For years, the biggest fear around department stores was simple. Nobody knew if they would survive the internet.

Consumers had stopped depending on one giant retail store for everything. Fashion moved online. Beauty moved to Nykaa. Sneakers moved to niche apps. Luxury shifted to brand-owned stores. Fast fashion exploded through Zara, H&M and increasingly Zudio. Even gifting became an Instagram business.

So somewhere along the way, stores like Shoppers Stop started feeling like leftovers from an older version of urban India.

But its latest earnings tell a very different story.

Not because the company delivered extraordinary profits. In fact, profitability is still under pressure. But because the numbers reveal something far more important. Indian consumers are shopping differently now. They are spending more on premium products, beauty, fragrances, experiences and loyalty-driven retail ecosystems. And Shoppers Stop has quietly repositioned itself right in the middle of that shift.

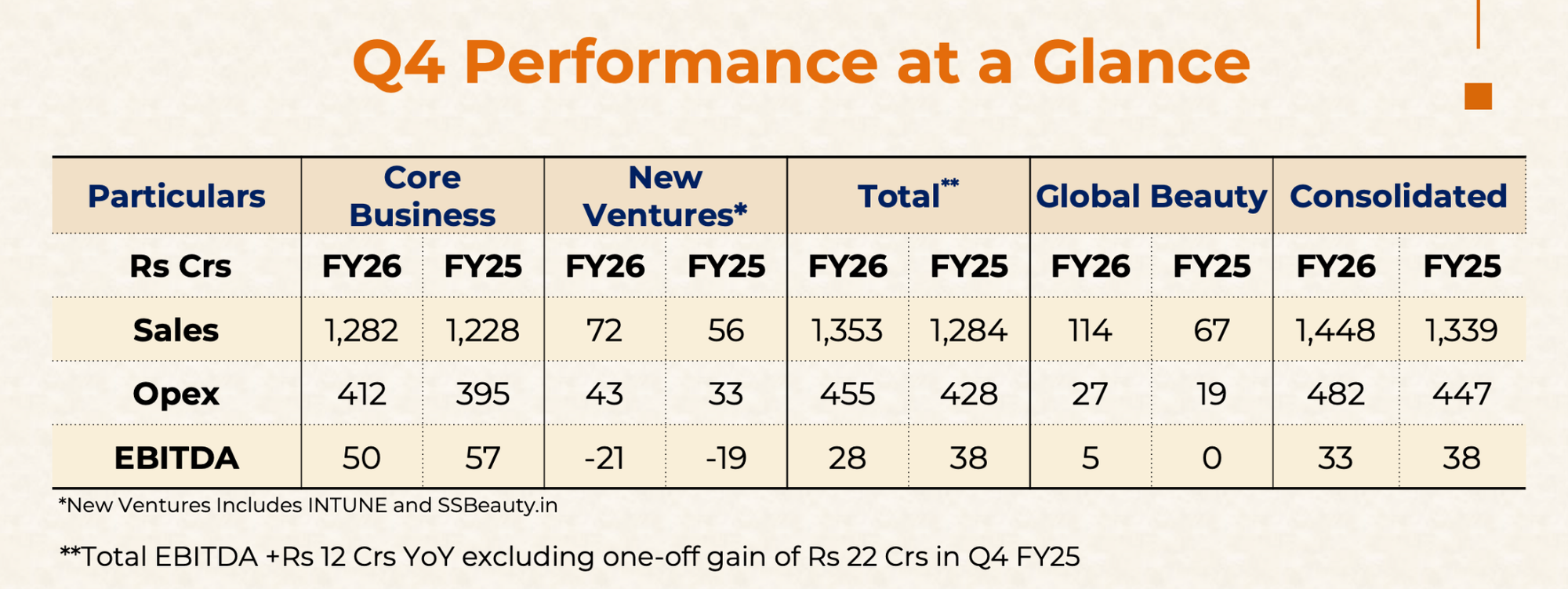

In Q4 FY26, the company reported consolidated revenue of ₹1,210 crore, up 14% year-on-year. Annual consolidated gross revenue crossed ₹6,057 crore, growing 8% over last year. Department store like-for-like sales grew 4.7%, which management says is the highest in a decade.

