India’s startup ecosystem is approaching a milestone that once felt wildly optimistic.

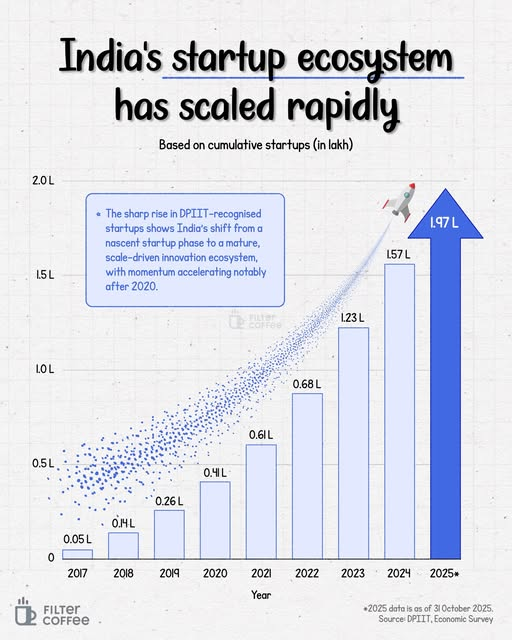

According to government data, India now has nearly 2 lakh DPIIT-recognised startups, a massive jump from just a few thousand a decade ago. The latest count stood at about 1.97 lakh startups as of October 2025, and the pace of growth over the past few years shows how dramatically the country’s innovation economy has scaled.

But the number itself is only part of the story.

The real shift is how quickly India moved from a phase of experimentation to a phase of scale.

Back in 2017, the number of recognised startups was barely 5,000. By 2019 it crossed 26,000. Then something interesting happened around 2020. The growth curve steepened sharply. Within just a few years, the count shot past 60,000 in 2021, crossed 1.2 lakh by 2023, and surged toward the two-lakh mark by 2025.

In less than a decade, the ecosystem multiplied nearly forty times.

That acceleration was several structural changes that reshaped the landscape. One of the biggest was formal recognition. The Startup India programme, launched in 2016, made it easier for founders to register, access tax incentives, and qualify for government schemes. This recognition allows startups to tap into benefits such as easier compliance rules, intellectual property support, and eligibility for government procurement.

But policy support alone does not create thousands of companies.

The second big catalyst was capital. Venture capital and private equity funding poured into India through the late 2010s and early 2020s. Global investors began to see India not just as a large market but as a place where technology companies could be built at scale. Startup funding surged dramatically, producing a wave of unicorns in sectors like fintech, e-commerce, logistics, SaaS, and mobility.

Then came the pandemic, which ironically accelerated the ecosystem further. Lockdowns pushed millions of Indians online, speeding up digital adoption across payments, commerce, healthcare, and education. Startups suddenly found themselves building solutions for a country that was becoming digital almost overnight. The result was a surge in entrepreneurial activity and company formation after 2020.

However, the story does not end with rapid expansion. The ecosystem is now entering a new phase where scale alone is no longer enough.

The focus is shifting toward sustainability and deeper innovation. Out of the nearly 2 lakh recognised startups, government data indicates that more than 6,000 have already shut down or dissolved. Failure is not an exception in this world; it is part of the process through which stronger companies emerge.

Policy changes are also evolving to match this maturity.

In early 2026, the government updated the official definition of a startup by raising the turnover limit for recognition to ₹200 crore, up from the earlier ₹100 crore threshold. This seemingly small change reflects a larger shift in thinking. Startups in India are no longer tiny experimental ventures. Many grow rapidly and need the flexibility to remain within the startup framework even as they scale.

Another notable development is the growing emphasis on deep technology startups. Policymakers are increasingly focusing on companies working in areas such as artificial intelligence, semiconductor design, robotics, spacetech, and climate technologies.

Reports suggest that India’s deeptech startups attracted around $2.3 billion in funding in 2025, a significant increase from the previous year. Within this segment, artificial intelligence has become the dominant theme, accounting for the overwhelming majority of deeptech investments.

The funding environment itself is also evolving. After the global venture capital slowdown of 2022 and 2023, early signs suggest that investment activity is stabilising again.

Indian startups raised roughly $1.2 billion in February 2026 alone, more than double the amount raised in the same period a year earlier. The difference now is that investors are becoming far more selective. The era of easy money and aggressive growth at all costs appears to be fading, replaced by a focus on sustainable business models and real revenue generation.

Tax and regulatory changes are also gradually addressing long-standing friction points. The removal of the controversial angel tax on startup investments was widely seen as a major positive signal for early-stage funding. At the same time, discussions are underway to expand ESOP tax deferral benefits to a wider set of startups, which could make employee stock ownership more attractive for talent joining young companies.

Taken together, the country is no longer trying to prove that startups can exist here. That question has already been answered. Instead, the conversation is moving toward what kind of startups India will produce next.

The next decade may look very different from the last one. The first wave was dominated by consumer internet companies solving everyday problems like payments, food delivery, ride-hailing, and online shopping. The next wave is increasingly expected to focus on deeper technologies, manufacturing innovation, climate solutions, and AI-driven infrastructure.

In other words, India’s startup story is gradually transitioning from a volume game to a value game. The rise from a few thousand startups to nearly two lakh within a decade shows how quickly entrepreneurial energy can scale in the right environment.

The real test now is whether this massive ecosystem can produce companies that not only grow fast but also build durable global businesses. If that happens, the number of startups may soon become the least interesting part of the story.