Everyone thought the biggest bottleneck in the AI boom would be chips.

Turns out, it might be electricity.

Over the last two years, the AI conversation has been dominated by Nvidia GPUs, trillion-parameter models, hyperscalers, and giant data centres being built across the US, Europe, and the Middle East.

Microsoft is spending aggressively. Meta plans to spend up to $65 billion in capex in 2026. Amazon, Google, Oracle, OpenAI, xAI, and dozens of others are racing to build more computing capacity. But somewhere in the middle of this frenzy, a far less known industry quietly became one of the most important sectors in the global economy.

Gas turbines.

Not because the world suddenly fell back in love with fossil fuels. But because AI data centres consume astonishing amounts of electricity, and the existing power grid is nowhere close to ready for what is coming next.

To understand the scale here, a traditional data centre already consumes huge amounts of power. But AI data centres are in another league altogether. Training and running large AI models requires thousands of GPUs operating continuously, often 24/7, at extremely high power densities.

According to industry estimates, electricity consumption from data centres is expected to rise nearly 96% between 2026 and 2031. Hyperscale facilities are now demanding hundreds of megawatts each. Some campuses are approaching gigawatt-scale requirements, which is equivalent to the electricity needs of entire cities.

And this is creating a very awkward problem.

The AI industry moves on software timelines. Power infrastructure moves on industrial timelines.

You can order GPUs relatively quickly. You can train a new model in months. But building transmission infrastructure, transformers, substations, power plants, and grid connections can take anywhere between 5 to 10 years.

In many regions, utilities are now receiving data centre requests faster than they can physically expand the grid. Transmission queues are clogged. Renewable projects are delayed. Interconnection approvals are slow. Some utilities are openly warning that they cannot provide enough reliable power fast enough.

So tech companies are looking for the fastest scalable source of reliable electricity available today.

That source is natural gas.

More specifically, gas turbines.

These turbines are essentially giant jet engines connected to electricity generators. Natural gas burns inside them, turbines spin at extraordinary speeds, and electricity is produced. Unlike solar or wind, gas turbines can generate power whenever needed.

That reliability matters enormously for AI infrastructure because data centres cannot tolerate unstable voltage, outages, or intermittent power supply. AI workloads require what the energy industry calls “dispatchable power” — electricity that can be delivered on demand, instantly and continuously.

This is where the story gets interesting.

The world has enough natural gas.

What it does not have enough of is gas turbines.