Like-for-like sales basically measure growth from existing stores rather than newly opened outlets. That makes the metric important because it shows whether older stores are genuinely attracting more spending or whether revenue growth is simply coming from expansion.

In Shoppers Stop’s case, existing stores themselves are performing better, suggesting that customer demand has strengthened meaningfully. More importantly, this growth is not being driven by mass discounts or basic essentials.

But then comes the contradiction.

Despite revenue growth, Shoppers Stop slipped into a quarterly net loss of around ₹17 crore compared to a profit of ₹2 crore in the same quarter last year. Non-GAAP EBITDA fell 11%, and margins narrowed despite stronger sales.

> Non-GAAP EBITDA is basically a company’s way of showing its “core operating performance” by removing certain accounting or one-time expenses that it believes distort the real business picture

So naturally, the question becomes obvious. If customers are spending more, then why are profits weakening?

The answer is that Shoppers Stop is no longer behaving like a traditional department store company trying to maximise short-term profits. It is trying to rebuild itself into something much larger. A premium retail ecosystem built around beauty, aspirational fashion, memberships, experiences and affluent urban consumption.

And building that ecosystem is expensive.

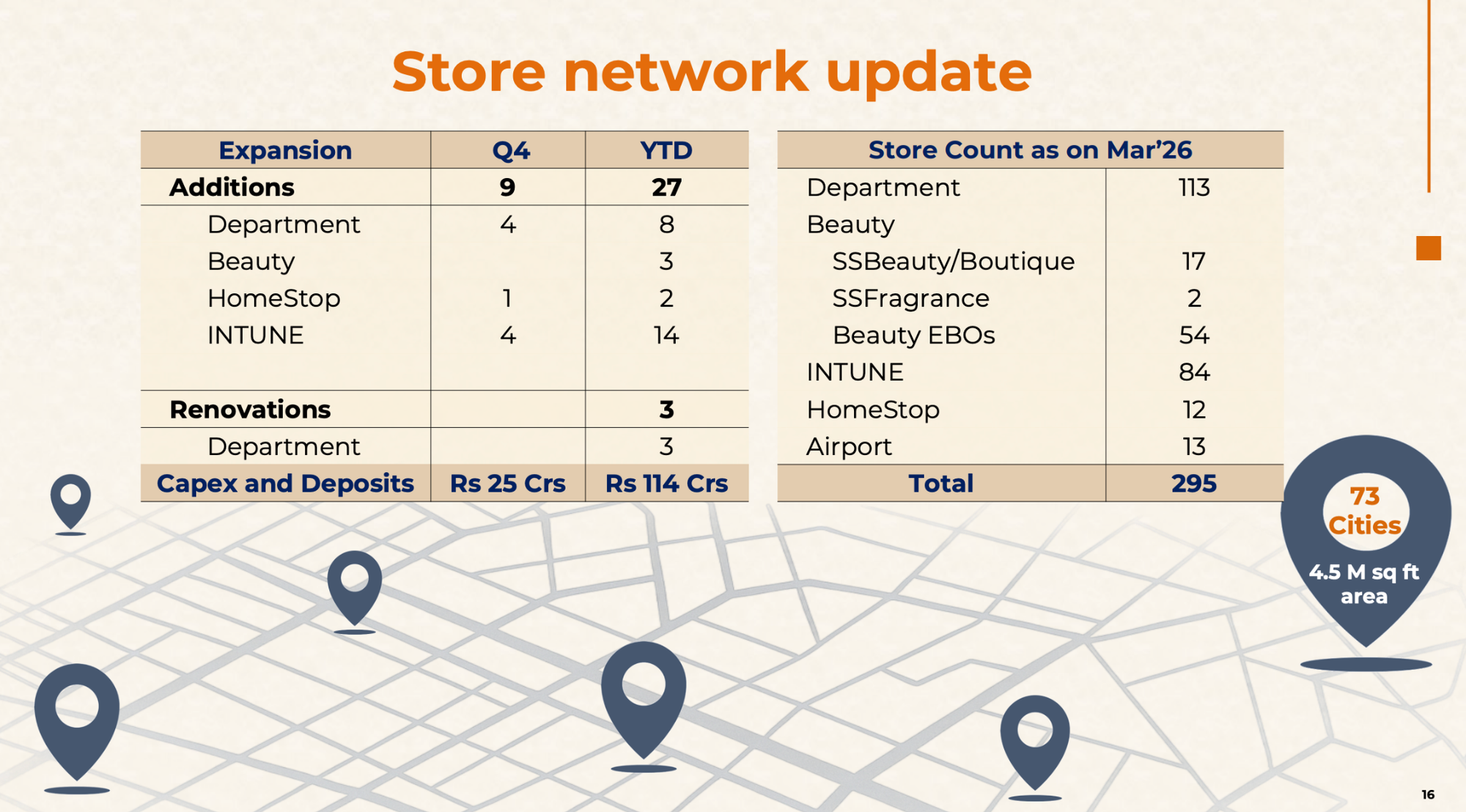

The company opened 27 stores during FY26, including 14 INTUNE stores, 8 department stores, 3 beauty stores and 2 HomeStop outlets. It spent ₹114 crore on capex. It renovated flagship locations like the Juhu store with upgraded premium layouts and aspirational merchandising. It continues to invest heavily in loyalty programs, CRM systems, beauty expansion and private brands.

This means the company is currently absorbing expansion costs while simultaneously trying to upgrade its positioning.

But beneath the profitability pressure, the operating story actually looks quite strong.

The clearest sign is that people walking into Shoppers Stop stores are spending meaningfully more money. Average transaction value rose 8% in Q4. So if a shopper earlier spent around ₹4,900 per visit, they are now spending over ₹5,300. Average selling price rose 11% to ₹1,926.

That is not the kind of growth you see when retailers are aggressively discounting inventory. It is premiumisation-led growth.

And premiumisation is basically the central thesis behind the business now.

