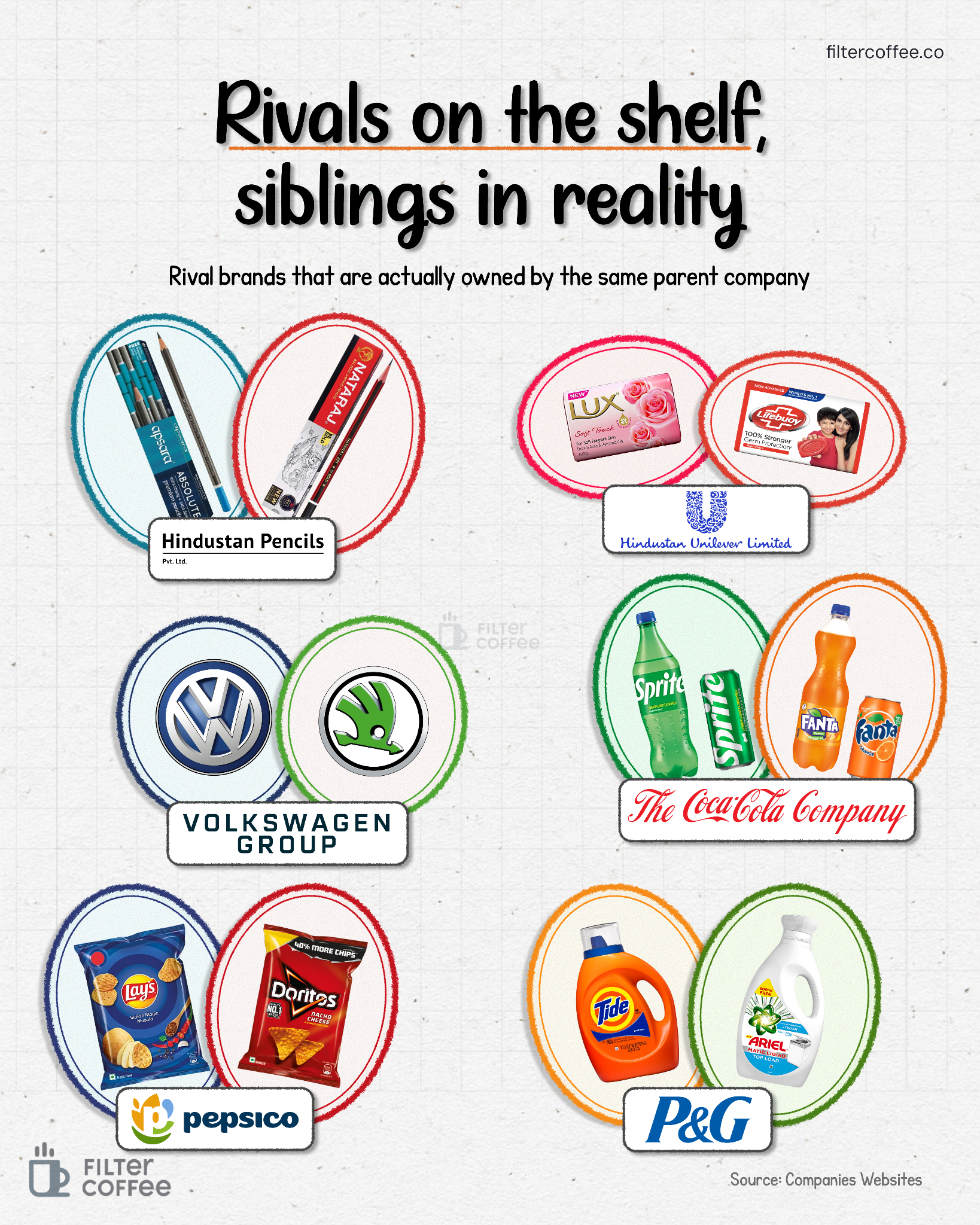

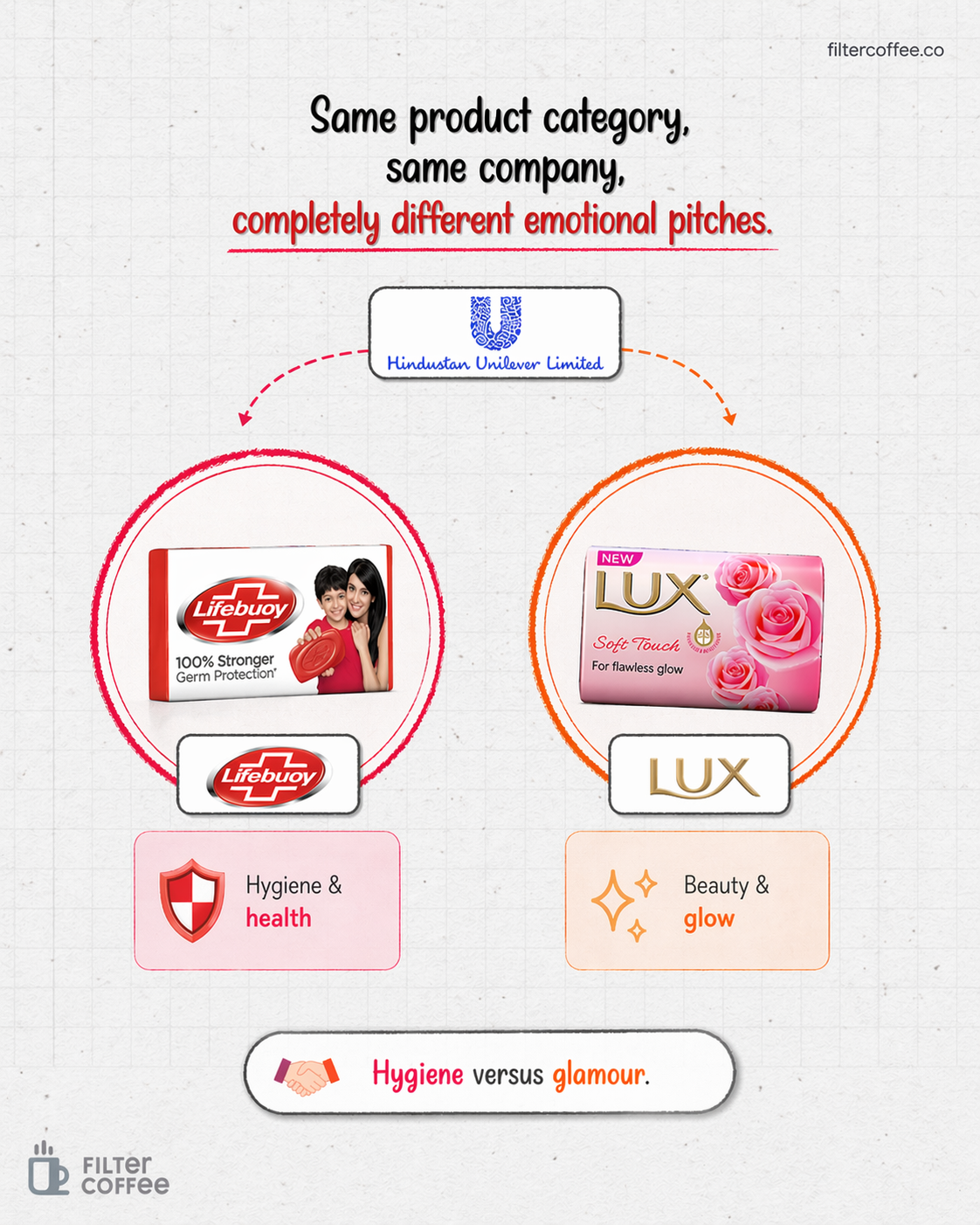

Take Hindustan Unilever. Lux and Lifebuoy compete for your attention in the soap aisle. But they are not fighting each other. They are dividing the market.

In FY25, HUL actively repositioned Lifebuoy from just a germ protection soap to a broader skin protection and health brand, even pushing it at large public events like the Maha Kumbh.

At the same time, Lux was relaunched with a stronger beauty and flawless glow positioning, with the company expanding its premium Lux International range.

Same product category, same company, but completely different emotional pitches. Hygiene versus glamour.

Now, let’s look at the snacks category more broadly.

PepsiCo owns both Lay’s and Doritos, and instead of letting them overlap, it is widening the gap.

In 2026, Lay’s underwent one of its biggest global refreshes in India, reinforcing its position as the familiar, everyday chip.

Meanwhile, Doritos is being pushed as bold and experimental, with new variants like Cool Ranch and Jalapeño Salsa Mexicana introduced in 2025.

And just to stretch the ladder further, PepsiCo has also brought in premium offerings like Red Rock Deli.

The strategy is simple. Whether you want safe, spicy, or premium, PepsiCo wants to own your craving.

The same playbook shows up in beverages.

