India’s electric scooter market just hit a turning point, and it’s not the one most people expected.

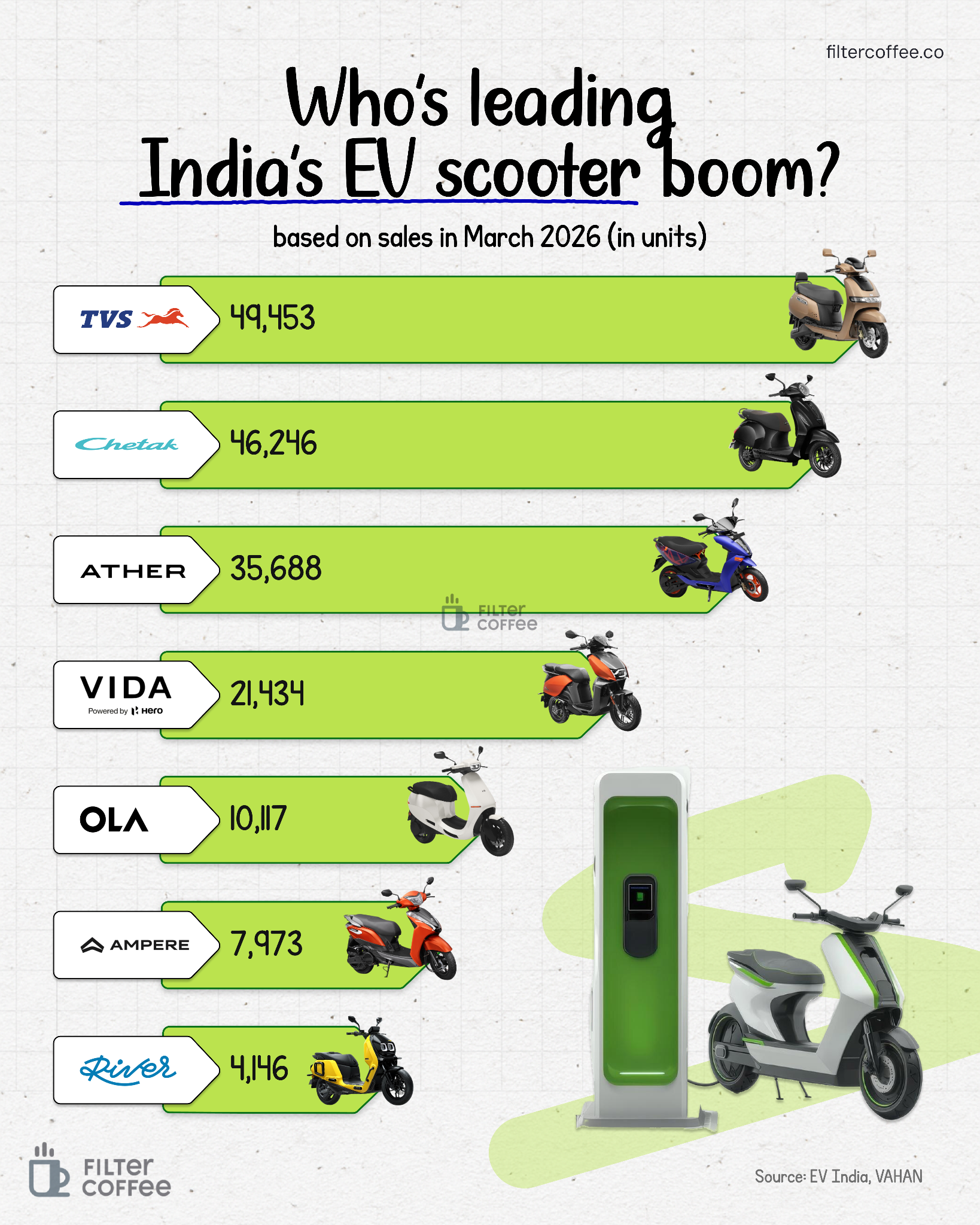

In March 2026, TVS sold about 49,000 electric scooters, edging past Bajaj’s Chetak at roughly 46,000 units, while Ather followed with over 35,000. Ola Electric, once the face of India’s EV revolution, sold just about 10,000 units that month.

This signals a deeper shift in how India’s EV two wheeler story is unfolding.

To understand why this matters, zoom out for a second.

March 2026 was not just any month. India clocked nearly 1.9 lakh electric two wheeler sales, making it the highest ever monthly figure. For the full financial year, the country sold about 14 lakh electric two wheelers, up more than 20 percent year on year.

Electric scooters alone now make up over half of all EV sales in India, and penetration has crossed 6.5 percent of total two wheeler sales. In simple terms, this is no longer a niche experiment. It is becoming a mainstream category.

But the real story is who is winning this mainstream race.

A couple of years ago, the narrative was simple. Startups like Ola and Ather were expected to dominate because they moved fast, built tech first products, and captured early consumer imagination. Legacy players were seen as slow and reactive.

However that script has now flipped.

TVS and Bajaj are leading the market not because they built the flashiest scooters, but because they solved the boring but critical problems of distribution, service, and trust.

When a product moves from early adopters to mass users, reliability starts to matter more than novelty, and that is where incumbents have an edge.

Take Bajaj for example. It did not just rely on the nostalgic appeal of the Chetak brand. It pushed into the mass market with models priced around one lakh rupees, offering practical range of over 120 kilometers and usable storage.

TVS followed a similar playbook, scaling its iQube lineup across cities with a strong dealer network.

These companies already had thousands of touchpoints across India, and that matters when your customer is not a tech enthusiast in Bengaluru but a daily commuter in a Tier 2 city who wants easy servicing and quick repairs.

At the same time, newer players are adapting.

Ather has expanded beyond its premium urban niche with family oriented scooters like the Rizta, which is helping it scale volumes.

Vida, backed by Hero MotoCorp, is emerging as a fast growing challenger, with sales jumping more than 150 percent year on year and cumulative numbers crossing 2 lakh units.

Even smaller players like River are carving out space by focusing on utility driven premium segments.

Ola’s story is more complicated. It is still innovating aggressively, launching new variants with higher range and investing in its own battery technology, but it is also restructuring and cutting costs.

Reports suggest it trimmed about 5 percent of its workforce in early 2026 as it tries to balance growth with profitability.

Policy is also quietly shaping this shift.

The government has extended incentives for electric two wheelers under schemes like PM E DRIVE until mid 2026, keeping upfront costs lower for buyers.

At the same time, states like Delhi are planning aggressive transitions, even proposing that only electric two wheelers be registered from 2028 onward. This combination of short term subsidies and long term mandates is creating both demand and certainty for manufacturers.

Put all of this together and the EV scooter boom in India starts to look very different from the hype cycle it began with.

This is no longer about who launches the coolest product or raises the most funding but about who can build a full stack business that works at scale in India’s chaotic, price sensitive, service heavy market.

The leaders today are the ones who understood that early. And if the March 2026 numbers are any indication, the race is far from over, but the rules of the game have already changed.