Every year, Mumbai does the same dance with the monsoon.

People leave home 30 minutes early “just in case.” Local train updates suddenly become the most important notifications on everyone’s phones. Offices start discussing work-from-home policies with suspicious urgency. Delivery apps show impossible timings. Construction sites slow down. Flights get delayed. Roads disappear under water. And somewhere in the middle of all this chaos, there’s always one person posting Marine Drive videos like the city is starring in its own disaster movie again.

For most people, rain is just weather. For Mumbai, rain is infrastructure stress, economic disruption, productivity loss, supply-chain chaos, and occasionally, emotional damage.

Now imagine turning all of that into a financial product.

That’s essentially what India is about to try.

The National Commodity & Derivatives Exchange, or NCDEX, is preparing to launch India’s first rainfall futures contract. The product, called RAINMUMBAI, will allow market participants to trade contracts linked to Mumbai’s monsoon rainfall using official data from the India Meteorological Department.

“But how do you trade rain?”

Fair question. Because this is not really a story about rain. It is a story about what happens when climate uncertainty becomes expensive enough for financial markets to start building products around it.

Let’s first understand how deeply the weather shapes India’s economy!

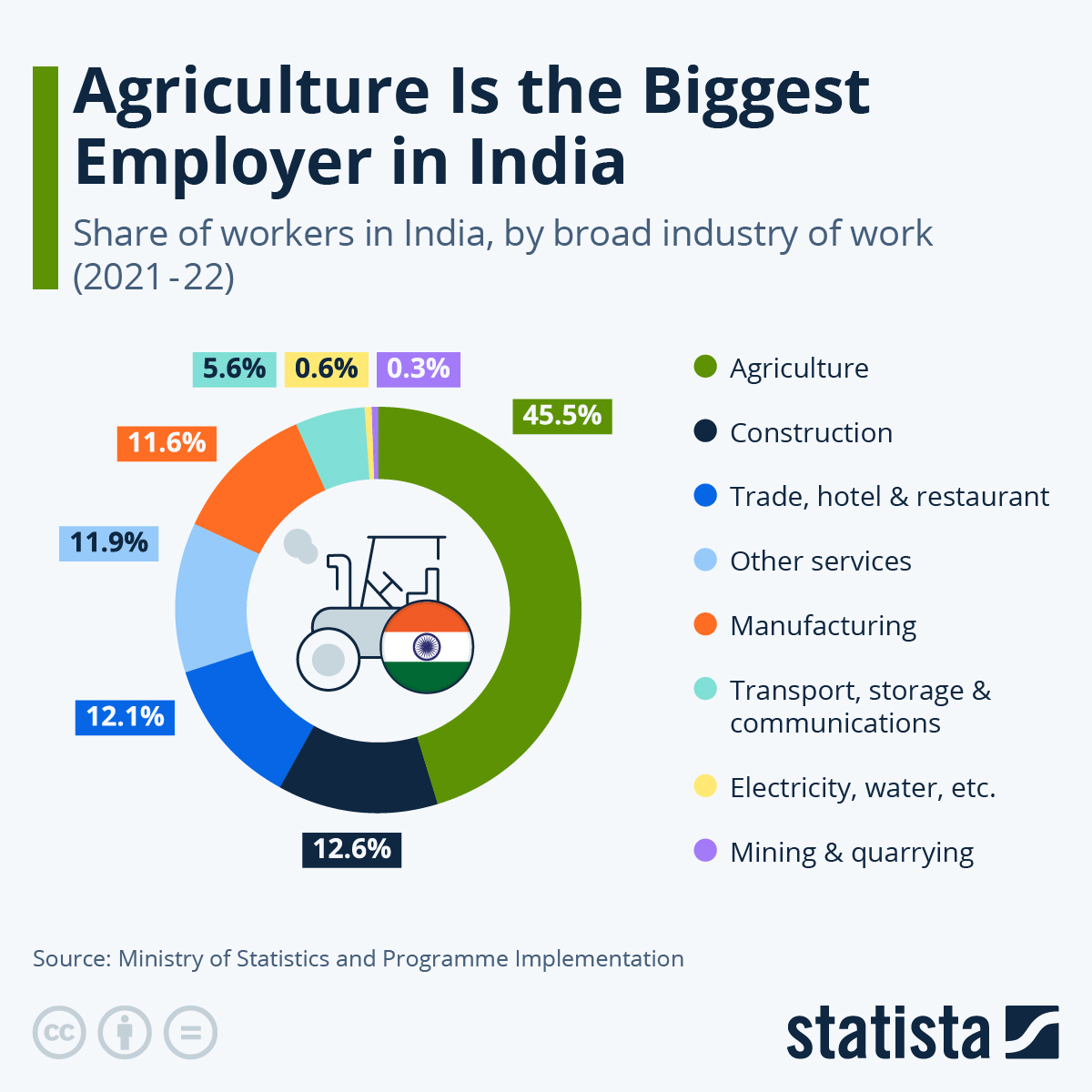

India still depends heavily on monsoons in ways most modern economies no longer do. Nearly half the country’s workforce is connected to agriculture. A weak monsoon can hurt crop output, push up food prices, affect rural consumption, and create inflation pressures across the economy. Excessive rainfall creates a different set of problems. Flooded cities, disrupted logistics, delayed infrastructure projects, damaged crops, higher insurance claims, and lower productivity.