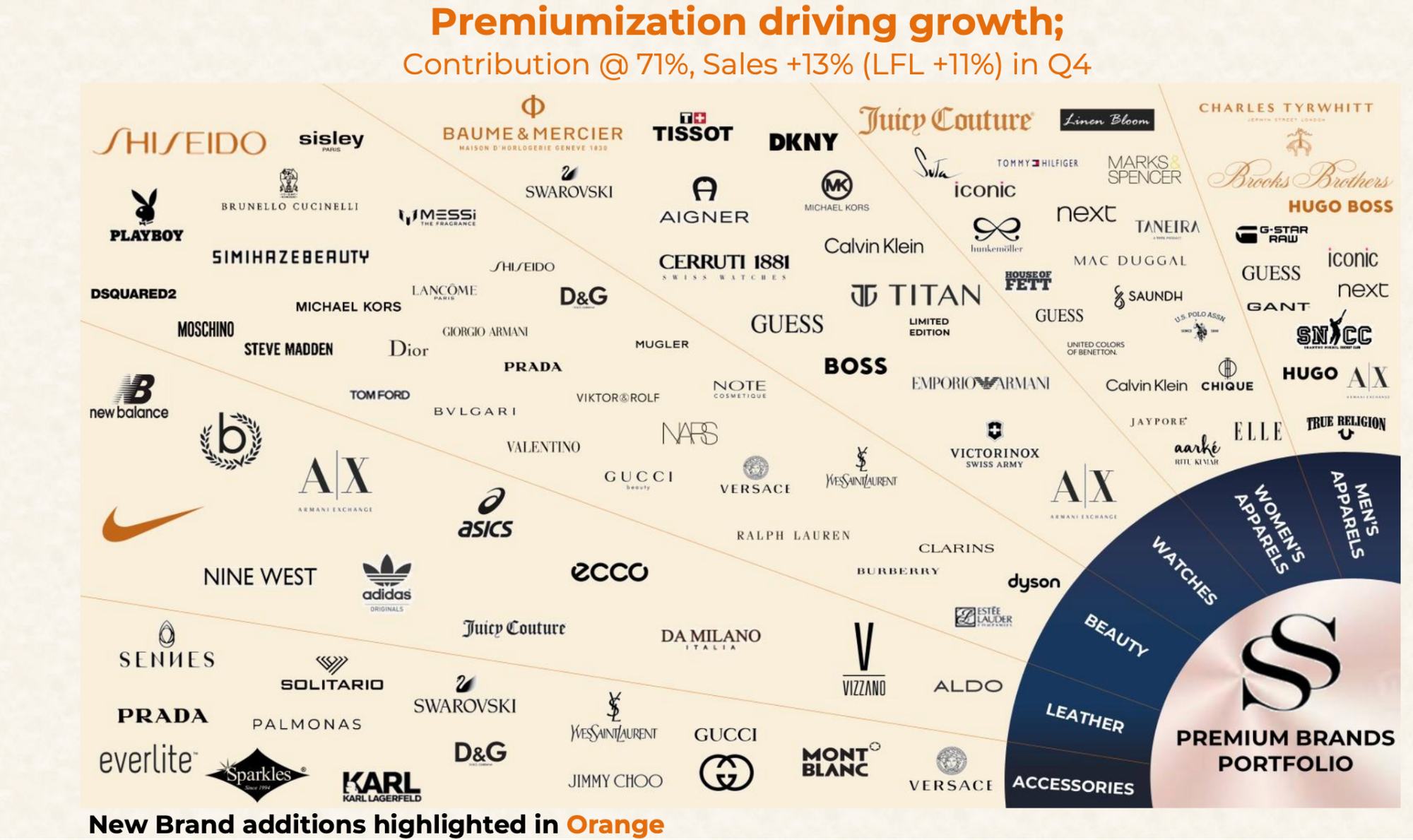

Premium brands contributed 71% of total sales during the quarter and grew 13% year-on-year with 11% like-for-like growth. The company has been aggressively adding aspirational labels like Hugo Boss, Brooks Brothers, Charles Tyrwhitt and Baume & Mercier because management clearly believes affluent Indian consumers are entering a stronger discretionary spending cycle.

What makes this especially interesting is that the strongest-performing categories were not core apparel categories. Watches grew 21%, handbags grew 13% and fragrances within the core retail business grew 15% during the quarter.

The company sold 150 fragrance units every hour during FY26 and 70 watches every hour. Modern Indian retail is increasingly shifting toward higher-margin, non-essential and identity-driven consumption where consumers are buying lifestyle signals as much as products.

This trend becomes even clearer in beauty. Shoppers Stop’s overall beauty business grew 17% year-on-year in Q4 to ₹309 crore, while the fragrance segment within beauty emerged as the fastest-growing category with 37% growth.

And this is not happening in isolation.

