Europe wants cleaner clothes.

China wants to dominate the material those clothes are made from.

And India is stuck somewhere in the middle trying to figure out whether it wants to build an industry or merely host factories for one.

That, in one sentence, is the story of lyocell right now.

A few years ago, almost nobody outside the textile industry had heard of this fabric. Today, it is becoming one of the most important fibres in global apparel manufacturing. H&M, Zara, Marks & Spencer, Decathlon and dozens of European fashion brands are actively increasing the share of “preferred fibres” in their products.

The European Union is tightening sustainability norms for textiles through regulations like the Ecodesign for Sustainable Products Regulation and the Digital Product Passport framework. Suddenly, the fashion supply chain is under pressure to prove not just where clothes are made, but what they are made from.

And that is pushing global brands toward fibres like lyocell.

To understand why this matters, it helps to understand how the modern clothing industry works. Most fabrics today come from two broad buckets. Natural fibres like cotton. And synthetic fibres like polyester, which is essentially derived from petroleum. Polyester dominates because it is cheap, durable and easy to mass produce. But it is also one of fashion’s biggest pollution problems. Every wash releases microplastics. It is fossil-fuel dependent. And Europe increasingly wants alternatives.

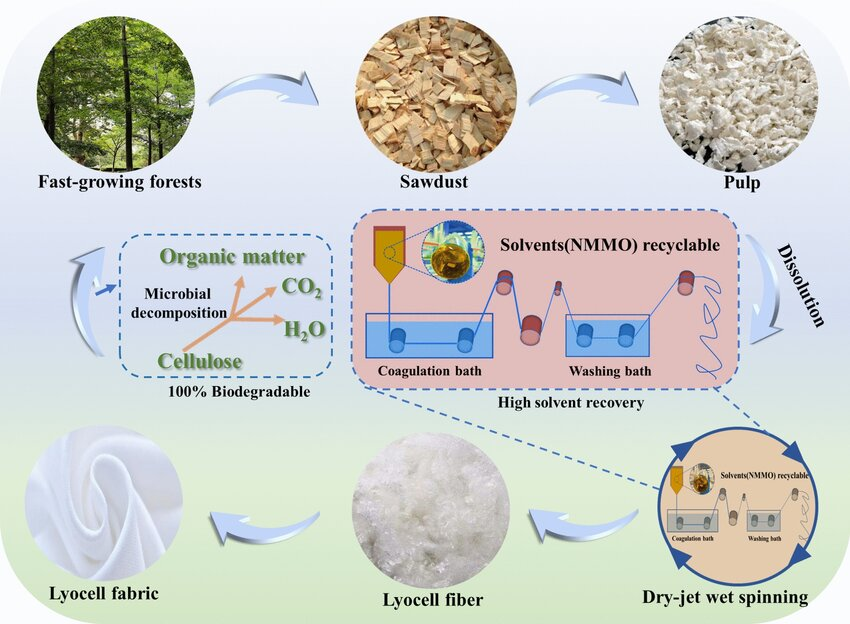

That created a massive opening for a third category called regenerated cellulosic fibres. These are fibres made from wood pulp. Think viscose, modal and lyocell. But among these, lyocell became the premium option because its chemistry solved one of the textile industry’s dirtiest problems.

Traditional viscose manufacturing uses toxic chemicals like carbon disulphide, which often leak into rivers and surrounding ecosystems. Lyocell uses a closed-loop solvent spinning process where nearly 99% of the chemicals get recovered and reused.

Image from: Research Gate

The fibre itself is biodegradable, breathable, softer than cotton, stronger when wet, and drapes like premium fabric. In the fashion industry language, it delivers both “performance” and “sustainability”. Which usually translates to higher margins.

That combination turned lyocell into one of the fastest-growing fibre categories globally. The global lyocell market was estimated at roughly $1.5-2 billion a few years ago and is expected to grow at high single-digit to low double-digit CAGR rates over the coming decade depending on the estimate. Europe especially became obsessed with it because regulators there are now actively restructuring textile imports around sustainability metrics.

And for once, India had an early lead in something advanced.

Aditya Birla Group, through Grasim Industries, built one of the world’s few commercial-scale lyocell plants at Kharach in Gujarat years before the category became fashionable. India was not merely stitching garments here. It was actually manufacturing an advanced textile material that the world wanted. That distinction matters because India’s textile industry has historically lived at the lower end of the value chain. Cheap labour, spinning, dyeing, garment exports. Rarely upstream technology.

The Indian government even supported some of this development through institutions like the Technology Development Board. At one point, this looked like the kind of industrial story policymakers dream about. India had capability. Europe had demand. China was relatively late.

Then China arrived properly.

And the entire economics of the industry changed.

The most important company here is Sateri, a subsidiary of Singapore-headquartered Royal Golden Eagle Group. Six years ago, Sateri did not manufacture lyocell at all. Today, it has become the largest producer in the world.

