India just made a pretty bold move in the data centre game. In the Union Budget 2026, the government quietly announced a tax holiday for foreign companies building global cloud and data infrastructure in India, valid all the way till 2047. Around the same time, Google said it plans to invest about $15 billion to build its first AI-focused data centre hub in Visakhapatnam. And Yotta, one of India’s largest data centre players, is setting up a massive AI cluster powered by over 20,000 NVIDIA Blackwell GPUs, expected to go live in 2026.

hat is a signal. India is no longer just catching up in digital infrastructure. It is trying to become a serious global hub for cloud and AI.

To understand why this matters, start with something simple. The internet is not floating in the air. Every WhatsApp message, Netflix binge, UPI transaction, and ChatGPT query runs through physical buildings packed with servers. These are data centres. Think of them as warehouses for the internet.

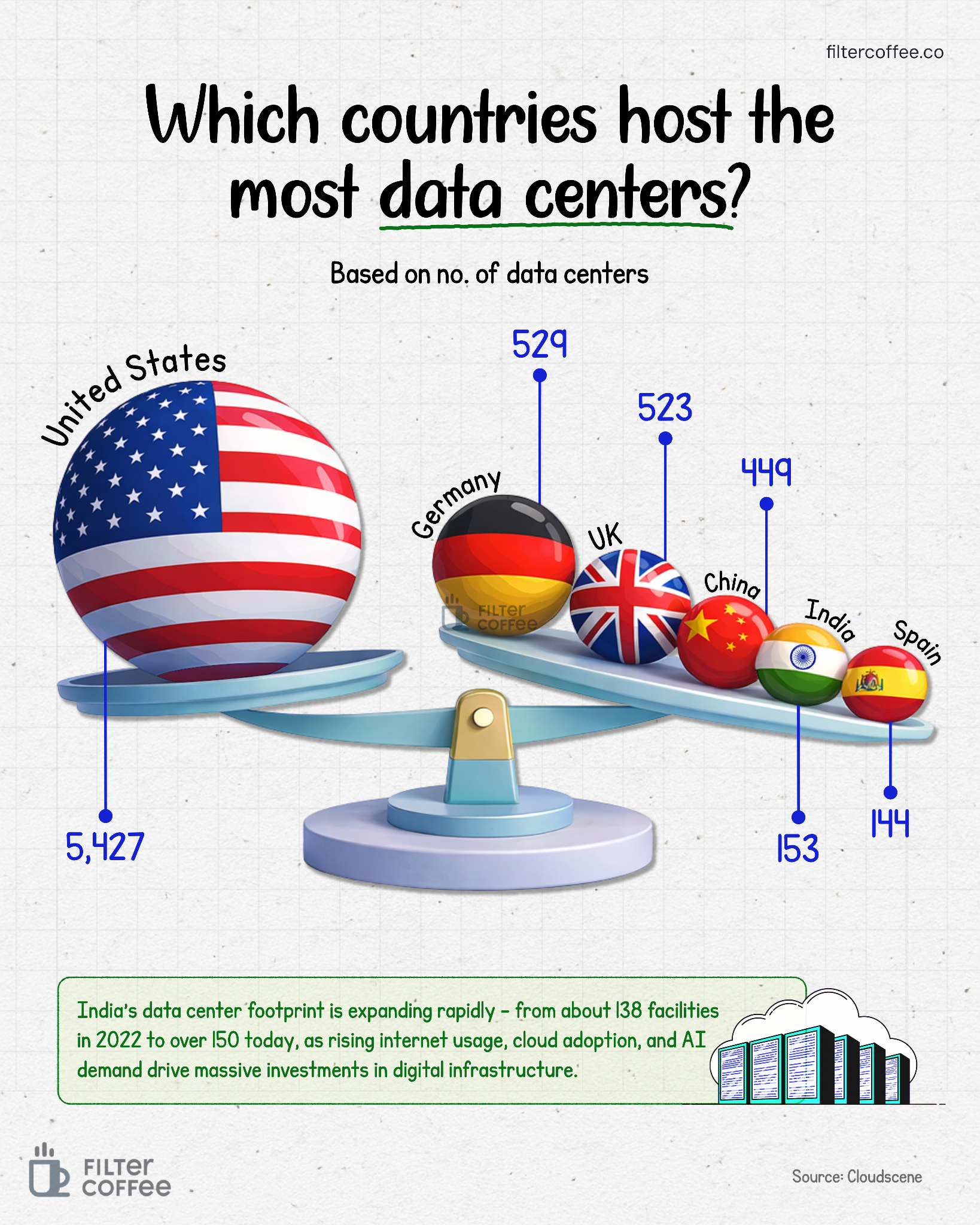

Globally, the US is still the king here, with over 5,400 data centres. Europe follows, with countries like Germany and the UK having over 500 each. India is still smaller in comparison, with roughly 150 to 180 facilities depending on how you count them. But here is where things get interesting. Counting buildings is misleading. What actually matters is capacity, basically how much computing power these centres can handle.

And this is where India’s story gets serious. As of mid-2025, India has already crossed roughly 1.2 to 1.3 gigawatts of installed data centre capacity. That might sound abstract, but it is growing fast. Projections suggest India could reach 4 gigawatts by 2030. That is more than a 3x jump in under a decade.

Why is this happening now?

First, demand is exploding. India has over 900 million internet users, one of the cheapest data costs globally, and a digital economy that runs on UPI, ONDC, streaming, gaming, and now AI. Every one of these needs storage and compute power.

Second, data localisation is becoming a thing. Regulators want sensitive data, like financial and government data, stored within India. That pushes companies to build local infrastructure instead of relying on overseas servers.

Third, AI has changed the game. Traditional cloud workloads are heavy. AI workloads are insane. Training models, running inference, storing datasets, all of this requires far more power, cooling, and specialised chips. That is why you are seeing players like Yotta investing in GPU clusters and global giants like Google betting billions.

Fourth, the government is actively nudging the sector. The tax holiday till 2047 is basically a long-term assurance to global players. Add to that state-level incentives, faster approvals, and infrastructure support, and India starts looking like a viable alternative to saturated markets like the US and Europe.

But the ecosystem is not evenly spread. Mumbai still dominates with more than half of India’s capacity, thanks to subsea cable connectivity and financial demand. Chennai, Hyderabad, and Delhi NCR are catching up fast. Even tier 2 locations are entering the chat as land and power costs in metros rise.

Of course, it is not all smooth. Data centres are power-hungry. A single large facility can consume as much electricity as a small town. India already struggles with power reliability in some regions. Then there is the issue of cooling. These facilities generate insane heat, and managing that efficiently is both expensive and environmentally tricky. Land acquisition, fibre connectivity, and skilled workforce are other bottlenecks.

But despite these challenges, the direction is clear. The conversation has shifted. A few years ago, India was asking how many data centres it has. Today, the real question is how much compute power it can build and how quickly it can scale for AI.

And that shift matters. Because the next decade of economic growth will not just be about roads, ports, and factories. It will be about servers, chips, and data. And for once, India is not late to the party. It is trying to host it.