India’s beauty and personal care market is expected to touch nearly $40 billion by 2030 and become the fourth-largest beauty market globally. Consumption habits are changing rapidly, especially among younger urban consumers. Ten years ago, many Indian consumers owned one moisturiser, one lipstick and maybe a kajal pencil. Today, routines include serums, sunscreens, blushes, lip oils, skin tints, fragrances, hair masks and ingredient-led skincare.

Global beauty giants have noticed this shift very aggressively.

Reliance recently launched Fenty Beauty in India through an elaborate Mumbai pop-up experience with Rihanna and Isha Ambani. Estée Lauder is acquiring Forest Essentials outright. HUL bought Minimalist. L’Oréal is reportedly exploring Indian D2C acquisitions while simultaneously investing in a ₹3,500 crore AI-led beauty technology hub in Hyderabad.

Shoppers Stop sits directly inside this broader beauty wave.

Its Global SSBeauty Brands distribution business grew 81% year-on-year to ₹426 crore during FY26. Over the last three years, that business has compounded at a staggering 90% CAGR.

The network now includes Armani, Prada and NARS boutiques along with distribution partnerships across 565 points of sale and 27 retailers. The company also onboarded brands like Jimmy Choo, Tory Burch Beauty, Narciso Rodriguez, Coach, Issey Miyake and Serge Lutens.

In practical terms, this means Shoppers Stop is slowly positioning itself as a gateway for premium global beauty and fragrance brands entering India.