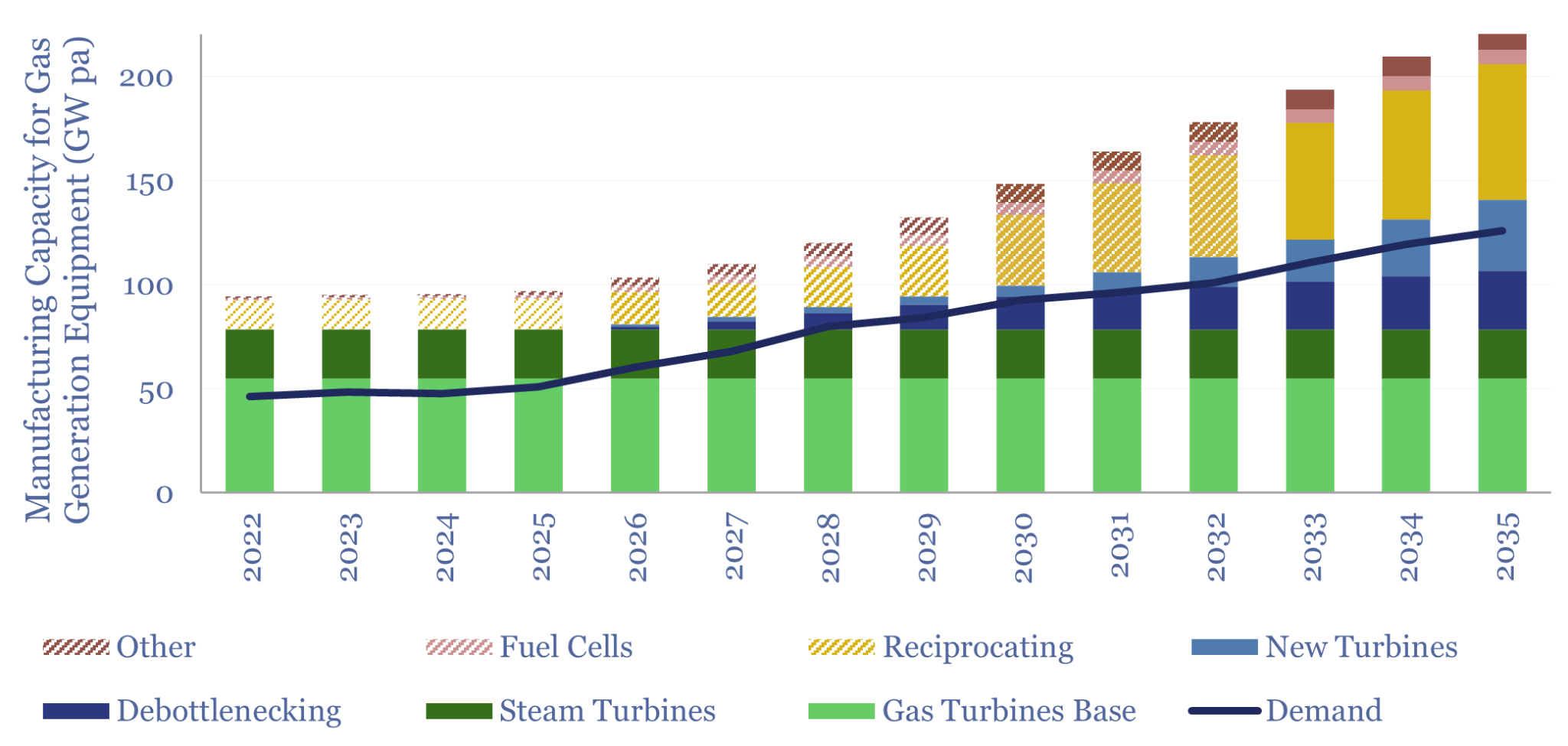

According to Wood Mackenzie, global gas turbine orders reached roughly 110 GW by the end of 2025. But global manufacturing capacity is only around 60-70 GW annually. That gap has created one of the biggest industrial bottlenecks in energy markets today. Lead times for turbines have stretched to 5-7 years. Some order books are already effectively sold out through 2030.

Image Source: Thunder Said Energy

Prices are exploding alongside demand. Wood Mackenzie estimates turbine prices could touch roughly $600/kW by the end of 2027, representing a staggering 195% increase from 2019 levels. Gas turbines already account for nearly 20-30% of combined-cycle plant costs and an even higher share in simple-cycle plants. So this is no longer just a fuel story. It is becoming a procurement story.

In fact, some power developers are now reserving manufacturing slots years in advance simply to secure delivery. GE Vernova, one of the world’s largest turbine manufacturers, expects to end 2025 with an 80 GW gas turbine backlog stretching into 2029. CEO Scott Strazik recently said turbine reservations could be sold out through 2030 by the end of 2026. The company has already booked 18 GW of turbine orders in a single quarter. Customers are no longer just buying turbines. They are paying for manufacturing certainty.

And yet, turbine manufacturers are being surprisingly cautious about ramping up production aggressively.

But if demand is exploding, why not just build more factories?

Because this industry has seen this movie before.

Around two decades ago, during the early internet boom, turbine manufacturers expanded production aggressively expecting massive growth in electricity demand. But the surge did not materialise as expected. The result was oversupply, collapsing prices, and painful financial damage across the sector. Many companies were left with excess capacity for years.

That historical trauma still shapes the industry today.

