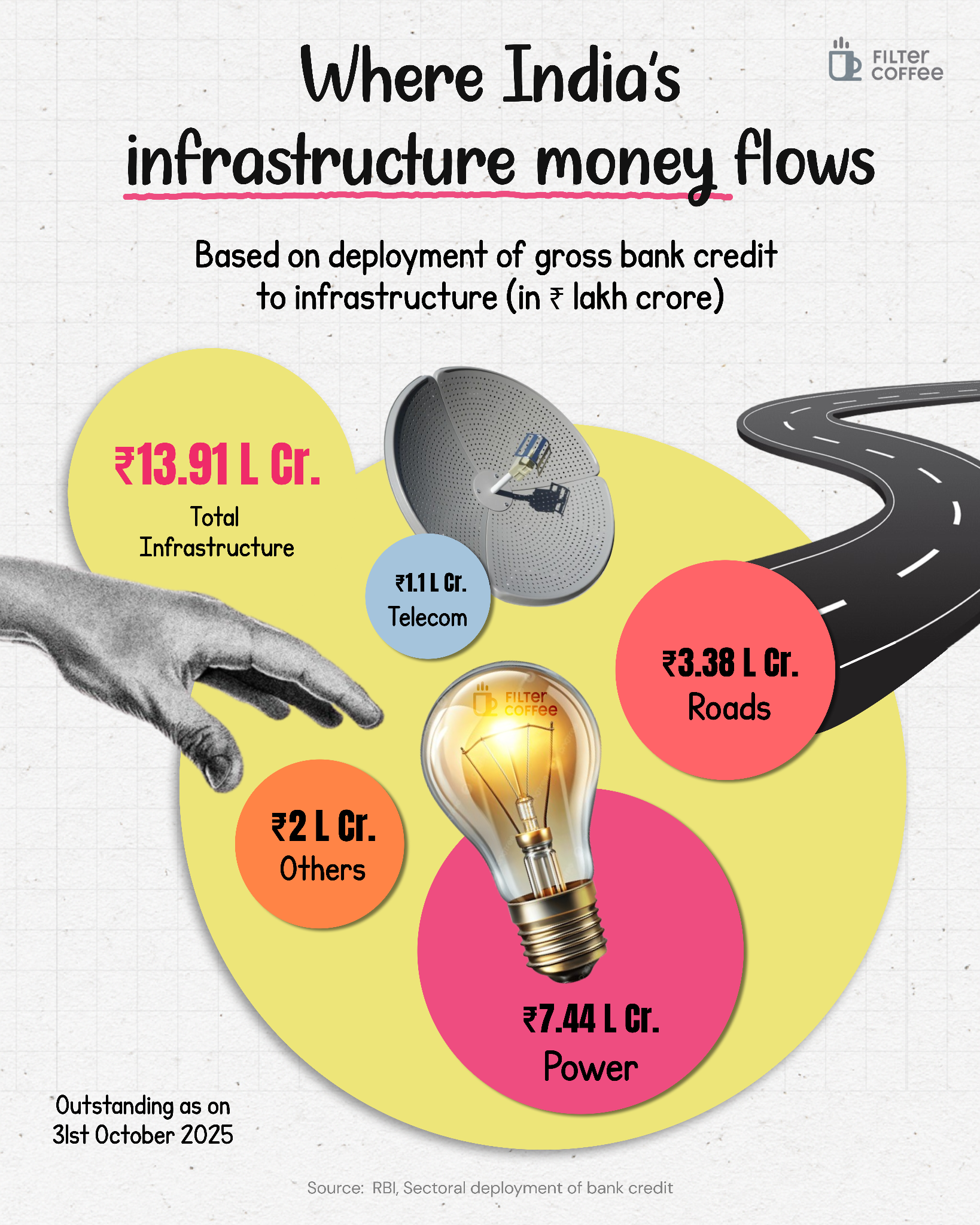

India’s infrastructure lending just revealed something interesting.

As of October 2025, banks had deployed close to ₹14 lakh crore into infrastructure. And if you zoom into where that money is going, the pattern is very clear. Power alone accounts for over ₹7.4 lakh crore. Roads come next at around ₹3.3 lakh crore. Everything else, including telecom, sits much lower.

Let’s start with power.

India is not just building more electricity capacity, it is completely rewiring how power flows. There is a massive push towards renewables, grid upgrades, storage systems, and even green hydrogen. The government has already lined up investments of over ₹9 lakh crore just for transmission infrastructure by 2032.

Add to that the ₹19,700 crore green hydrogen mission and the ongoing renewable energy expansion, and you start to see why banks are heavily exposed here. Power is no longer a static sector. It is becoming the backbone of everything from EVs to data centres.

Then come roads. India has been building highways at a scale we have never seen before. The national highway network has expanded from about 91,000 km in 2014 to over 1.46 lakh km today. Annual capex on highways alone has crossed ₹3 lakh crore. This is not just about faster travel. Roads unlock logistics, reduce costs for businesses, and connect smaller cities into the formal economy. Which is why lenders are comfortable backing these projects.

The cash flows are relatively predictable once traffic stabilises.

Now here is where things get more interesting. Telecom, despite being critical, has a much smaller share in bank credit. But that does not mean it is not growing. The government is spending over ₹1.39 lakh crore on BharatNet to connect 2.6 lakh gram panchayats with fibre. Over 2.18 lakh have already been connected. The difference is in how it is being funded. Telecom is increasingly driven by policy spending, private capex, and strategic investments rather than heavy bank lending.

But the real shift is happening behind the scenes. India is slowly moving away from a system where banks carry the entire burden of infrastructure financing. That model has not always worked well. Long-term infrastructure projects and short-term bank deposits are not a perfect match. That mismatch has caused stress in the past.

So now, the financing model itself is evolving. The government has ramped up capital expenditure from ₹2 lakh crore in FY15 to over ₹12 lakh crore planned for FY27. At the same time, institutions like NaBFID are stepping in to provide long-term funding. India’s infrastructure pipeline now includes nearly 9,000 projects worth over $1.5 trillion.

New layers are being added. Development finance institutions, multilateral agencies like ADB and AIIB, municipal bonds, and structures like InvITs are all becoming part of the ecosystem. Even a new Infrastructure Risk Guarantee Fund is being introduced to make projects more attractive for private investors.

So when you look back at that simple chart, it is not just about where money is flowing today. It is about how India is building its future. Power and roads are getting the bulk of funding because they are foundational. But the way this money is being raised and deployed is changing rapidly.

And that might be the bigger story here.

India is no longer just building infrastructure. It is building a full-fledged financing system around it.

Also read: Can one InvIT fund India’s next decade?