India’s auto market just had another record year, but the real story is not who sold the most cars, it is who investors believe will win the future.

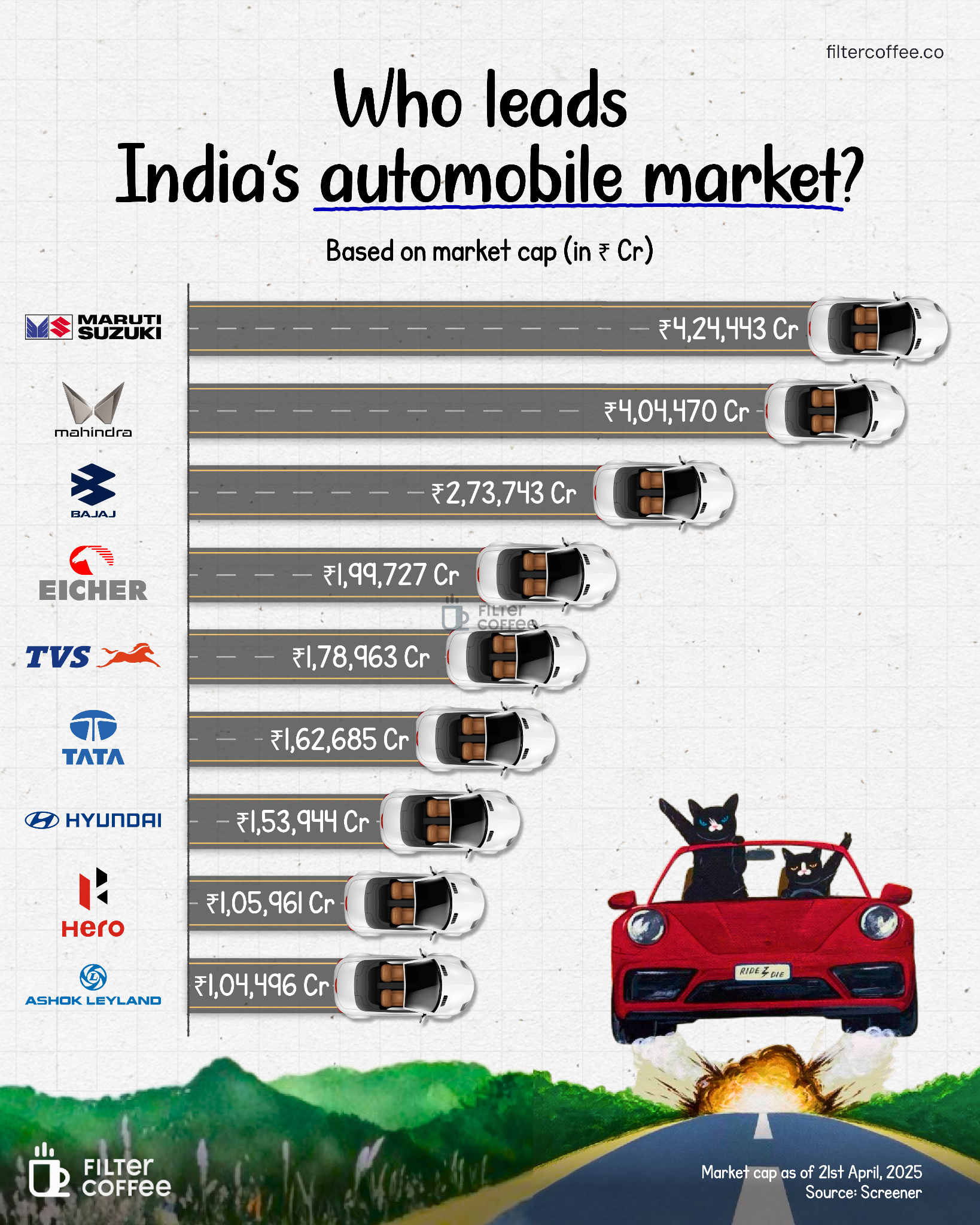

As of April 2025, Maruti Suzuki sat at the top with a market cap of about ₹4.2 lakh crore, closely followed by Mahindra at ₹4.0 lakh crore, with Bajaj Auto a distant third.

That ranking still mostly holds true in 2026. However, the focus is shifting from sheer scale to the narratives behind it, and those are changing fast.

To start with, Maruti is still the clear volume leader in India.

In FY26, it sold over 18.2 lakh passenger vehicles domestically and crossed 2.4 million total units. Yet, despite that dominance, its lead in market cap over Mahindra is surprisingly narrow. Why? Because the market isn’t rewarding size alone anymore. It’s rewarding how a brand positions itself.

India’s car market has transformed into an SUV-first market.

Utility vehicles now make up well over half of all passenger vehicle sales. This shift has played directly into Mahindra’s strengths.

In FY26, Mahindra sold about 6.6 lakh passenger vehicles and overtook both Tata Motors and Hyundai to become the number two carmaker in the country. That is a massive shift in a market that was once predictable.

Investors have noticed that Mahindra is now seen as a premium SUV powerhouse with strong pricing power and long waiting lists.

Meanwhile, Tata Motors tells a completely different story. It is not leading in total volumes, but it dominates the EV narrative.

In FY26, Tata sold over 92,000 electric cars and still held roughly 40% of India’s EV passenger vehicle market.

But that lead is shrinking.

Mahindra has already pushed its EV share to nearly 24%, and Maruti has finally entered the EV race with the e Vitara, offering a claimed range above 500 km.

So the EV race isn’t just about one player anymore. It’s getting crowded, more competitive, and a lot more interesting.

Then there is Hyundai, which used to be the clear number two in India for years.

In FY26, it slipped to fourth place in passenger vehicle sales with about 5.8 lakh units. It’s not a collapse, but it shows how quickly the ground is shifting. What worked before isn’t a given anymore.

The two-wheeler side adds another layer.

Companies like TVS and Bajaj are being re-rated because they are proving they can win in electric mobility.

TVS alone sold over 3 lakh electric two-wheelers in FY26, while Bajaj’s Chetak continues to scale. Even Hero MotoCorp, once seen as slow in EVs, has crossed 2 lakh VIDA deliveries.

It matters because electric two-wheelers account for more than half of all EV sales in India, which crossed 24.5 lakh units in FY26.

Zoom out and the macro picture becomes clearer, India’s auto industry is growing, but not evenly.

Passenger vehicle sales hit a record 46.4 lakh units in FY26, up nearly 8%. Commercial vehicles grew over 12% to cross 10.8 lakh units, helped by infrastructure and logistics demand.

EV adoption is accelerating, with electric passenger vehicle sales surging 84% to nearly 2 lakh units in FY26.

At the same time, policy is shifting from subsidies to manufacturing.

Schemes like PM E DRIVE and the new EV manufacturing policy are pushing companies to invest thousands of crores locally.

So when you look back at that market cap chart, it isn’t just a ranking, it shows where the market thinks the future is going.

Maruti still represents scale and consistency. Mahindra represents the SUV boom.

Tata represents the EV bet. Bajaj and TVS represent the transition of two-wheelers into an electric future.

And that is the real takeaway. India’s auto market is no longer about who sells the most vehicles today. It is about who is best positioned for what Indians will drive tomorrow.