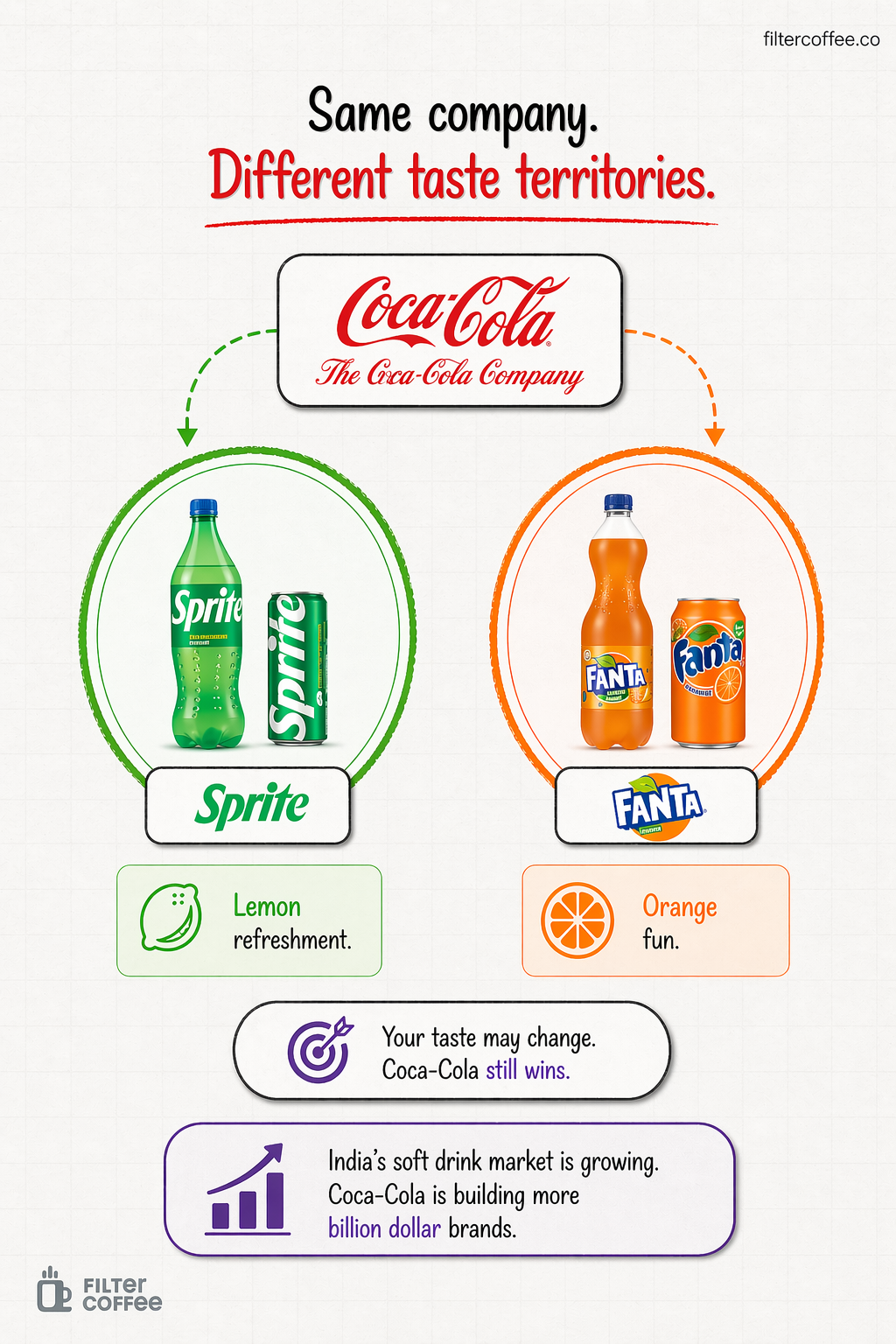

Coca-Cola sells both Sprite and Fanta, which seem like direct competitors are actually dominating different taste territories.

Sprite, now a billion dollar brand in India, plays in the clear lemon refreshment space. Fanta, on the other hand, holds more than 50 percent share in the orange flavoured soft drink segment.

So even if your taste flips between citrus and orange, Coca-Cola still wins. And with India’s soft drink market expanding, the company is doubling down on pushing multiple brands into the billion dollar league.

This is not limited to FMCG.

In the auto world, Volkswagen and Škoda appear to compete for similar buyers in India. But both sit under the Volkswagen Group, which is now doubling down on the country.

Škoda Auto India recorded its highest ever quarterly sales of over 20,000 units in early 2026, while the group is preparing a €1 billion India 3.0 investment plan.

What looks like competition in showrooms is actually coordinated expansion at the group level.

Even everyday categories like detergents follow this logic.

Brands like Tide and Ariel coexist within P&G’s portfolio, each targeting slightly different consumer segments. One leans more mass, the other more premium performance.

Yet together, they helped P&G Home Products cross ₹9,000 crore in revenue in FY25 with nearly 19% profit growth.

The rivalry exists only at the consumer’s eye level.

Recently, companies have not changed the existence of this strategy, but they have increased its intensity.

The rise of quick commerce platforms like Blinkit and Instamart means digital shelves now matter as much as physical ones.

Companies like HUL are building platform specific portfolios and increasing online availability year on year.

In a world where search results and thumbnails decide purchases, having multiple brands increases the chances of being seen, clicked, and bought.

So the next time you think you are choosing between two competing brands, pause for a second. Chances are, you are not picking a winner in a battle. You are simply choosing which version of the same company wins today.

And that is the real game. Not beating the competition, but becoming the competition.

Different brands, different moods, same company winning every time you choose.