And beauty retail is strategically important because beauty consumers behave differently from fashion consumers. Beauty products create repetition.

A customer may buy a handbag once every year or two, but they might repurchase a serum, perfume or foundation every few months. Once consumers trust a beauty product, switching behaviour also becomes stickier.

That is why beauty retail globally has become heavily dependent on ecosystems, repeat consumption and loyalty programs.

Which brings us to another important detail inside the earnings this quarter.

Shoppers Stop’s business is becoming increasingly loyalty-driven.

Its First Citizen membership program contributed 83% of total sales during the quarter. The company now has 13.5 million members. Black Card membership rose 50% year-on-year to 134,000 while Silver membership rose 16% to 800,000.

Even more importantly, repeat members contributed 68% of total sales. Modern retail economics increasingly depend on retaining customers rather than constantly acquiring new ones. Customer acquisition through digital advertising has become expensive. Influencer marketing costs are rising. Social media is overcrowded. Discounting hurts margins.

So retailers are trying to build habit ecosystems.Airlines do this through loyalty miles. Hotels do this through membership tiers. Credit cards do this through reward programs.

Shoppers Stop is trying to do the same through fashion and beauty retail.

Its Black Card customers alone contributed 21% of total sales. The company hosted 36 Black Card events across 25 cities and expanded its personal shopper business, which generated over ₹1,200 crore in revenue during FY26.

Indian premium retail is increasingly becoming service-led rather than transaction-led. Consumers spending ₹20,000 or ₹50,000 in one visit expect curation, guidance and experiences alongside products. Physical retail still holds a major advantage here because certain categories simply work better offline.

Perfumes need testing. Luxury beauty products need consultation. Foundation matching still works best with human assistance.

That is why Shoppers Stop conducted more than 200,000 makeovers and over 370 beauty masterclasses during the quarter. According to the company, those activities alone contributed nearly ₹46 crore in beauty sales.

But while the premiumisation story looks exciting, the financial stress underneath the business is still very real. Global supply-chain disruptions are beginning to create inflationary pressure across retail categories.

Management itself acknowledged that supply-chain disruptions may impact costs in upcoming quarters. And then there is INTUNE. This is probably the most fascinating contradiction inside the entire Shoppers Stop story. While the core business is moving aggressively toward affluent premium consumers, INTUNE targets almost the opposite segment: Affordable fast fashion.

The company introduced a ₹1,299 price point across categories inside INTUNE and says early response has been encouraging. The sales rose 46% during FY26. But despite that growth, the business remains deeply loss-making. EBITDA losses widened to ₹80 crore during the year.

So why continue investing in it?

Because Indian retail is increasingly splitting into two completely different consumption stories. One India is premiumising rapidly. The other India still remains deeply price-sensitive.

Retailers that want long-term scale increasingly need exposure to both markets INTUNE is essentially Shoppers Stop’s attempt to build a value-fashion growth engine before the segment becomes too crowded.

Whether it succeeds remains uncertain. But the company says sales trends improved sharply from February onward and momentum continued into April.

In the cash flow statement, Shoppers Stop generated ₹301 crore in operating cash flow during FY26 compared to just ₹70 crore last year. That improvement largely came from ₹155 crore worth of working capital optimisation.

In simpler terms, the company became far more disciplined with inventory and cash management. Interestingly, Shoppers Stop reduced inventory despite expansion.

The company also reduced debt by ₹109 crore during the year and says it is on track to become debt-free by FY27. After years of startup cash burn and e-commerce discount wars, investors increasingly want operational discipline, cash generation and sustainable economics.

And perhaps that is the real takeaway from these earnings.

Shoppers Stop understands that India’s next retail boom may come from selling aspiration itself. At the same time, the company also knows India remains an extremely unequal market where value-conscious consumption still dominates large sections of the population.

One India is buying Armani fragrances, joining Black Card loyalty programs and spending heavily on beauty routines.

The other India is still comparing ₹799 jeans with ₹999 jeans.

And the company is trying to build businesses for both worlds at the same time.

That balancing act is what makes these earnings genuinely interesting.