India’s listed hotel companies are planning to add more than 70,000 rooms by FY30. That sounds like a simple expansion plan, but it is actually a signal that something deeper has shifted in how India travels, spends, and builds.

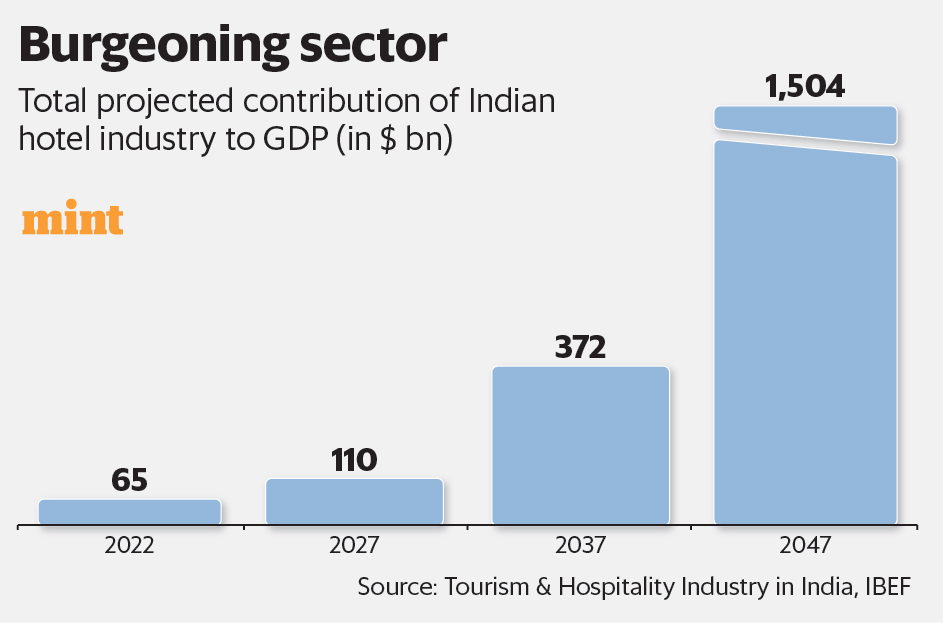

For context, India’s hotel industry is now expected to grow from about $24.6 billion in 2024 to roughly $31 billion by 2029. That is not explosive growth but backed by something far more important than foreign tourists, which is domestic demand.

In 2025 alone, domestic travel surged enough to push total visits to around 4.1 billion, a massive 40% year-on-year jump. Even as foreign tourist arrivals dipped to about 90 lakh in 2025, the sector kept growing. That tells you the engine has changed. India is now travelling within India, and that is enough to sustain an entire industry.

Now here is where it gets interesting.

This is not just about more hotels. It is about what kind of hotels are being built. Around 60% of new openings are concentrated in upper-midscale, upscale, and luxury categories. In simple terms, people are not just travelling more, they are also upgrading how they travel.

The rise of destination weddings, curated vacations, spiritual tourism, and even weekend luxury stays has pushed hotel companies to chase higher room rates instead of just higher occupancy.

In 2025, occupancy levels reached around 64%, which is healthy, but the bigger story is pricing power. Revenue per available room grew 11% year-on-year, while average daily room rates increased by 8.7%. Hotels are making more money per room, not just filling more rooms.

This also shows up in how companies are expanding.

Earlier, growth meant building expensive properties from scratch. Today, most large players are going asset-light. Indian Hotels Company is targeting over 700 hotels by 2030, largely through management contracts and partnerships rather than owning everything.

Lemon Tree already has more than 17,000 rooms across operational and pipeline inventory and is pushing toward 20,000 rooms by the next few years, focusing heavily on mid-market expansion.

ITC Hotels is doing something similar, but with a sharper tilt toward premium brands, scaling its presence without tying up too much capital. The idea is simple. Grow fast, spend less, and earn through management fees and brand power.

At the same time, money is flowing into the sector again. In 2025, hotel deal values jumped to around $456 million, nearly 2.5 times the previous year.

Private equity firms and institutional investors are no longer treating hotels like a risky side bet. They are seeing them as long-term assets with steady cash flows. The Leela operator, Schloss Bangalore, even tapped public markets with one of the largest hospitality IPOs, signalling that capital markets are now open to this space.

When both private and public money start showing up together, it usually means the industry has moved past survival mode.

Another layer here is geography. This boom is not just happening in Mumbai, Delhi, or Bengaluru. A lot of new supply is heading into tier 2 and tier 3 cities, and even religious hubs like Ayodhya, Varanasi, and Puri. These are places where demand used to be seasonal or unorganised. Now they are becoming year-round travel markets with branded hotels stepping in. Infrastructure is playing a big role here, with better highways, airports, and rail connectivity making these locations more accessible than ever before.

But there are a few ground realities. Hotel pipelines always look bigger than what actually gets delivered.

Construction delays, approvals, and funding issues tend to slow things down. Even in 2025, despite record signings of nearly 47,000 rooms, actual completions lagged behind. On top of that, external disruptions like aviation issues or geopolitical tensions can quickly impact travel demand. So while the outlook is strong, execution is still a big question mark.

Still, the direction is clear. India’s hotel industry is no longer just recovering from Covid. It has entered a new phase where demand is deeper, pricing power is stronger, and capital is more willing to back growth. What started as a rebound story has quietly turned into a scale story. And if 70,000 new rooms actually get built over the next few years, it will not just mean more hotels. It will mean a very different kind of travel economy taking shape in India.