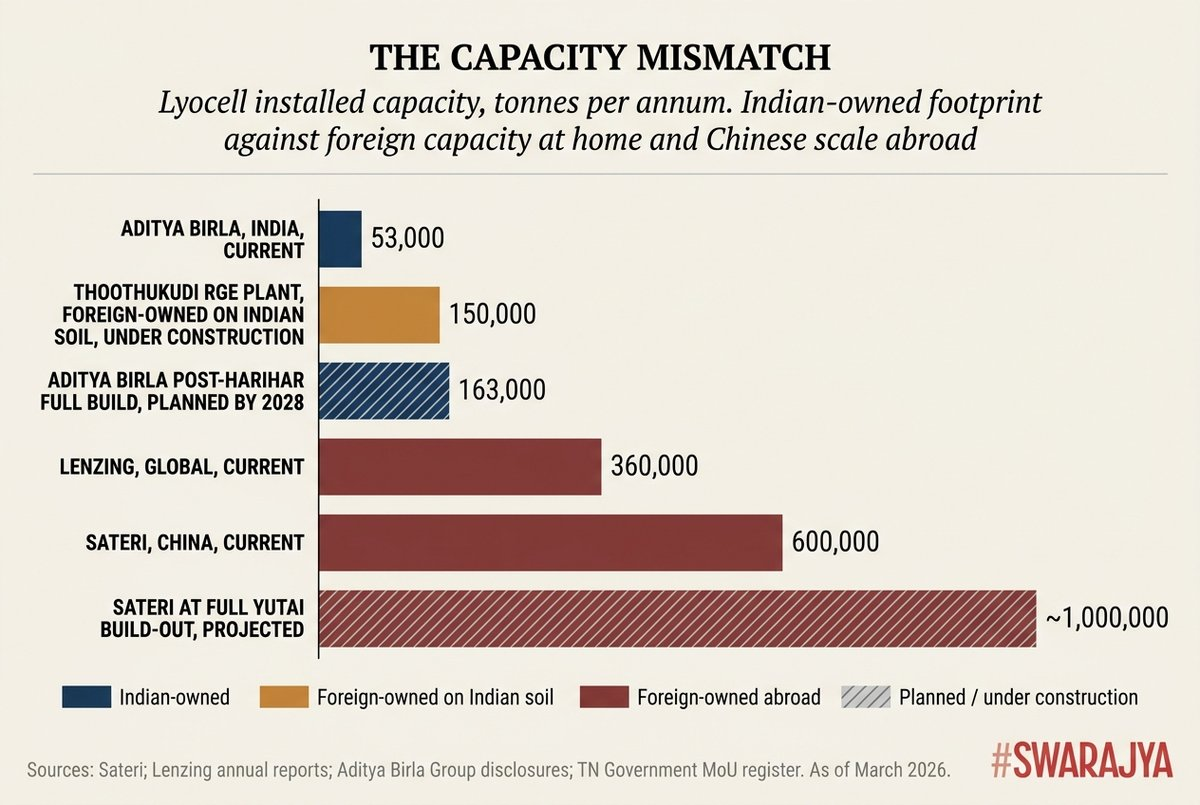

Its newest plant at Yutai in Shandong province started commercial production in March 2026. Once fully ramped up, this single facility alone will hold more lyocell capacity than the entire global industry had as recently as 2023. Across all facilities, Sateri now has roughly 600,000 tonnes of installed lyocell capacity and plans to move toward nearly one million tonnes eventually.

To put that into perspective, Aditya Birla’s current footprint is estimated around 50,000 tonnes. Even after Birla’s new expansion at Harihar in Karnataka gets fully built out, total capacity may reach roughly 110,000 tonnes. Sateri already produces several multiples of that.

And scale changes everything in manufacturing.