Even sectors that appear disconnected from weather end up getting affected. Retail footfall changes. Electricity demand fluctuates. Construction timelines move. Commodity prices react. Transportation slows down.

In many ways, rainfall in India behaves less like a seasonal event and more like an economic variable. And financial markets have always had a habit of trying to price economic uncertainty.

Oil prices became tradable. Interest rates became tradable. Volatility became tradable. Weather was eventually going to enter the list too.

In fact, weather derivatives have existed globally for years. The Chicago Mercantile Exchange in the US has offered weather-linked contracts since the late 1990s. Companies there already hedge risks linked to snowfall, temperatures, and hurricanes.

Utilities use them because warmer winters reduce heating demand. Retailers use them because unexpected weather affects sales patterns. Energy companies use them because electricity consumption is heavily weather dependent.

Ironically, one of the earliest companies to popularise weather derivatives was Enron. Yes, that Enron.

> Enron was an American energy company that became hugely famous in the 1990s for turning things like electricity, gas, and even weather into tradable financial markets. But in 2001, it collapsed after massive accounting fraud was exposed, becoming one of the biggest corporate scandals in history and a warning sign about how risky complex financial engineering can become when greed takes over.

Their basic logic was surprisingly straightforward. If weather affects revenues, then weather risk can also be hedged financially.

India is now slowly entering the same territory.

The proposed Mumbai rainfall contract works using historical rainfall averages. Mumbai’s long-period average monsoon rainfall sits at around 2206.7 millimetres. During the season, actual rainfall will be measured against this benchmark. If rainfall exceeds the average, the deviation moves positive. If rainfall remains below average, it turns negative. Traders and businesses can then take positions based on these outcomes.

Now, this does not mean somebody sitting in Bandra will suddenly start day-trading clouds on Zerodha.

The early users are more likely to be businesses with genuine exposure to weather disruptions. Think logistics firms, insurers, commodity players, construction companies, energy utilities, or even large retailers.

For example, imagine a construction company that loses money every time heavy rain delays projects. Or a logistics company whose delivery network slows down during flooding. A rainfall-linked hedge could help offset some of those losses financially.

India recently forecast below-average monsoon rainfall for 2026 for the first time in three years. Heatwaves are becoming more frequent. Urban flooding now feels less like an exception and more like an annual event. Climate volatility is no longer theoretical. Businesses are already dealing with its consequences.

According to various estimates, India has lost roughly $180 billion over the last three decades due to extreme weather events. Globally too, insurers and financial institutions are increasingly worried about climate-linked losses becoming structurally bigger.

Which is why a much larger trend is quietly emerging across the world.

Climate risk is slowly entering financial markets.

That may sound abstract, but it is already visible everywhere. Carbon markets are growing. Catastrophe bonds are becoming more common. Parametric insurance products are expanding. Investors are increasingly evaluating climate exposure while pricing infrastructure and real estate projects.

Rainfall futures are part of that same shift.

And there’s another important detail here. Products like these are not traditional insurance.

Usually, insurance claims involve paperwork, inspections, verification, and long settlement timelines. Parametric products work differently. If a predefined trigger is hit, payouts happen automatically based on data itself.

So if rainfall crosses a certain threshold, the settlement gets triggered immediately. No one needs to physically inspect flooded roads or damaged warehouses first. That efficiency is one reason climate-linked financial products are attracting attention globally.

But this is also where the story becomes slightly uncomfortable.

Because once financial markets create a tradable product, speculation inevitably follows. Today, the official pitch is risk management. But markets rarely stop there. Over time, hedge funds, traders, and speculators may enter simply because volatility itself becomes profitable.

At some point, people with zero direct exposure to rainfall may start betting on floods and droughts purely for financial gain.

And suddenly the whole thing starts raising awkward questions. Are we adapting to climate change? Or are we learning how to trade around it?

Because rainfall futures will not fix Mumbai’s drainage systems. They will not stop roads from flooding every monsoon. They will not help informal workers stranded during extreme weather. They will not make Indian cities climate-resilient. At best, they redistribute financial losses after the damage is already done.

And yet, dismissing the idea entirely would also be shortsighted.

Financial systems tend to evolve when risks become unavoidable. Insurance itself emerged because people realised uncertainty needed mechanisms to absorb financial shocks. Weather derivatives are essentially an extension of that logic into a climate-stressed world.

And maybe that is the real story here.

Mumbai’s rainfall becoming tradable sounds absurd only because climate volatility still feels emotionally disconnected from finance for most people. But markets are already treating climate instability as an economic reality that needs pricing, hedging, and financial infrastructure around it.

Which means this launch is not just about rain.

It is about how economies behave when climate uncertainty stops being occasional and starts becoming permanent.