Executives at Mitsubishi Power and Siemens Energy have openly admitted they are wary of overbuilding capacity based purely on AI hype. One manufacturer dramatically increasing output could eventually crash pricing across the industry if demand normalises later. So despite massive current shortages, OEMs are expanding carefully rather than recklessly.

And this caution is colliding directly with AI’s urgency.

The problem becomes even more complicated once you understand how difficult turbines actually are to manufacture.

A modern heavy-duty gas turbine is one of the most sophisticated industrial machines ever built. The hottest section inside these turbines operates at temperatures exceeding 1,500°C, often above the melting point of the underlying metal itself. The blades rotate at extraordinary speeds while handling immense thermal and mechanical stress simultaneously.

Ordinary metal would fail instantly under those conditions.

So manufacturers developed one of the most remarkable feats in industrial metallurgy: single crystal turbine blades.

Normally, metals contain multiple microscopic crystal grains. Those grain boundaries become weak points under extreme stress and heat. Single crystal blades eliminate those grain boundaries entirely by growing the entire blade as one continuous crystal structure. This improves strength, creep resistance, and thermal durability.

But manufacturing them is brutally difficult.

The process involves vacuum casting, advanced ceramic core design, internal cooling channels, thermal barrier coatings, precision heat treatment, and decades of accumulated materials science expertise. Academic studies estimate a single set of roughly 40 advanced turbine blades can cost over $600,000 and require 60 to 90 weeks to manufacture.

This is why the gas turbine industry remains so concentrated globally.

Only a handful of companies truly dominate advanced turbine manufacturing at scale: GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Rolls Royce, Baker Hughes, and Solar Turbines. The moat here is not just patents or designs. It is process knowledge accumulated over decades. You can copy the external shape of a turbine blade. You cannot easily replicate 50 years of metallurgy data, failure analysis, coating chemistry, and manufacturing precision.

And the bottlenecks do not stop at turbines.

Transformers are also becoming critically constrained. These devices step electricity up and down across the grid and inside data centres. Lead times for large transformers now stretch into years. GE Vernova recently completed its $5.3 billion acquisition of Prolec GE largely to strengthen its transformer manufacturing footprint. The company openly admits transformers are now one of the biggest choke points in electrical infrastructure.

Then there are shortages in:

- skilled labour,

- EPC contractors,

- grid engineers,

- electricians,

- hot-section turbine components,

- coatings,

- forgings,

- and transmission equipment.

The AI economy is suddenly rediscovering something markets ignored for years: software still depends on physical infrastructure.

And that is where India quietly enters the story.

India itself is not currently experiencing a massive domestic gas turbine construction boom. Gas-based power utilisation remains relatively low compared to coal and renewables. But Indian companies are increasingly entering the global turbine manufacturing supply chain, especially in high-precision engineering and metallurgy.

Azad Engineering is one example. The company supplies critical components to multiple global turbine OEMs controlling roughly 75% of the global turbine market. In March 2026, Azad signed an 8-year single-source agreement with Mitsubishi Heavy Industries for hot-section nozzle vane segments. This is important because the hot section is where the most advanced metallurgy exists.

PTC Industries, through Aerolloy Technologies, became the first Indian company to secure a GTRE-DRDO order involving post-cast operations on single-crystal-ready turbine blades and vanes. The scope includes vacuum heat treatment, thermal barrier coating, brazing, and advanced machining. These capabilities overlap not just with energy but also aerospace and defence manufacturing.

This is what makes the turbine story fascinating.

At one level, it is about electricity shortages.

At another level, it is about industrial policy, metallurgy, advanced manufacturing, supply chains, and the physical limits of infrastructure scaling.

For nearly 15 years, technology investing was dominated by software narratives. Apps scaled infinitely. Cloud computing abstracted away physical constraints. AI has abruptly reversed that illusion. Every AI query eventually converts into watts, cooling requirements, substations, transformers, turbines, and transmission lines.

The companies supplying those physical systems operate on timelines measured in decades, not quarters.

And that may become one of the defining economic realities of the AI era.