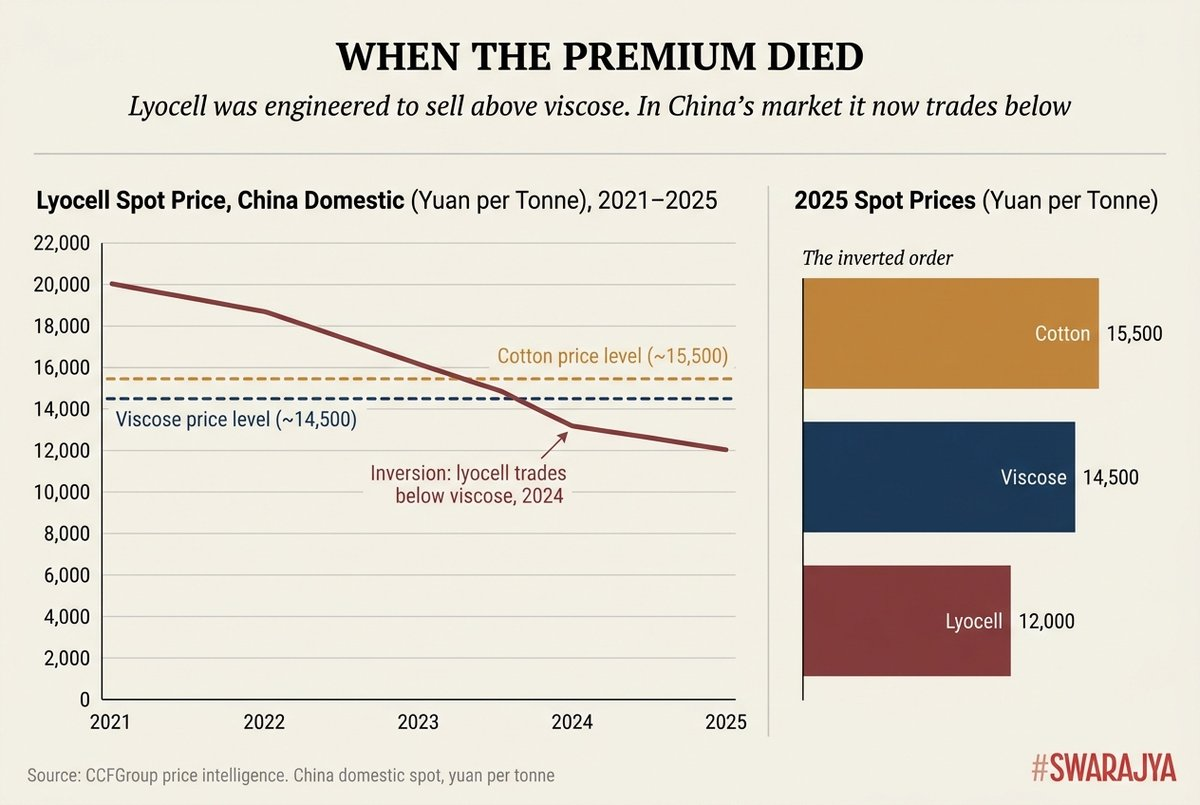

Lyocell was originally positioned as a premium fibre that could sell above cotton and viscose. But China’s giant capacity buildout has now crushed prices. In parts of China, lyocell reportedly trades below viscose prices itself. That is remarkable because viscose was supposed to be the cheaper, dirtier alternative.

This is starting to look eerily similar to what China previously did in solar panels, EV batteries and steel. Enter aggressively. Build huge capacity. Push prices down so hard that competitors struggle to survive. Then dominate global supply chains.

Even Lenzing, the Austrian company that invented lyocell and built its TENCEL brand into the global benchmark, is under pressure. Since 2021, Lenzing has lost roughly 80% of its market value. It scrapped a major US expansion project. And it is increasingly retreating from commodity-grade lyocell to focus on premium specialty segments where Chinese oversupply hurts less.

The interesting part is that India is simultaneously benefiting and losing from this shift.

In January 2026, after nearly nineteen years of negotiations, India and the European Union finally signed their long-awaited Free Trade Agreement. One major provision removes the 8-12% import duty Europe imposed on Indian textile exports. China does not get this advantage.

On paper, this should have been a huge opportunity for India. Europe’s textile market is worth over $260 billion. Sustainable fibres are among the fastest-growing categories inside it. India already has a massive garment manufacturing ecosystem. Add cheaper access to Europe and a domestic lyocell industry, and this should have been a strong export story.

But there is a catch.

Trade agreements help only if you have manufacturing depth ready to exploit them. And right now, China’s scale advantage is becoming overwhelming.

Worse, some of that Chinese-linked capacity is now entering India itself.

In August 2025, Tamil Nadu signed an MoU with RGE, Sateri’s parent company, for a 150,000-tonne lyocell plant in Thoothukudi. That single foreign-backed facility on Indian soil could eventually produce more lyocell than all of Birla’s Indian operations combined.

Which creates an uncomfortable question.

If India’s biggest opportunity in advanced manufacturing still depends on foreign-owned capital, foreign technology ecosystems and imported industrial strategy, how much value are we truly capturing?

Because industrial policy is not merely about attracting factories. It is about building ecosystems. China did not dominate sectors like batteries or solar by just offering cheap land. It built integrated supply chains, logistics networks, port infrastructure, chemical ecosystems, state financing support and massive scale simultaneously.

Sateri’s Chinese plants are deeply integrated with biomass power systems, wastewater treatment infrastructure and inland logistics. This is coordinated industrial development at scale. Not isolated factory announcements.

India still largely approaches manufacturing through MoUs, subsidies and tariff negotiations.

That matters because lyocell is not just another textile fibre anymore. It sits at the intersection of sustainability regulation, fashion supply chains, advanced materials and geopolitics. Europe wants cleaner textiles. Fashion brands want lower-carbon sourcing. China wants manufacturing dominance. India wants export growth.

Everyone wants the same market.

But not everyone is playing the same game.

Right now, India still has advantages. It has a large textile ecosystem, improving trade access to Europe, lower labour costs, and companies like Birla that already understand the chemistry and manufacturing process. If the EU’s sustainability push accelerates, demand for regenerated cellulosic fibres could rise sharply over the next decade.

But the bigger story here is not really about fabric.

It is about whether India can hold onto advanced manufacturing industries once China decides they matter.

Because India got into lyocell early. It had capability before the market exploded. It had domestic manufacturing before Europe’s sustainability shift fully arrived. And yet, within a few years, the scale gap has become enormous.

That is the real warning hidden inside this industry.

India may finally be entering the right sectors.

But it still struggles to industrialise at the speed needed to stay ahead once global competition arrives.